Embed Size (px)

Citation preview

155Agricultural Policies, Prices and Production

Throughout the early post-colonial period inAfrica there were two basic approaches to the de-velopment of agriculture. The first aimed at�modernizing� smallholder agriculture through thepromotion of specialization, standardization andincreased use of productivity-enhancing inputs andquality control, particularly by means of integratedrural development projects. The second aimed atchannelling resources into highly capitalized in-digenous private agribusinesses and state farms.Both these approaches sought to address under-capitalization and structural constraints in Africanagriculture, but had serious shortcomings in theirdesign and implementation.

At the beginning of the past decade policyreforms were initiated in line with the view thatwhat mattered most for agricultural developmentwere market incentives. It was argued that muchof the poor performance of agriculture in SSA wasdue to excessive taxation of farmers by govern-ments. According to this view, policies designedto extract resources from agriculture in order topromote industrial development and to providesubsidized goods and services to the urbaneconomy undermined agricultural development byreducing the attractiveness of farming:

African farmers have faced the world�sheaviest rates of agricultural taxation ... ex-plicitly through producer price fixing, exporttaxes, and taxes on agricultural inputs. They

were also taxed implicitly through overval-ued exchange rates, and through high levelsof industrial protection ... The high rates oftaxation contributed to sub-Saharan Africa�salarming decline in ... agricultural growth.1

Reforms have accordingly aimed at remov-ing distortions in the incentive structure. Theinitial thrust of reforms was to realign producerprices with world prices through marketing boardsand to correct overvalued exchange rates. Fromthe late 1980s onwards there was wider recogni-tion of the importance of structural constraints,2

but in reality greater attention has been paid toderegulating agricultural markets by dismantlingthe marketing boards and allowing a greater rolefor private actors in both product and input mar-kets. Current best practice in agricultural policyis now regarded as including unsubsidized mar-ket-determined prices for both inputs and outputs,prices at border parity determined on the basis of�adequate� exchange rates, and economically neu-tral taxation of agriculture and other sectors. Onthis view, governments� responsibility is to main-tain access to markets, ensure dissemination ofinformation, and provide adequate legal and regu-latory frameworks, rather than to intervene inprices.3

However, despite intensive reforms over anumber of years, the supply response to price lib-eralization has been much less than expected,

Chapter III

AGRICULTURAL POLICIES, PRICES ANDPRODUCTION

A. Introduction

156 Trade and Development Report, 1998

raising several questions about the underlyingrationale of the reforms. First, have governments inSSA really taxed agriculture excessively, especiallycompared with the rest of the developing world?Second, how far have price reforms removed taxa-tion and resulted in greater incentives for farmers?Lastly, are price incentives the only, or even themost important, component of agricultural growthand development?4 Addressing these questions isessential for greater understanding of the factorsaffecting agricultural development, including therole of price and non-price incentives, the provisionof public goods, and structural and institutionalimpediments to supply response. That is the pur-pose of this chapter.

The next section enlarges on the brief analy-sis of the behaviour of agricultural prices presentedin TDR 1997, covering a wider range of prices,using a broader sample of countries and products,and making international comparisons.5 This isfollowed by a discussion of various factors affect-ing supply behaviour in SSA, and of the role of publicinvestment in removing structural impediments.

The analysis shows that export crops werenot always taxed through price-fixing much morein African than in other major producing countriesand that subsequent liberalization of agriculturalmarkets has not always reduced the margin betweenexport prices and producer prices. Secondly, thedomestic terms of trade for agriculture in SSAwere generally kept above the world terms of trade

between agricultural commodities and manufac-tures. This was partly due to price and subsidypolicies in favour of food crops. Since reformsbegan, agricultural terms of trade and real pro-ducer prices have generally performed better inthose countries that have continued with interven-tionist policies in agricultural marketing than inthose with more liberal policies.

The behaviour of production and exportsnoted in the last chapter has been influenced by anumber of factors, including the policy reforms.In the context of falling world prices, incentivesprovided through pricing and exchange rate re-forms have been weak. Recovery in productionin the mid-1980s coincided with the turnaroundin net resource flows (chapter I, chart 7) and therecovery in imports. Increased availability of con-sumer goods in rural areas in some cases, andpressure to satisfy basic consumption needs inothers, appear to have contributed to a positiveshort-run supply response in some countries.Where devaluations have corrected major ex-change rate misalignments, exports recovered,partly because they were diverted into officialchannels. But adjustment policies have failed toaddress a number of institutional and structuralimpediments to increasing agricultural productiv-ity and output. Removing such impedimentswould have called for increased public investmentin agricultural infrastructure and research, but thishas not been possible under fiscal retrenchmentcharacteristic of adjustment programmes.

