Embed Size (px)

Citation preview

Sociedade de ConstruçõesSoares da Costa, SA

2012SUMMARY OF

REPORT &ACCOUNTS

REPORT & ACCOUNTS 2012 | SOCIEDADE DE CONSTRUÇÕES SOARES DA COSTA, SA

SOCIEDADE DE CONSTRUÇõES SOARES DA COSTA

.1

PROFILE

Sociedade de Construções Soares da Costa, S.A. is the main construc-tion, engineering and infrastruture company of Soares da Costa Group. In addition to a relevant position in the domestic market, the company has a very strong international activity, operating in Angola, Mozam-bique and Romania. Regarding international operations, the Angolan market has the most relevant role. This business portfolio, with expo-sure to a mature market (Portugal) and emerging markets, is one of the key positive features of the company, allowing risk diversification, to maintain growth rates significantly above its domestic market and also to display a higher resilience of its profitability and competitive pressure.

MISSION

As Soares da Costa Group main company operating in the construction area, Sociedade de Construções Soares da Costa, has the responsibili-ty to, through this business area, embody and materialize its mission: “answer to the market and to our clients’ needs, through a sustainable business model, motivated and skilled resources, generating economic, social and environmental value, with an attractive return to sharehol-ders”. This mission is pursued through a set of values, which although defined at the Group’s level, are proudly shared by the company:

> Permanent orientation to the market and to the clients’ satisfaction,

> Management’s efficiency,

> Integrity and ethics,

> Socially responsible conduct,

> Respect for the environment.

STRATEGY

Following the strategic guidelines presented to the Group in September 2010, that were revised in November 2011, and sharing these guideli-nes with the construction business area of which is part, Sociedade de Construções is concentred in enhancing growth of its international ac-tivity, including the consolidation of the strong positioning achieved in some markets (Angola, Mozambique) and in the defence of its activity’s profitability and sustainability.

Strong international positioning

Main international markets: Angola e Mozambique

Focus on internationalactivity growth

23

The current strategic plan was defined and approved during the second half of 2011, when the Group’s management, taking into consideration the substantial changes that took place in the macroeconomic context, the financing scarcity and the strong contraction of the domestic cons-truction market, decided to adjust and update the Group’s strategic planning. In general terms, this adjustment consists in a strong focus on the construction activity in the Group’s core markets. The strategic guidelines being implemented are strongly oriented to INTERNACIONA-LISATION, to the CONSTRUCTION business area and to the FINANCIAL SUSTAINABILITY of the activities. This strategic guidelines target to assure an activity growth level compatible with the external restrictions, namely financial, to protect profitability levels and to achieve, by the end of the period of the plan’s implementation, a significant reduction in the indebtness level.

SHAREHOLDERS’ STRUCTURE

Soares da Costa Group holds 100% of Sociedade de Construções Soares da Costa’s share capital. The Group, with more than 90 years of history, is currently a diversified group, with a strong positioning in the construction market but also operating in some construction sector’s complementary areas: transport concessions, real estate and energy services. The Group’s activity also has a traditionally intense interna-tional profile, representing more than 70% of the Group’s consolidated turnover in 2012.

The Group’s strategic guidelines: INTERNACIONALIZATION, focus on the CONSTRUCTION business area and on the FINANCIAL SUSTAINABILITY

Soares da Costa Group holds 100% of Sociedade de Construções Soares da Costa

2012 IN GRAPHICS 2.

100 200 300 400 500 600 700

2011 606

2012 520Evolution of Turnover

Turnover (million Euros)

REPORT & ACCOUNTS 2012 | SOCIEDADE DE CONSTRUÇÕES SOARES DA COSTA, SA

Evolution of EBITDA (Recurrent and Non Recurrent)

EBITDA(million Euros)

Recurrent EBITDA(million Euros)

10 20 4030 50 60

201146

47

201226

36

EBITDA Margin

Recurrent EBITDA Margin

Evolution of EBITDA Margin (Recurrent and Non Recurrent)

5.1%

6.9%7.5%

7.7%

2011 2012

Evolution of EBIT(Non Recurrent)

EBIT (million Euros)

0-5 5 10 20 2515 30 35

2011 32

2012 -2

Portugal

32%

Angola

61%Mozambique

7%

Other Countries

0,5%

Romania

0,1%Turnover’s Breakdown by

Market in 2012

25

Financial Results(million Euros)

Evolution of Financial Results

Evolution of Net Earnings(Non Recurrent)

Net Earnings(million Euros)

-30 -25 -15 -10-20 -5

2011-13

2012-28

-25-30 -20 -15 -5 0-10 5 10 15

2011 -24

2012 12

EVOLUTION OF THE ACTIVITY IN 2012 3.

