Embed Size (px)

Citation preview

Presented By-Harjeet KaurMegha Tomar

Priyanka JoliyaSakshi Kankar

WHAT IS BUDGET??Budget is a detailed plan of operations for some specific future period.

According to Gordon budget may be defined as “a predetermined detailed plan of action developed and distributed as a guide to current operations and as a partial basis for the subsequent evaluation of performance”.

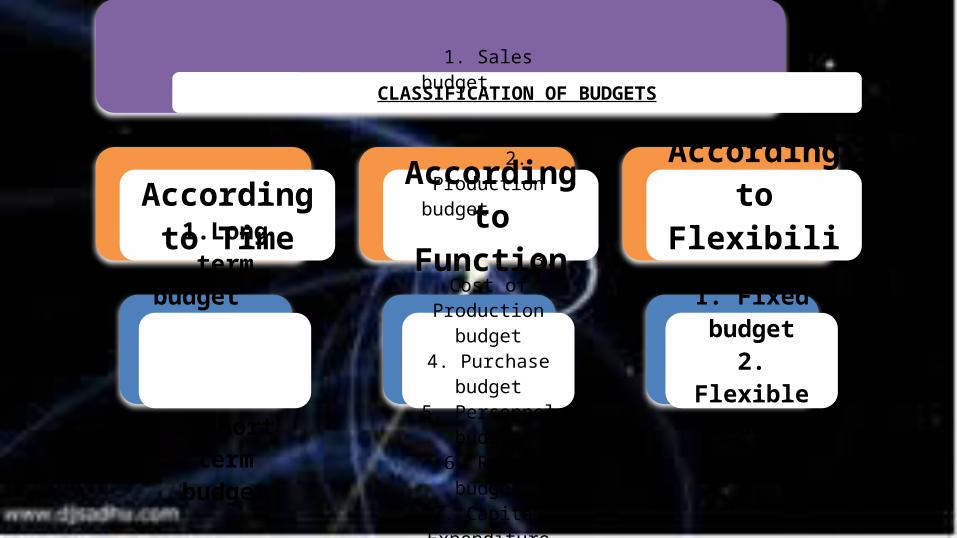

CLASSIFICATION OF BUDGETS

According to Time

1.Long term

budget 2.Short

term budget

According to Function

1. Sales budget 2. Production

budget 3.

Cost of Production

budget4. Purchase

budget5. Personnel

budget6. R & D budget

7. Capital Expenditure

budget8. Cash budget

9. Master budget

According to Flexibility

1. Fixed budget

2. Flexible budget

According to Function1. SALES BUDGET: Sales budget is the most

important budget based on which all the other budgets are built up. This budget is a forecast of quantities and values of sales to be achieved in a budget period.

2. PRODUCTION BUDGET: Production budget involves planning the level of production which in turn involves the answer to the following questions:a. What is to be produced?b. When is it to be produced?c. How is it to be produced?d. Where is it to be produced?

3. COST OF PRODUCTION BUDGET:This budget is an estimate of cost of output planned for a budget period and may be classified into –

• Material Cost Budget• Labour Cost Budget• Overhead Cost Budget

4. PURCHASE BUDGET:This budget provides information about the materials to be acquired from the market during the budget period.

5. PERSONNEL BUDGET:

This budget gives an estimate of the requirements of direct labour essential to meet the production target. This budget may be classified into –

a. Labour requirement budget b. Labour recruitment budget6. RESEARCH AND DEVELOPMENT BUDGET:

This budget provides an estimate of expenditure to be incurred on R & D during the budget period.

A R&D budget is prepared taking into consideration the research projects in hand and new R & D projects to be taken up.

7. CAPITAL EXPENDITURE BUDGET: This is an important budget providing for acquisition of assets necessitated by the following factors:a. Replacement of existing assets.b. Purchase of additional assets to meet increased productionc. Installation of improved type of machinery to reduce costs.8.CASH BUDGET: This budget gives an estimate of the anticipated receipts and payments of cash during the budget period.Cash budget makes the provision for minimum cash balance to be maintained at all times.