B. Agricultural prices

1. Taxation of export crops

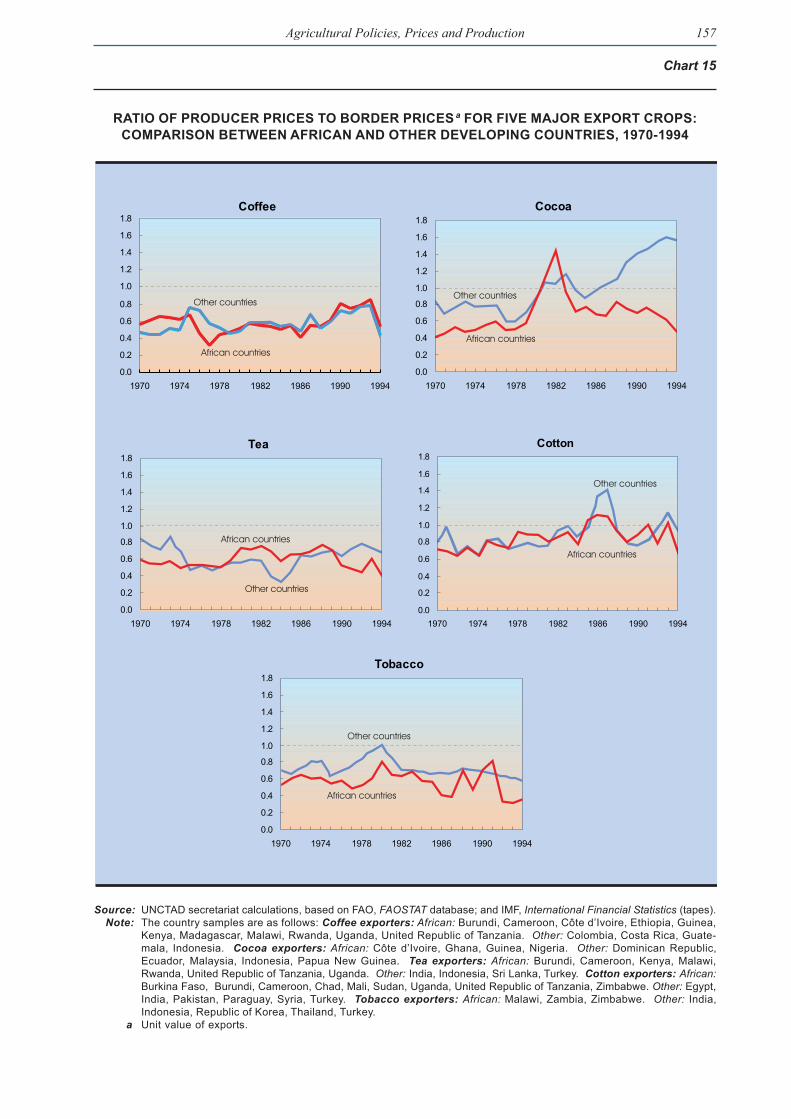

One way of addressing the question of �taxa-tion� of agriculture is to examine the marginbetween export prices (in national currency) andprices received by farmers for major export crops,and to compare the margins between major Africanand non-African exporters of these crops.6 Chart15 presents estimates of the evolution of the ratioof prices received by farmers to border (unit ex-

port) prices for coffee, cocoa, tea, cotton and to-bacco since 1970. This relative magnitude, whichis a non-adjusted nominal protection coefficient(NPC), gives a measure of the rate of surplus ex-traction from farmers by exporters.

Clearly, the margin between export and pro-ducer prices indicates a surplus extraction onlywhen producers and exporters are different enti-ties, and not when producers export directly, as in

157Agricultural Policies, Prices and Production

Chart 15

RATIO OF PRODUCER PRICES TO BORDER PRICES a FOR FIVE MAJOR EXPORT CROPS:COMPARISON BETWEEN AFRICAN AND OTHER DEVELOPING COUNTRIES, 1970-1994

Source: UNCTAD secretariat calculations, based on FAO, FAOSTAT database; and IMF, International Financial Statistics (tapes).Note: The country samples are as follows: Coffee exporters: African: Burundi, Cameroon, Côte d�Ivoire, Ethiopia, Guinea,

Kenya, Madagascar, Malawi, Rwanda, Uganda, United Republic of Tanzania. Other: Colombia, Costa Rica, Guate-mala, Indonesia. Cocoa exporters: African: Côte d�Ivoire, Ghana, Guinea, Nigeria. Other: Dominican Republic,Ecuador, Malaysia, Indonesia, Papua New Guinea. Tea exporters: African: Burundi, Cameroon, Kenya, Malawi,Rwanda, United Republic of Tanzania, Uganda. Other: India, Indonesia, Sri Lanka, Turkey. Cotton exporters: African:Burkina Faso, Burundi, Cameroon, Chad, Mali, Sudan, Uganda, United Republic of Tanzania, Zimbabwe. Other: Egypt,India, Pakistan, Paraguay, Syria, Turkey. Tobacco exporters: African: Malawi, Zambia, Zimbabwe. Other: India,Indonesia, Republic of Korea, Thailand, Turkey.

a Unit value of exports.

Cocoa

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

1970 1974 1978 1982 1986 1990 1994

Other countries

African countries

Tea

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

1970 1974 1978 1982 1986 1990 1994

Cotton

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

1970 1974 1978 1982 1986 1990 1994

Coffee

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

1970 1974 1978 1982 1986 1990 1994

Other countries

African countries

Other countries

African countries

Other countries

African countries

Tobacco

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

1970 1974 1978 1982 1986 1990 1994

Other countries

African countries

158 Trade and Development Report, 1998

the case of plantation- and TNC-based agribusiness.Moreover, it does not necessarily represent ex-plicit taxation by governments in the sense usedin conventional analysis. Such a margin also ex-ists in the case of private traders and exporters.Nevertheless, public marketing boards were theprincipal exporting agents in Africa until the early1990s, while similar institutions were less wide-spread elsewhere. In what follows, however, theterm �tax� is used to describe the margin betweenexport and producer prices regardless of the insti-tutional arrangements in the markets for exportcrops.

It should be noted that this is a crude ap-proximation of the degree of taxation since noallowance is made for marketing and transporta-tion costs and any other value added between theinitial (on-farm) and export stages of the market-ing chain. However, since domestic transactioncosts are generally higher in African countries thanin most other developing countries, the observedNPC values may overstate the extent of taxationof farmers in SSA countries compared with otherdeveloping countries. Nevertheless, there mayalso be greater value added between the farm andthe export stages among non-African exporters,accounting for part of the margin between theborder and producer prices.