HIGHLIGHTS

> Turnover attained 520.0 million Euros, coming in 14.1% below the corresponding amount of the previous year, reflecting a steeper drop in the domestic market (-29.4%);

> The international market represented 68.3% of the activity (61.5% in 2011);

> Organizational and operational (reallocation and reduction of per-manent employees and merger by incorporation of Contacto) and financial (rescheduling of debt maturities) restructuring;

> EBITDA of 26.3 million Euros (45.5 million Euros in 2011) is im-paired by non-recurring costs incurred with the termination of labour contracts of 9.5 million Euros (1.1 million Euros in 2011);

> Financial results of -28.1 million Euros versus -13.3 million in the previous year;

> Restructuring costs and credit impairments significantly affect the earnings before tax of -30.4 million Euros (+12.2 million in 2011);

> Net loss of 24.3 million Euros versus the net income of 12.2 mil-lion Euros of the previous year.

REPORT & ACCOUNTS 2012 | SOCIEDADE DE CONSTRUÇÕES SOARES DA COSTA, SA

14% decrease in turnover 2012, strongly impacted by the

domestic activity decline

Very pronounced decline of the activity in Portugal

Key Performance Indicators

(million Euros) 2012 2011 Variation

Turnover 520.0 605.7 -14.1%

Portugal 164.7 233.1 -29.4%

International activity 355.3 372.6 -4.6%

EBITDA 26.3 45.5 -42.3%

EBITDA margin 5.1% 7.5% -2.5p.p.

Recurrent EBITDA 35.8 46.6 -17.4%

Recurrent EBITDA margin 6.9% 7.7% -0.8p.p.

Operational results (EBIT) -2.2 31.8 -107%

Financial results -28.1 -13.3 -

Earnings before taxes -30.4 18.5 -

Net earnings -24.3 12.2 -

Note: Recurrent EBITDA is the adjusted EBITDA without costs with termination of labour contracts

ACTIVITY ANALYSIS

TURNOVER

The turnover of the company totalled 520.0 million Euros in 2012, which represents a decline of 14.1% on the amount recorded in the previous year. The following table presents turnover breakdown by geographical market in a comparative analysis with the previous year:

Turnover by Geographical Market

(million Euros) 2012 % 2011 % Variation

Portugal 164.7 31.7% 233.1 38.5% -29.4%

Angola 315.2 60.6% 310.6 51.3% 1.5%

Mozambique 37.3 7.2% 54.9 9.1% -32.0%

Romania 0.3 0.1% 6.6 1.1% -95.4%

Other countries 2.5 0.5% 0.4 0.1% 489.5%

TOTAL 520.0 100.0% 605.7 100.0% -14.1%

The very pronounced decline in PORTUGAL is the most outstanding factor, having decreased significantly in terms of its contribution to global turnover. Nevertheless, regarding the works concluded in 2012 in the domestic market we highlight the power reinforcement capacity at the Alqueva dam, the opening of several stretches integrated in Trans-

27

The international activity also registered a negative evolution, of 4.6%, influenced by the performance in Mozambique and Romania

The Angolan market is the main market of the company, growing 1.5% in 2012

montana motorway, and the road bridges of Jorjais and Tinhela. Also having relevancy in the production volume of this market the works of the road accesses to the Lisboa Norte logistic platform in the stretch Vila Franca de Xira/ Nó A1 of North motorway to Brisa, the construction of the enlargement and improvement to 2x3 ways of the stretch Maia/ Santo Tirso of A3 of Porto/ Valença motorway to Brisa and the Serra da Estrela Inn in Covilhã to Enatur.

The international activity registered a 4.6% decline of its turnover compared with the previous year, with a slightly positive evolution in Angola not completely offsetting the performance in the Mozambican and Romanian market. Therefore, the level of activity in Angola slightly surpassed (+1.5%) the previous’ year figure, while the Mozambican market, representing an interesting activity level, revelled a decrease compared with the extraordinary growth and high level reached in the previous year.