9. MASTER BUDGET:

CIMA defines this budget as “ The summary budget incorporating its component functional budget and which is finally approved, adopted and employed”.Thus master budget is a summary of all functional budgets in capsule form available in one report.

FIXED BUDGET: This is defined as a budget which is designed to remain unchanged irrespective of the volume of output or turnover attained.This budget will, therefore, be useful only when the actual level of activity corresponds to the budgeted level of activity.

According to Flexibility

FLEXIBLE BUDGET: CIMA defines this budget as one “ which, by recognizing the difference in behavior between fixed and variable costs in relation to fluctuations in output, turnover or other variable factors such as number of employees, is designed to change appropriately with such fluctuations”.

Short Term Budget•May cover periods of three to twelve months depending upon nature of business•Should be long enough to allow completion of a season or all aspects of a business•The period should coincide with financial accounting period to facilitate evaluation of performance•e.g. A budget allocated to manufacturing of lots for spring-summer season, Fashion Retailing, etc.

Long Term Budget•A systematic and formalized process for directing & controlling operations for period extending beyond one year•It evaluates future implications associated with present decisions•Market trends, change in demographics, national income, etc. play important role in preparing long term budget•It proves useful in forecasting and evaluation of an organization over period of time•e.g. A father planning money requirement for his child’s future.

According to Time

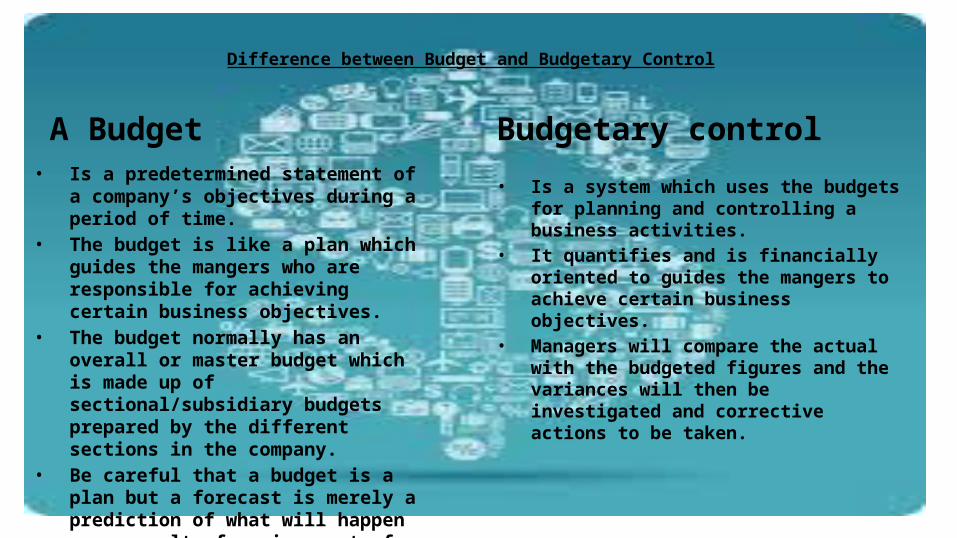

Difference between Budget and Budgetary Control

A Budget• Is a predetermined statement of

a company’s objectives during a period of time.

• The budget is like a plan which guides the mangers who are responsible for achieving certain business objectives.

• The budget normally has an overall or master budget which is made up of sectional/subsidiary budgets prepared by the different sections in the company.

• Be careful that a budget is a plan but a forecast is merely a prediction of what will happen as a result of a given set of circumstances.

Budgetary control• Is a system which uses the

budgets for planning and controlling a business activities.

• It quantifies and is financially oriented to guides the mangers to achieve certain business objectives.

• Managers will compare the actual with the budgeted figures and the variances will then be investigated and corrective actions to be taken.