The rate of taxation is not independent of theexchange rate. The border price is determined bythe nominal exchange rate and dollar prices re-ceived by exporters in international markets. Alower exchange rate would thus raise the domes-tic currency prices received by exporters. If pricespaid to farmers remain unchanged, or are raisedby less than the rate of devaluation of the currency,the tax rate will rise. Indeed, such behaviour wasobserved after the post-1986 devaluations in anumber of countries in SSA when prices receivedby farmers declined relative to unit export val-ues. However, even when devaluations lead to awidening of the margin, they tend to raise realproducer prices of export crops vis-à-vis non-tradables, thus providing incentives for exports.

It is generally agreed that the currencies ofmany SSA countries were overvalued during theperiod from the mid-1970s to the mid-1980s. How-ever, the evidence presented in chart15 does notsupport the conventional view that African pro-ducers have always been more heavily taxed thanthose in other developing countries through croppricing policies. Indeed, it suggests that this claim

is a gross oversimplification. A commodity-spe-cific comparison of African and non-Africanexporters presents a much more complex picture:

� For coffee, on average the ratio of producerprices to border (unit export) prices does notappear to have been very different betweenAfrican and non-African producers exceptduring 1975-1977, when the level of taxationin Africa was higher. Producer prices werearound 50 per cent of actual border prices inboth instances from 1979 to 1988, and thenincreased sharply before falling back to theirprevious levels.

� Cocoa producers in Africa were always moreheavily taxed than in other developing coun-tries, except for a brief interlude in the early1980s. Producer prices in Africa were onaverage 55 per cent below actual borderprices throughout the 1970s, against 60-80per cent for their competitors. The situationimproved in Africa briefly after 1980, butsoon deteriorated significantly when the ben-efits of devaluations were retained primarilyby exporters. Paradoxically, taxation appearsto have risen during the reform period in Af-rica. By contrast, since the late 1980s, pricesreceived by non-African cocoa producers ap-pear to have exceeded the export unit values,which suggests that exports were subsidized.

� For tea, taxation was higher in Africa at thebeginning and the end of the period underconsideration. However, unlike in the caseof cocoa, Africa had lower rates of taxationof producers for roughly half of the periodcovered. During most of the 1980s, Africanproducer prices averaged around 70 per centof border prices, whereas the ratio was gen-erally below 50 per cent for other developingcountry producers.

� Taxation of cotton appears to have been moremoderate and stable than that of tree crops,among both African and non-African produc-ers, and no major difference emerges betweenthe two groups of countries in this respect.The moderate downward trend of the tax ratesin the 1980s was reversed subsequently inboth groups of countries.

� For tobacco, the proportion of border pricesreceived by African producers has consistentlybeen lower than that received by non-African

159Agricultural Policies, Prices and Production

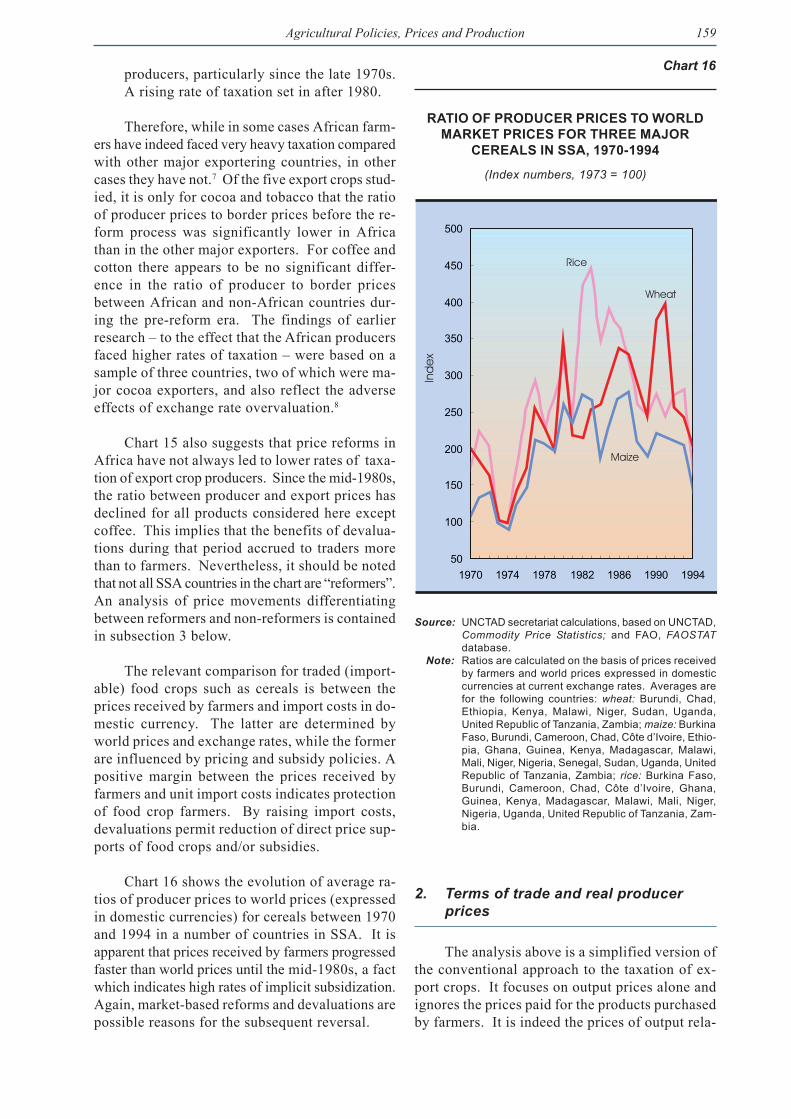

producers, particularly since the late 1970s.A rising rate of taxation set in after 1980.