ANGOLA, were the company has had an uninterrupted presence of over three decades, continues to be a primal strategic market in the development of the company’s business, that has strived to attain and consolidate recognized prestige and reputation, namely in the buildings construction segment, with the construction of projects of great impor-tance and significance in the various sub-segments: residential, com-mercial and office buildings.

The infrastructure segment is also an important vector to develop in order to diversify and widen the business portfolio, with the company presenting a significant operational importance and a growing weight in this country.

Amongst the more relevant construction works in the year’s production, in the buildings segment, are the following: 1º Congresso Tower (BESA); Bayview – TTA Office Building (provisionally accepted); Torres Dipanda Building; INE’s new building; Luanda Towers Project; New Office Build-ing AAA; Science and Technology Museum; Hotel da Ilha (Hotel); Armed Forces Museum (completed); and “Shopping Fortaleza” project. In terms of regional diversification the project “Private Residential Hous-ing”, to be developed in Soyo, in the province of Zaire, is of note. It is a condominium construction project to house the technicians of the natu-ral gas facilities of Angola LNG, a project worth close to 220 million USD and in which the company is in consortium with MSF. Noteworthy, too, is the company’s expansion into Huambo with two important projects for this city, the Huambo Cultural Centre and the rehabilitation of the S. José de Cluny School.

In the infrastructure area, in addition to the rehabilitation works on the Luanda’s waterfront road (in the 2nd phase of execution), for Socie-dade Baía de Luanda, we highlight, due to its great significance and amplitude, the project “Rehabilitation of the Slopes of Sambizanga and Boavista” in the amount of circa 90 million USD.

Besides the construction of buildings, Soares da Costa has invested in the infrastructure segment

REPORT & ACCOUNTS 2012 | SOCIEDADE DE CONSTRUÇÕES SOARES DA COSTA, SA

In MOZAMBIQUE, another market in which Soares da Costa has an historical presence, it is important to refer, in this context, solely to the activity carried out by the permanent establishment of the com-pany, given that the construction activity of Grupo Soares da Costa in this territory extends to the Mozambican subsidiary, Soares da Costa Moçambique, S.A.R.L., whose share capital is 80% held by Soares da Costa Construção, S.G.P.S., S.A..

During 2012, the company’s activity was fundamentally concentrated on the important rehabilitation works on the N221 road, between Com-bomune and Chicualaquala and on the construction of the bridge over the Zambezi River, in Tete.

ROMANIA currently has a reduced importance in the total activity of the company. Nevertheless, the followings works were completed in this country during 2012: accesses to the Casimcea wind farm, in Tulcea, a contract amounting to approximately 6 million RON (circa 1.38 million Euros); accesses to the Alpha Wind farm, in Tulcea, a project valued at approximately 3.3 million RON (circa 770 thousand Euros).The work “Constructia Variantei de Ocolire Tecuci” in the amount of 49 million RON (11.1 million Euros), for the national road authority of Ro-mania (CNADNR - Compania Nationala de Autostrazi si Drumuri National din Romania S.A.) is in progress.

In the other geographies we highlight the activity developed in Brazil and the weight of a project in Oman, initiated in the second half of 2012, which should reach a higher volume in 2013.

BRAZIL, according to the Group’s strategic plan, is considered one of the priority markets within the company’s scope of international expan-sion. In 2012, through the 50% shareholding in the specific purpose company Terceira Onda Planejamento e Desenvolvimento Ltda, civil construction works for the implementation of a complete unit were completed in October 2012 in Rio Branco do Sul (Paraná) for Votoran-tim Cimentos. On the other hand, the interventions on the project for production line 3 of the Cezarina cement plant in Goiás for Cimpor Brasil. By the end of 2012, this Brazilian company also commenced a project related with the extension of the Viracopos International Airport terminal, in Campinas, São Paulo, for the construction consortium Vi-racopos. However, given that the 2012 activity was not directly carried out by the company the individual financial statements accompanying this report do not reflect, in numeric terms, the relevant impacts with regards to this market.

In OMAN, following on the successful commercial incursions carried out in previous years, the company participates in a consortium with a local company, in the execution of road infrastructure and associated infrastructure network projects in an area situated between the Masqat international airport and the motorway of the same city.