Therefore, while in some cases African farm-ers have indeed faced very heavy taxation comparedwith other major exportering countries, in othercases they have not.7 Of the five export crops stud-ied, it is only for cocoa and tobacco that the ratioof producer prices to border prices before the re-form process was significantly lower in Africathan in the other major exporters. For coffee andcotton there appears to be no significant differ-ence in the ratio of producer to border pricesbetween African and non-African countries dur-ing the pre-reform era. The findings of earlierresearch � to the effect that the African producersfaced higher rates of taxation � were based on asample of three countries, two of which were ma-jor cocoa exporters, and also reflect the adverseeffects of exchange rate overvaluation.8

Chart 15 also suggests that price reforms inAfrica have not always led to lower rates of taxa-tion of export crop producers. Since the mid-1980s,the ratio between producer and export prices hasdeclined for all products considered here exceptcoffee. This implies that the benefits of devalua-tions during that period accrued to traders morethan to farmers. Nevertheless, it should be notedthat not all SSA countries in the chart are �reformers�.An analysis of price movements differentiatingbetween reformers and non-reformers is containedin subsection 3 below.

The relevant comparison for traded (import-able) food crops such as cereals is between theprices received by farmers and import costs in do-mestic currency. The latter are determined byworld prices and exchange rates, while the formerare influenced by pricing and subsidy policies. Apositive margin between the prices received byfarmers and unit import costs indicates protectionof food crop farmers. By raising import costs,devaluations permit reduction of direct price sup-ports of food crops and/or subsidies.

Chart 16 shows the evolution of average ra-tios of producer prices to world prices (expressedin domestic currencies) for cereals between 1970and 1994 in a number of countries in SSA. It isapparent that prices received by farmers progressedfaster than world prices until the mid-1980s, a factwhich indicates high rates of implicit subsidization.Again, market-based reforms and devaluations arepossible reasons for the subsequent reversal.

2. Terms of trade and real producerprices

The analysis above is a simplified version ofthe conventional approach to the taxation of ex-port crops. It focuses on output prices alone andignores the prices paid for the products purchasedby farmers. It is indeed the prices of output rela-

Chart 16

RATIO OF PRODUCER PRICES TO WORLDMARKET PRICES FOR THREE MAJOR

CEREALS IN SSA, 1970-1994

(Index numbers, 1973 = 100)

Source: UNCTAD secretariat calculations, based on UNCTAD,Commodity Price Statistics; and FAO, FAOSTATdatabase.

Note: Ratios are calculated on the basis of prices receivedby farmers and world prices expressed in domesticcurrencies at current exchange rates. Averages arefor the following countries: wheat: Burundi, Chad,Ethiopia, Kenya, Malawi, Niger, Sudan, Uganda,United Republic of Tanzania, Zambia; maize: BurkinaFaso, Burundi, Cameroon, Chad, Côte d�Ivoire, Ethio-pia, Ghana, Guinea, Kenya, Madagascar, Malawi,Mali, Niger, Nigeria, Senegal, Sudan, Uganda, UnitedRepublic of Tanzania, Zambia; rice: Burkina Faso,Burundi, Cameroon, Chad, Côte d�Ivoire, Ghana,Guinea, Kenya, Madagascar, Malawi, Mali, Niger,Nigeria, Uganda, United Republic of Tanzania, Zam-bia.

50

100

150

200

250

300

350

400

450

500

1970 1974 1978 1982 1986 1990 1994

Ind

ex

Rice

Wheat

Maize

160 Trade and Development Report, 1998

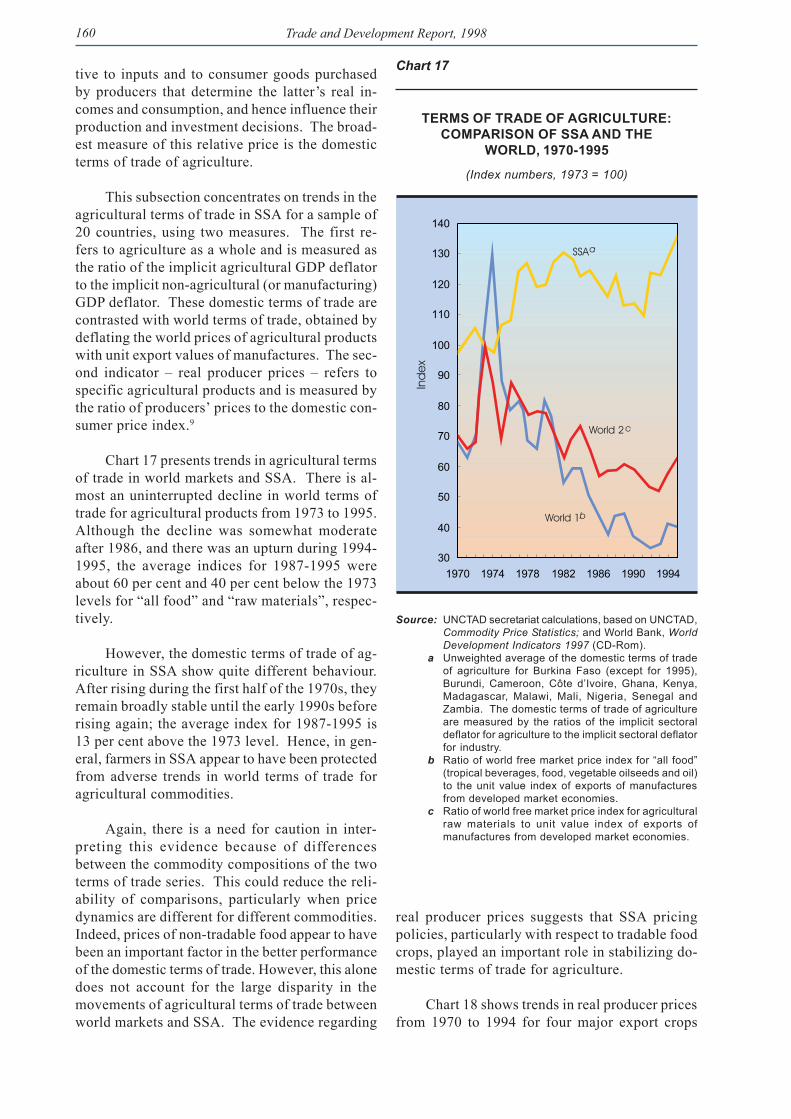

tive to inputs and to consumer goods purchasedby producers that determine the latter�s real in-comes and consumption, and hence influence theirproduction and investment decisions. The broad-est measure of this relative price is the domesticterms of trade of agriculture.

This subsection concentrates on trends in theagricultural terms of trade in SSA for a sample of20 countries, using two measures. The first re-fers to agriculture as a whole and is measured asthe ratio of the implicit agricultural GDP deflatorto the implicit non-agricultural (or manufacturing)GDP deflator. These domestic terms of trade arecontrasted with world terms of trade, obtained bydeflating the world prices of agricultural productswith unit export values of manufactures. The sec-ond indicator � real producer prices � refers tospecific agricultural products and is measured bythe ratio of producers� prices to the domestic con-sumer price index.9

Chart 17 presents trends in agricultural termsof trade in world markets and SSA. There is al-most an uninterrupted decline in world terms oftrade for agricultural products from 1973 to 1995.Although the decline was somewhat moderateafter 1986, and there was an upturn during 1994-1995, the average indices for 1987-1995 wereabout 60 per cent and 40 per cent below the 1973levels for �all food� and �raw materials�, respec-tively.

However, the domestic terms of trade of ag-riculture in SSA show quite different behaviour.After rising during the first half of the 1970s, theyremain broadly stable until the early 1990s beforerising again; the average index for 1987-1995 is13 per cent above the 1973 level. Hence, in gen-eral, farmers in SSA appear to have been protectedfrom adverse trends in world terms of trade foragricultural commodities.

Again, there is a need for caution in inter-preting this evidence because of differencesbetween the commodity compositions of the twoterms of trade series. This could reduce the reli-ability of comparisons, particularly when pricedynamics are different for different commodities.Indeed, prices of non-tradable food appear to havebeen an important factor in the better performanceof the domestic terms of trade. However, this alonedoes not account for the large disparity in themovements of agricultural terms of trade betweenworld markets and SSA. The evidence regarding

Chart 17

TERMS OF TRADE OF AGRICULTURE:COMPARISON OF SSA AND THE

WORLD, 1970-1995

(Index numbers, 1973 = 100)

Source: UNCTAD secretariat calculations, based on UNCTAD,Commodity Price Statistics; and World Bank, WorldDevelopment Indicators 1997 (CD-Rom).

a Unweighted average of the domestic terms of tradeof agriculture for Burkina Faso (except for 1995),Burundi, Cameroon, Côte d�Ivoire, Ghana, Kenya,Madagascar, Malawi, Mali, Nigeria, Senegal andZambia. The domestic terms of trade of agricultureare measured by the ratios of the implicit sectoraldeflator for agriculture to the implicit sectoral deflatorfor industry.

b Ratio of world free market price index for �all food�(tropical beverages, food, vegetable oilseeds and oil)to the unit value index of exports of manufacturesfrom developed market economies.

c Ratio of world free market price index for agriculturalraw materials to unit value index of exports ofmanufactures from developed market economies.

real producer prices suggests that SSA pricingpolicies, particularly with respect to tradable foodcrops, played an important role in stabilizing do-mestic terms of trade for agriculture.

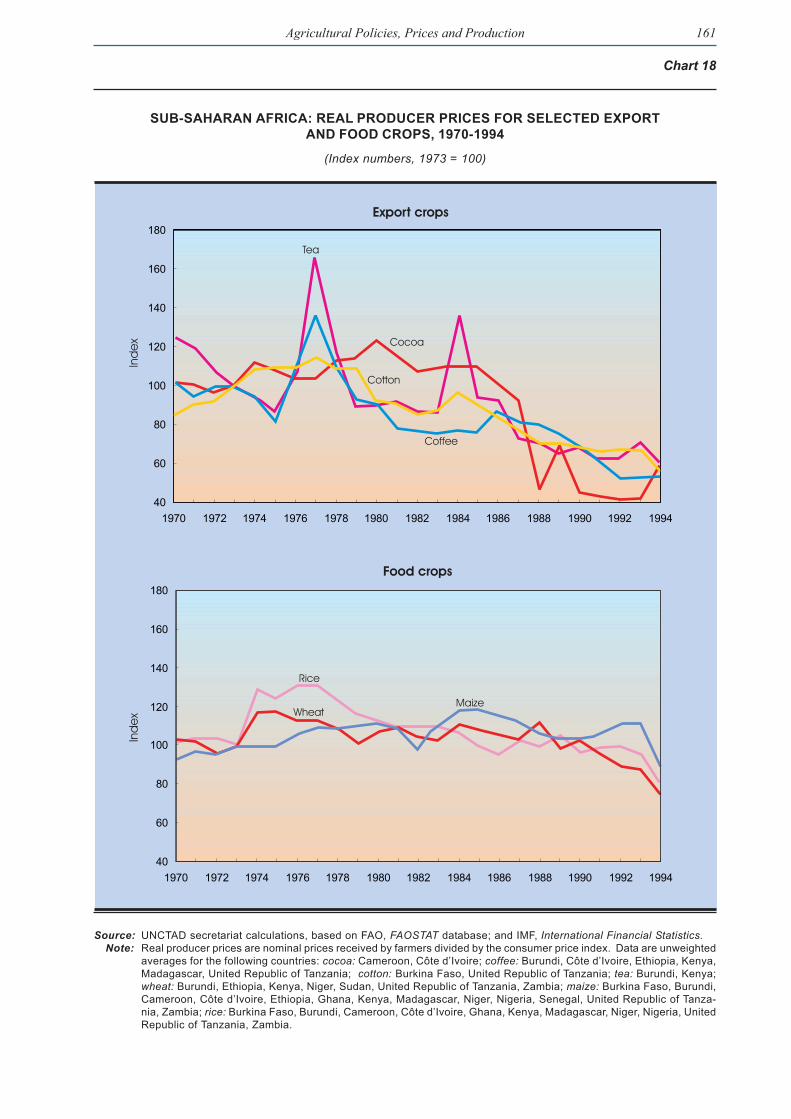

Chart 18 shows trends in real producer pricesfrom 1970 to 1994 for four major export crops