Mozambique is another market in which Soares da Costa has an

historical presence

Soares da Costa is present in Oman in 2012

Romania reduced significantly its contribution to the total turnover

in 2012

Entrance in the Brazilian market has been gradual, with works in

the industrial segment

29

OPERATIONAL PROFITABILITY

For a better analysis we present below, aggregated in a convenient manner, the following components of the results for the year and that immediately preceding it:

(million Euros) 2012 % OI 2011 % OI Variation

Turnover 520.0 102.3% 605.7 99.5% -14.1%

Change in production -18.9 -3.7% -19.1 -3.1% -1.2%

Other operational income 7.4 1.5% 22.2 3.7% -66.6%

Operational Income (OI) 508.6 100.0% 608.8 100.0% -16.5%

Cost of goods sold 75.8 14.9% 97.7 16.0% -22.4%

External supplies 311.5 61.2% 369.9 60.8% -15.8%

Staff costs 83.8 16.5% 83.1 13.6% 0.9%

Other operational costs 11.2 2.2% 12.6 2.1% -11.3%

EBITDA 26.3 5.2% 45.5 7.5% -42.3%

Depreciations, provisions and Adjustments (net of reversions) 28.5 5.6% 13.7 2.2% 108.1%

Operational Result (EBIT) -2.2 -0.4% 31.8 5.2% -107.0%

Financial Results -28.1 -5.5% -13.3 -2.2% 111.7%

Earnings before taxes -30.4 -6.0% 18.5 3.0% -

Income tax 6.0 1.2% -6.4 1.0% -5.4%

Net earnings -24.3 -4.8% 12.2 2.0% -

Although turnover decreased by 14.1%, the sum of the captions costs of goods sold and external supplies decreased proportionally more (17.2%). However, this effect was neutralized by the behaviour of staff costs which, affected by the compensation costs incurred with labor contracts’ termination by mutual agreement (an amount that attained 9.5 million Euros in 2012, versus the 1.1 million Euros of the previous year), could not yet evidence the expected decrease.

EBITDA margin in relation to total operating revenue decreased from 7.5% to 5.2% but, recalculated, excluding the compensation costs, would have come in at 7.0%, even so, still below that of 2011. A less interesting development in terms of profitability came from the Trans-montana motorway project which, due to the vicissitudes that involved the project and that originated the extension of its execution period, for reasons that were outside the control and intervention of the company, contributed to such negative evolution.

The recognition of impairment losses, namely on credits over third par-ties, consequence of the general adverse panorama of the economy that has been leading to the degradation of the solvency and liquidity conditions of many companies and, thus, to the deterioration of col-lection conditions and to increased litigation, also affected the perfor-mance for the period, increasing the caption depreciations, provisions and adjustments (net of reversals) to an amount (28.5 million Euros) doubling the amount of the previous year (13.7 million Euros).

Efficiency gains were registered at the costs of goods sold and external supplies level

Staff costs were impacted by non-recurrent costs

In 2012 were accounted impairment costs related with general adverse context, with impact at the EBIT level