30

40

50

60

70

80

90

100

110

120

130

140

1970 1974 1978 1982 1986 1990 1994

Ind

ex

World 1b

World 2c

SSAa

161Agricultural Policies, Prices and Production

Chart 18

SUB-SAHARAN AFRICA: REAL PRODUCER PRICES FOR SELECTED EXPORTAND FOOD CROPS, 1970-1994

(Index numbers, 1973 = 100)

Source: UNCTAD secretariat calculations, based on FAO, FAOSTAT database; and IMF, International Financial Statistics.Note: Real producer prices are nominal prices received by farmers divided by the consumer price index. Data are unweighted

averages for the following countries: cocoa: Cameroon, Côte d�Ivoire; coffee: Burundi, Côte d�Ivoire, Ethiopia, Kenya,Madagascar, United Republic of Tanzania; cotton: Burkina Faso, United Republic of Tanzania; tea: Burundi, Kenya;wheat: Burundi, Ethiopia, Kenya, Niger, Sudan, United Republic of Tanzania, Zambia; maize: Burkina Faso, Burundi,Cameroon, Côte d�Ivoire, Ethiopia, Ghana, Kenya, Madagascar, Niger, Nigeria, Senegal, United Republic of Tanza-nia, Zambia; rice: Burkina Faso, Burundi, Cameroon, Côte d�Ivoire, Ghana, Kenya, Madagascar, Niger, Nigeria, UnitedRepublic of Tanzania, Zambia.

40

60

80

100

120

140

160

180

1970 1972 1974 1976 1978 1980 1982 1984 1986 1988 1990 1992 1994

40

60

80

100

120

140

160

180

1970 1972 1974 1976 1978 1980 1982 1984 1986 1988 1990 1992 1994

Ind

ex

Ind

ex

Tea

Cocoa

Coffee

Cotton

Export crops

Food crops

Rice

WheatMaize

162 Trade and Development Report, 1998

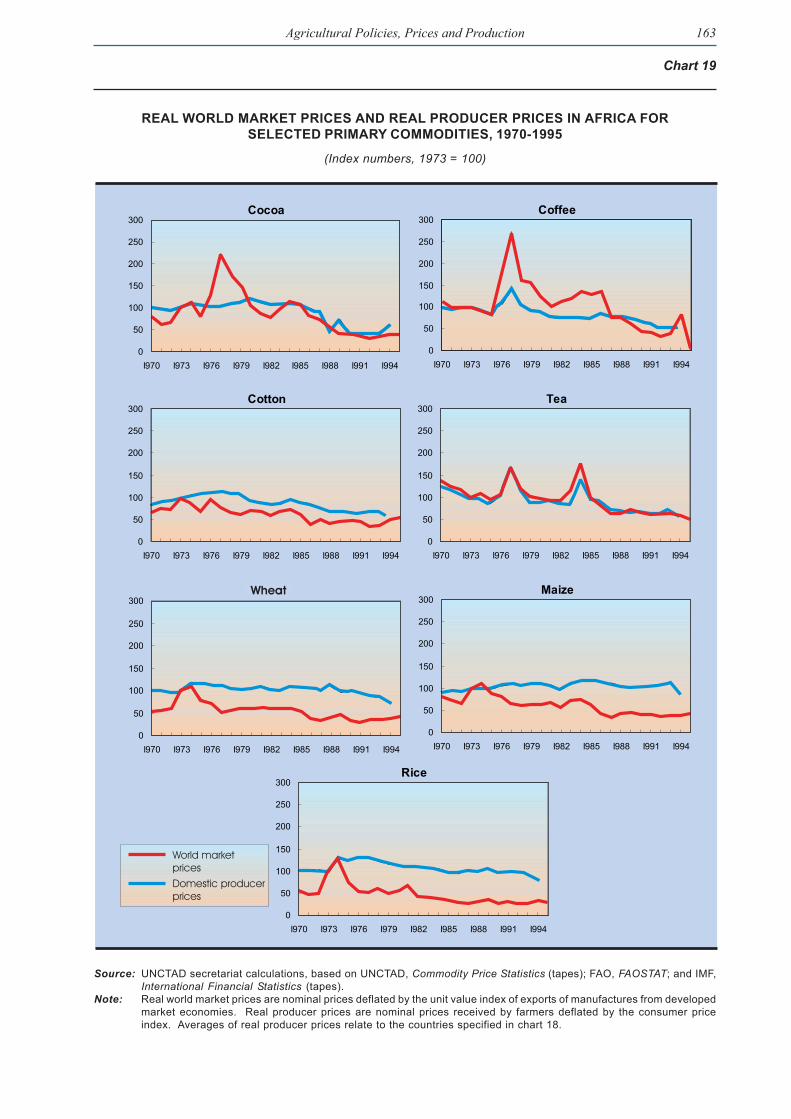

and three food crops in SSA countries. Overall,the contrast between the sharp deterioration forexport crops and a high degree of stability for foodcrops is striking. Real producer prices of cocoa,coffee, cotton and tea in the early 1990s were 40-50per cent lower than their average levels during the1970s. For cereals, real domestic prices in SSAwere relatively stable over the same period, withsome modest declines after the mid-1980s. A com-parison between domestic and international pricesshows that while in real terms, domestic prices ofexport crops generally followed the downwardtrend in international prices, for cereals those priceswere higher and more stable (chart 19).

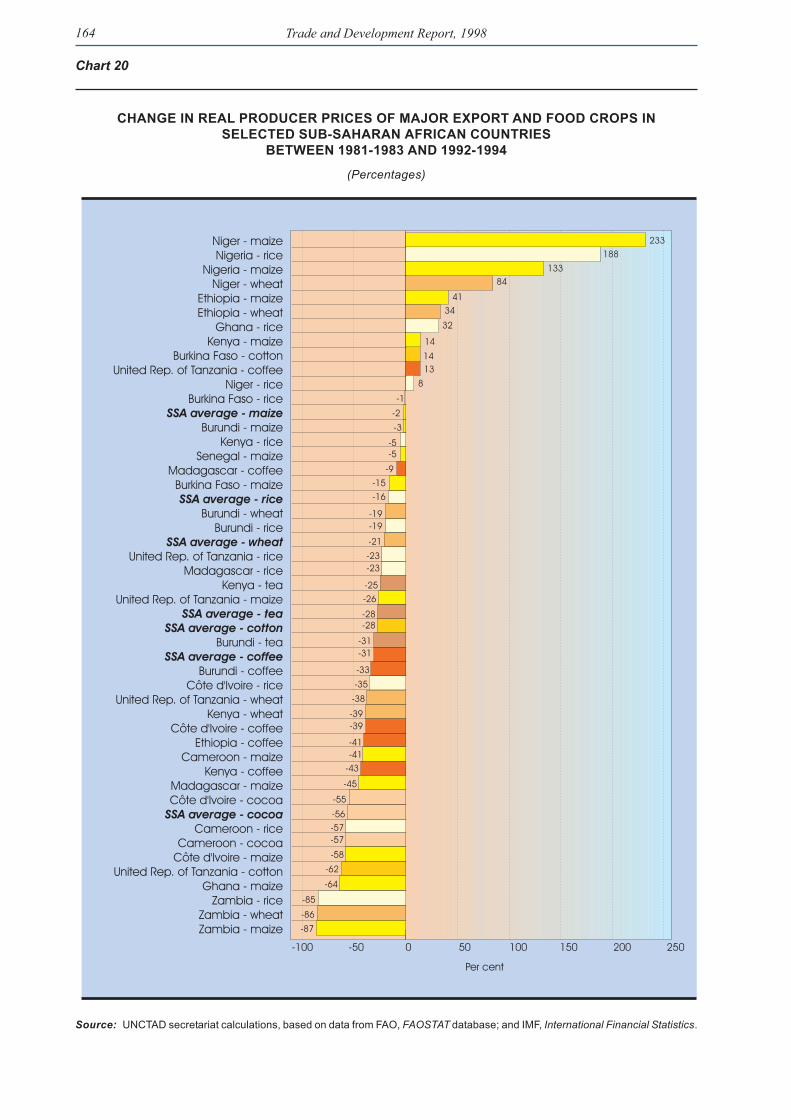

Movements in domestic terms of trade andreal producer prices are influenced by a host offactors, including developments in world marketsfor agricultural commodities and manufactures,government intervention in national output and/or input markets, and exchange rate policies.Generally, in most African countries governmentintervention until recently favoured food cropsover export crops through price supports and sub-sidies. This, together with overvalued exchangerates, kept food prices high relative to exportcrops. With market liberalization, the prices ofboth food crops and export crops have been linkedmore closely to world prices, but more so for ex-port crops. Devaluations only partly compensatedfor the downward trend in real prices of exportcrops in world markets while, as noted above, atthe same time widening the rate of taxation. Con-sequently, in general, real producer prices forexport crops fell throughout the 1980s while thosefor cereals rose or fell less. These differing trendsare shown in chart 20 for changes between the av-erage prices in 1981-1983 and in 1992-1994 for anumber of food and export crops in various coun-tries. Nevertheless, despite this broad tendency,there are important differences in the behaviourof real prices of the same food and export crops indifferent countries, reflecting in large part differencesin exchange rate policies and the extent and type ofintervention in agricultural product markets.

3. Policy reforms and agricultural prices

The findings discussed above show that de-spite widespread market-oriented agriculturalprice reforms, the past ten years have not producedsignificant improvements in relative prices andterms of trade for agriculture or lowered the rates

of taxation of farmers. A more direct way of study-ing the impact of these reforms is to compare theprice movements between �reforming� countriesand those that continued with �interventionist�policies. Here, this exercise is carried out for thesame set of prices examined above, with countriesclassified on the basis of their policy regimes asevaluated by the World Bank in its study Adjust-ment in Africa cited above.10