REPORT & ACCOUNTS 2012 | SOCIEDADE DE CONSTRUÇÕES SOARES DA COSTA, SA

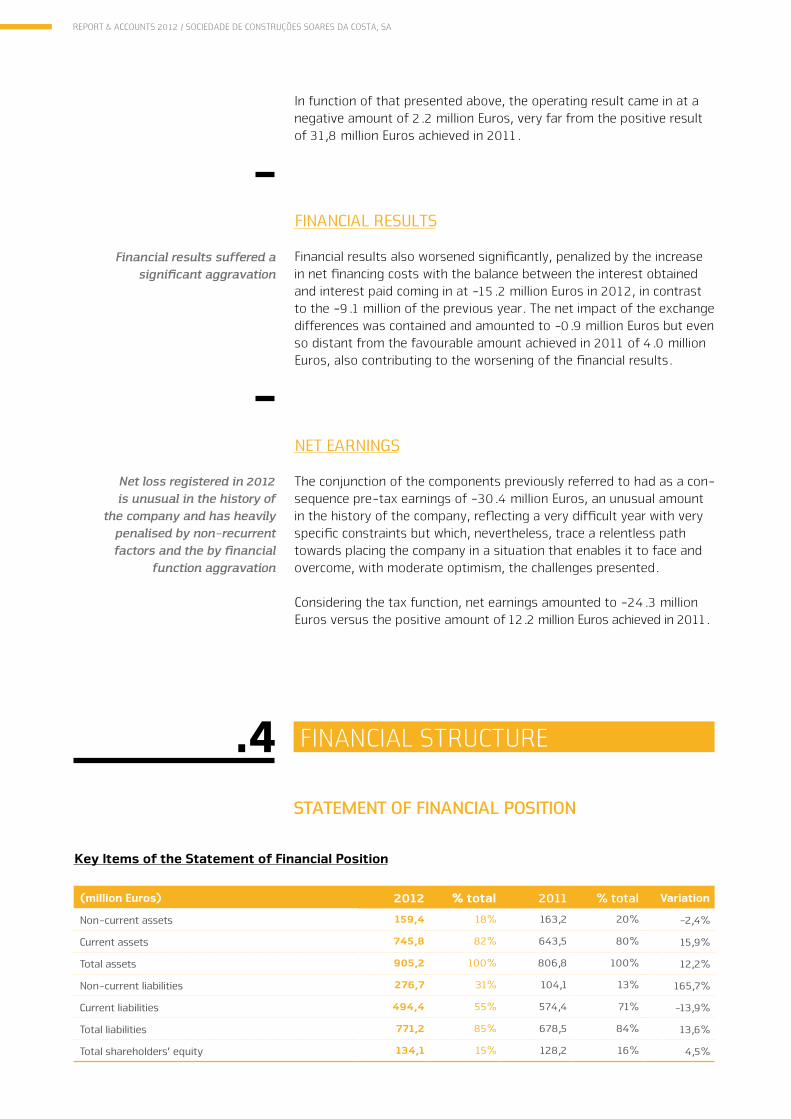

FINANCIAL STRUCTURE.4STATEMENT OF FINANCIAL POSITION

Key Items of the Statement of Financial Position

(million Euros) 2012 % total 2011 % total Variation

Non-current assets 159,4 18% 163,2 20% -2,4%

Current assets 745,8 82% 643,5 80% 15,9%

Total assets 905,2 100% 806,8 100% 12,2%

Non-current liabilities 276,7 31% 104,1 13% 165,7%

Current liabilities 494,4 55% 574,4 71% -13,9%

Total liabilities 771,2 85% 678,5 84% 13,6%

Total shareholders’ equity 134,1 15% 128,2 16% 4,5%

In function of that presented above, the operating result came in at a negative amount of 2.2 million Euros, very far from the positive result of 31,8 million Euros achieved in 2011.

FINANCIAL RESULTS

Financial results also worsened significantly, penalized by the increase in net financing costs with the balance between the interest obtained and interest paid coming in at -15.2 million Euros in 2012, in contrast to the -9.1 million of the previous year. The net impact of the exchange differences was contained and amounted to -0.9 million Euros but even so distant from the favourable amount achieved in 2011 of 4.0 million Euros, also contributing to the worsening of the financial results.

NET EARNINGS

The conjunction of the components previously referred to had as a con-sequence pre-tax earnings of -30.4 million Euros, an unusual amount in the history of the company, reflecting a very difficult year with very specific constraints but which, nevertheless, trace a relentless path towards placing the company in a situation that enables it to face and overcome, with moderate optimism, the challenges presented.

Considering the tax function, net earnings amounted to -24.3 million Euros versus the positive amount of 12.2 million Euros achieved in 2011.

Financial results suffered a significant aggravation

Net loss registered in 2012 is unusual in the history of

the company and has heavily penalised by non-recurrent factors and the by financial

function aggravation

31

Total assets grew 12% and current assets +16%, with an expressive increase of the account receivable from group, associated and other companies

Financial programme with impact on the liabilities structure; reduction of the current liabilities and increase of non-current liabilities

Shareholders’ equity increased 66.4 million Euros due to the merger by incorporation of Contacto

At the ASSETS level a substantial and desirable decrease in invento-ries was observed, in particular in the caption products and work-in--progress (which decreased from 26.8 million Euros to 7.8 million); additionally, receivables, namely accounts receivable (which dropped from 397.0 million Euros to 344.9 million) would have had a significant decrease were it not for the increase in accounts receivable from group, associated and other companies (that increased from 54.4 million Euros to 192.8 million Euros).

In terms of LIABILITIES, the statement of financial position shows a more favourable scheduling of the debt, with current liabilities decre-asing from 574.4 to 494.4 million Euros (significantly below current assets of 745.8 million Euros) whilst non-current liabilities increased from 104.1 to 276.7 million Euros, fundamentally due to the increase in bank loans.

This rescheduling is the result of a agreement celebrated between the company (and other Group companies), at the end of November 2012, and six financial institutions, reprogramming the respective bank loans with recourse, in a total amount of circa 275 million Euros. This opera-tion is characterized by a longer reimbursement period (maturity of 9 years, with a grace period, for capital, of 3 years) and remuneration at a moderate interest rate.

Net debt amounted to 320.1 million Euros at the end of 2012.

Regarding ShAREhOLDERS’ EQUITy, during 2012, due to the merger by incorporation of Contacto, the company’s share capital incre-ased from 50 million Euros to 66,404,000 Euros, represented by 13,280,800 ordinary shares with a par value of 5 Euros, totally held by Soares da Costa Construção, S.G.P.S., S.A..

Net shareholders’ equity as of December 31, 2012 amounted to 134.1 million Euros, increasing from the 128.2 million Euros of the previous year due to the conjugation of the following changes:

> The ordinary general meeting that approved the 2011 accounts de-liberated the distribution of a dividend in the amount of 9.6 million Euros;

> The merger of the already mentioned Contacto provoked an increase in equity of 38.9 million Euros;

> The recognition of net earnings for the year of -24.3 million Euros.

RATIOS

The evolution of the economic and financial indicators required by Or-dinance no. 274/2011, of 26 September, for the annual revalidation of the charter foreseen in the legal regime governing the construction activity, approved by Decree-Law no. 12/2004, of 9 January, had the following evolution over the last three years:

REPORT & ACCOUNTS 2012 | SOCIEDADE DE CONSTRUÇÕES SOARES DA COSTA, SA

Evolution of Current ratio and Equity/ Total assets ratio

2012 2011 2010 Min. Required

Current ratio 150.8% 112.0% 109.9% 100.0%

Equity/Total assets Ratio 14.8% 15.9% 15.1% 5.0%

PROSPECTS.5

Outlook for Portugal continues to be negative, which makes the

investment in the international markets fundamental

Important works were awarded to the company in Angola in 2012

ORDER BOOK AND AWARDS

The construction market in PORTUGAL continues with a depressive pa-norama, a context with reflects in the generalized scarcity of tenders, which inevitably leads to the degradation of prices, as well as to the reduced rate of decisions taken on tenders launched. The activity of the national construction companies cannot, therefore, be based on natio-nal production over the coming years, and it is on the international front that the short to medium-term future will be sustained.

Despite this, we present some of the awards that occurred in 2012, in Portugal: gas pipeline Mangualde-Celorico-Guarda (for REN), waste water treatment station in Paços de Sousa (for Simdouro) and reha-bilitation of the CRIZ (I and II) and the S. João das Areias bridges of EN 234 (for Estradas de Portugal).

In ANGOLA we highlight, due to its relevance and amplitude, the award of the works “project and construction of the social facilities for the employees of Angola LNG (1st phase)”, in Soyo, a project worth 252 million USD. Close to the end of the year, a consortium that includes Sociedade de Construções Soares da Costa, SA was awarded the work on the basic infrastructure of the Fútila Industrial Hub, in the province of Cabinda.Of note in this market, amongst others, are the following awards in 2012:

> Talatona Data Centre, for Movicel;

> Upgrades of Operational Bases in Soyo for Schlumberger;

> Huambo Cultural Centre, for the Provincial Government of Huambo;

> Rehabilitation and outfitting of the S. José de Cluny School Complex (phase 1), for the Provincial Government of Huambo;

> Construction of INE’s provincial offices in Malanje and in Benguela;

> Construction of the Fortaleza Shopping Centre, in Luanda.

The works referred to above are a clear and elucidative expression of the extension of the company’s territorial activity which, in turn, requi-res a significant concentration and cooperation of efforts, namely orga-nizational and logistical.

33

The activity in Mozambique continues to evidence a remarkable dynamism

The human resources adjustment should be concluded in 2013

Ambitious goal to 2013:attain a turnover close to that achieved in 2012

Over the last few years in MOZAMBIQUE, closely reflecting the develo-pment of the country itself, has come to represent a growing importan-ce to the company.

During 2012, the construction works on the bridges over the Rivers Sangaze, Pompwe, Macuca and Chidge in the Province of Sofala and on the bridges over the Rivers Muira, Tsanzabue and Nhagucha in the Pro-vince of Manica were awarded. These works, awarded by the Adminis-tração Nacional de Estradas (National Road Administration), are worth 21.7 million Euros.

Taking advantage of the capacity installed in Mozambique, a consortium in which Sociedade de Construções Soares da Costa holds a 50% parti-cipation, received an intention of award of a project in Swaziland, that consists in the construction of a road, with circa 12 Km in length and including two bridges, in the global amount of 17.6 million Euros.

PROSPECTS

As can be inferred from the national economic environment in general and the construction sector in particular investors/ managers’ expecta-tions for 2013 cannot be optimistic.

Concerning the Group, during the first months of the year the human resources adjustment process, started at the end of 2011 and profoun-dly developed in 2012, is expected to be concluded, thereby stabilizing the structure to the current and foreseeable market dimensions.

In terms of turnover, an additional activity decrease is expected in 2013 in the domestic market where, given the advanced state of the Trans-montana motorway project, with its conclusion foreseen for the third quarter, the decrease is expected to be significant.

On the other hand, a significant increase in activity is expected in the Portuguese-speaking African countries, namely in Angola and, espe-cially, in Mozambique.

As a result of this increased activity in Africa, further augmented by the contribution to turnover from other markets (namely Oman), an am-bitious objective has been set for 2013 – attaining a global turnover close to that achieved in 2012.

The increased international activity share and the significant weight of the non-recurring costs incurred in 2012, permit the assumption of a significant improvement in the EBITDA margin goal, set at close to 9%.

Level of activity in Africashould grow

REPORT & ACCOUNTS 2012 | SOCIEDADE DE CONSTRUÇÕES SOARES DA COSTA, SA

FINANCIAL STATEMENTS.6

Income Statement (2012 and 2011)

(Euro)

2012 2011

Turnover 520,046,624 605,677,038

Change in production stocks (18,882,260) (19,107,345)

Other operational income and gains:

Subsidies 40,756 -

Work for own business 2,589,319 6,793,682

Reversal of impairments 492,246 -

Other 4,800,802 15,442,323

Operational income and gains 509,087,486 608,805,698

Cost of goods sold (75,754,905) (97,662,156)

Third party supplies & services (311,501,464) (369,861,690)

Staff costs (83,832,716) (83,097,026)

Depreciation, amortisation and impairment losses (12,229,214) (12,329,052)

Provisions and fair value adjustments (16,753,601) (1,363,816)

Other operational costs

Taxes (5,947,362) (4,847,497)

Other (5,284,325) (7,817,243)

Operating costs and losses (511,303,586) (576,978,481)

Operational results (continued activity) (2,216,099) 31,827,217

Interest received 15,261,074 5,789,104

Interest paid (30,454,696) (14,928,587)

Net financing costs (15,193,622) (9,139,483)

Other financial income 6,195,529 29,102,223

Income from equity investments 160,000 20,000

Other financial costs (19,296,018) (33,273,687)

Other financial income/costs (12,940,489) (4,151,465)

Financial results (28,134,111) (13,290,948)

Earnings before taxes (30,350,210) 18,536,269

Income tax (6,014,469) (6,357,413)

Net earnings (24,335,741) 12,178,856

Earnings per share of continued activities:

Basic (1.832) 1.218

Diluted (1.832) 1.218

Earnings per share:

Basic (1.832) 1.218

Diluted (1.832) 1.218

35

Statement of Financial Position (as of December 31, 2012 and 2011)

(Euro)

ASSETS 31.12.2012 31.12.2011

NON CURRENT

Fixed tangible assets:

Land 4,800,554 4,800,554

Buildings 64,254,647 68,154,584

Basic equipment 41,030,506 47,108,996

Transport equipment 7,622,023 9,067,991

Administrative equipment 1,816,563 2,275,255

Other tangible fixed assets 11,000 36,256

Fixed assets in progress 5,116,088 3,068,157

124,651,381 134,511,792

Financial investments:

Participations in subsidiaries 283,382 20,622

Loans granted to subsidiaries 257,886 257,886

Participations in associated companies 63,359 63,359

Loans granted to associated companies 7,663,425 2,970,019

Other financial investments 10 10

8,268,061 3,311,896

Deferred taxes (assets) 607,308 1,051,219

Accounts receivable:

Retention of guarantees 25,310,652 24,373,301

Other non current assets 570,000 -

TOTAL NON CURRENT ASSETS 159,407,403 163,248,208

CURRENT

Inventories:

Raw & subsidiary materials and consumables 11,720,835 13,910,879

Finished and intermediary products 20,778,204 20,778,204

Products and work in progress 7,817,822 26,837,389

40,316,861 61,526,471

Accounts receivable:

Trade debtors 344,860,053 397,010,299

Payments in advance 16,463,487 14,343,537

Receivables from public entities 3,431,530 5,804,979

Group and associated companies and subsidiaries 192,780,843 54,367,942

Other accounts receivable 8,908,897 9,839,559

566,444,810 481,366,316

Other current assets 85,349,082 61,272,973

Cash and equivalents 53,691,834 39,358,235

TOTAL CURRENT ASSETS 745,802,587 643,523,995

TOTAL ASSETS 905,209,990 806,772,204

REPORT & ACCOUNTS 2012 | SOCIEDADE DE CONSTRUÇÕES SOARES DA COSTA, SA

(Euro)

Shareholders Equity & Liabilities 31.12.2012 31.12.2011

SHAREHOLDERS’ EQUITY

Share capital 66,404,000 50,000,000

Reserves and retained earnings:

Issue premiuns 22,174,402 22,174,402

Legal reserves 4,809,001 4,200,058

Excess of revaluation 35,796,508 35,823,889

Other reserves 34,666,432 9,335,168

Retained earnings (5,458,255) (5,485,637)

Net earnings (24,335,741) 12,178,856

TOTAL ShAREhOLDERS EQUITy 134,056,347 128,226,736

LIABILITIES

NON CURRENT

Provisions 572,481 15,000

Loans:

Bank loans 238,946,269 63,469,487

238,946,269 63,469,487

Accounts payable:

Supplier's retention of guarantee 12,979,034 9,706,410

Investments' suppliers 100,912 617,939

Payments in advance 11,114,936 19,570,325

24,194,882 29,894,674

Deferred taxes (liabilities) 13,022,918 10,756,814

TOTAL NON CURRENT LIABILITIES 276,736,550 104,135,975

CURRENT

Loans:

Bank loans 133,457,498 134,322,067

Other loans 685,659 37,005,321

134,143,157 171,327,388

Accounts payable:

Trade creditors 189,144,179 174,542,189

Investments' suppliers 845,919 2,277,351

Payments in advance 63,434,728 72,815,925

State and other public entities 1,692,520 2,058,065

Group and associated companies and subsidiaries 108,711 8,180,059

Other accounts payable 34,421,401 37,101,488

289,647,457 296,975,077

Derivative financial instruments - 1,190,357

Other current liabilities 70,626,480 104,916,669

TOTAL CURRENT LIABILITIES 494,417,093 574,409,492

TOTAL LIABILITIES 771,153,643 678,545,467

TOTAL ShAREhOLDERS EQUITy & LIABILITIES 905,209,990 806,772,204

Statement of Financial Position (as of December 31, 2012 and 2011)

BESA Luanda Headquarters // Edifício Sede do BESA Luanda Angola

complete portfolio available in //portfolio completo disponível em: www.portfolio.soaresdacosta.pt

Olympic Village Mozambique // Vila Olímpica Moçambique

complete portfolio available in //portfolio completo disponível em: www.portfolio.soaresdacosta.pt

![alekoe/Papers/Koerich_SBMICRO_1994.pdf · the properties of the series association of MOS transistors [5]. The voltage at the intermediate node of the association provides the information](https://img.document.onl/doc/110x75/5c0d44a109d3f247038d61c7/alekoepaperskoerichsbmicro1994pdf-the-properties-of-the-series-association.jpg)