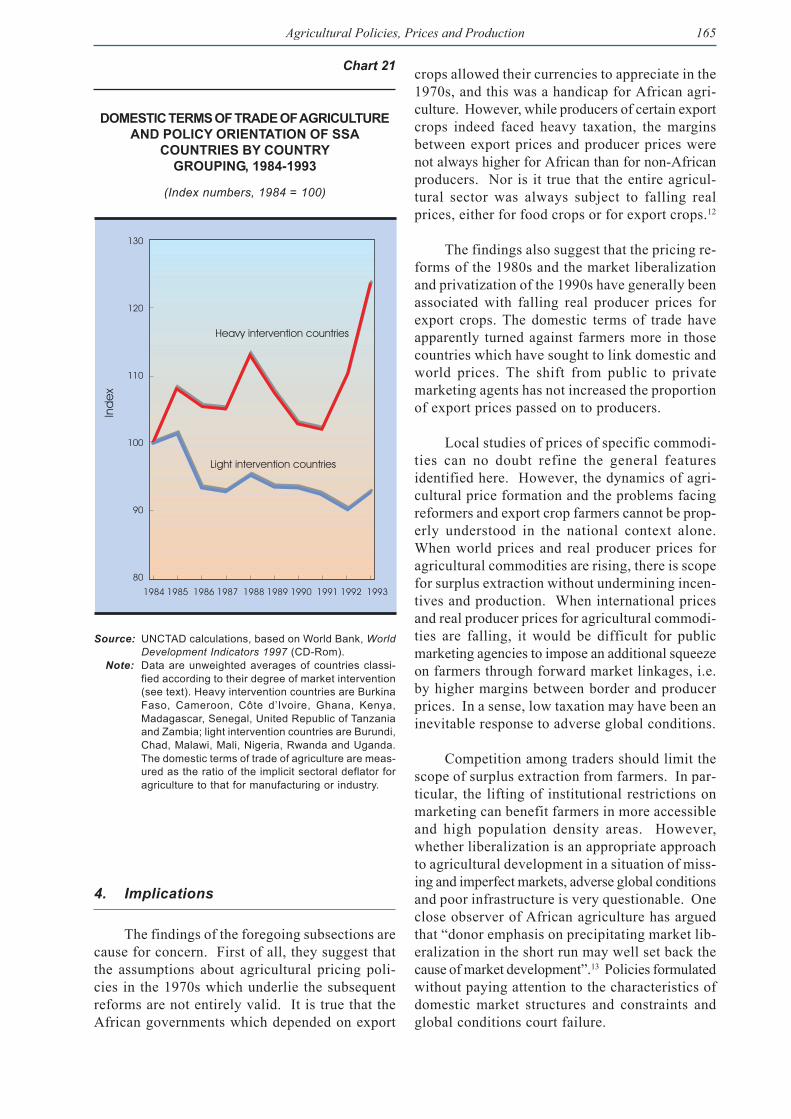

Chart 21 shows that since 1984 the overalldomestic terms of trade for agriculture have movedmuch more favourably in the �heavy intervention�countries than in the �light intervention� ones. Asof 1993, the former group had achieved an im-provement of 24 per cent compared with a 7 percent decline in the latter.

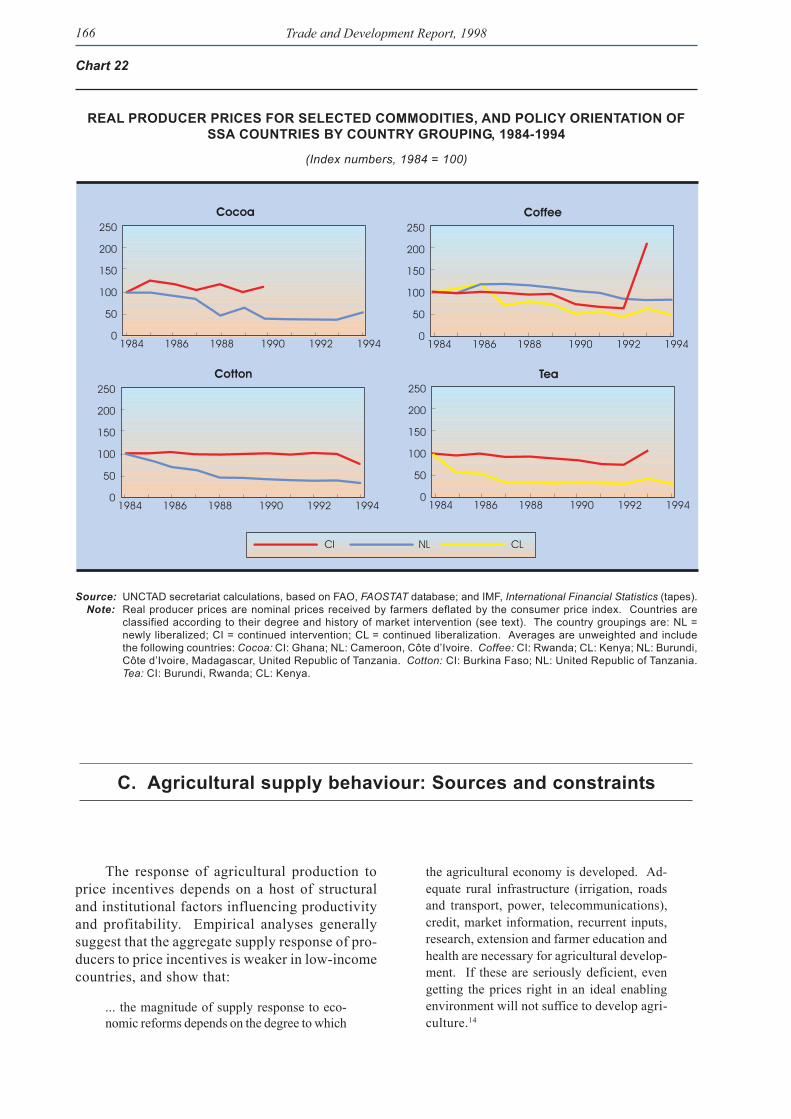

The impact of policy regimes on real pro-ducer prices is examined here by classifying majorAfrican producers of cocoa, coffee, cotton, tea andcereals into groups with �continued intervention-ist�, �continued liberal� and �newly liberalized�policy regimes vis-à-vis agricultural markets asdefined by the World Bank. For export crops, withthe exception of coffee until 1992, real producerprices have performed better since 1984 in thosecountries which have continued with intervention-ist policies in the markets for the specifiedcommodities than in those with more liberal policyregimes (chart 22). This is consistent with thefindings reported in the World Bank study,11 whichshow that in those countries which had continuedwith centralized producer pricing, there was anincrease of 4.8 per cent in the domestic real pro-ducer prices for export crops, whereas there wasa fall of 18.8 per cent in countries which hadshifted from centralized pricing to indicative pric-ing or total deregulation. For food crops, itappears that farmers in countries with a high de-gree of intervention in agricultural marketsenjoyed significantly better relative prices than theaverage, particularly during more recent years.

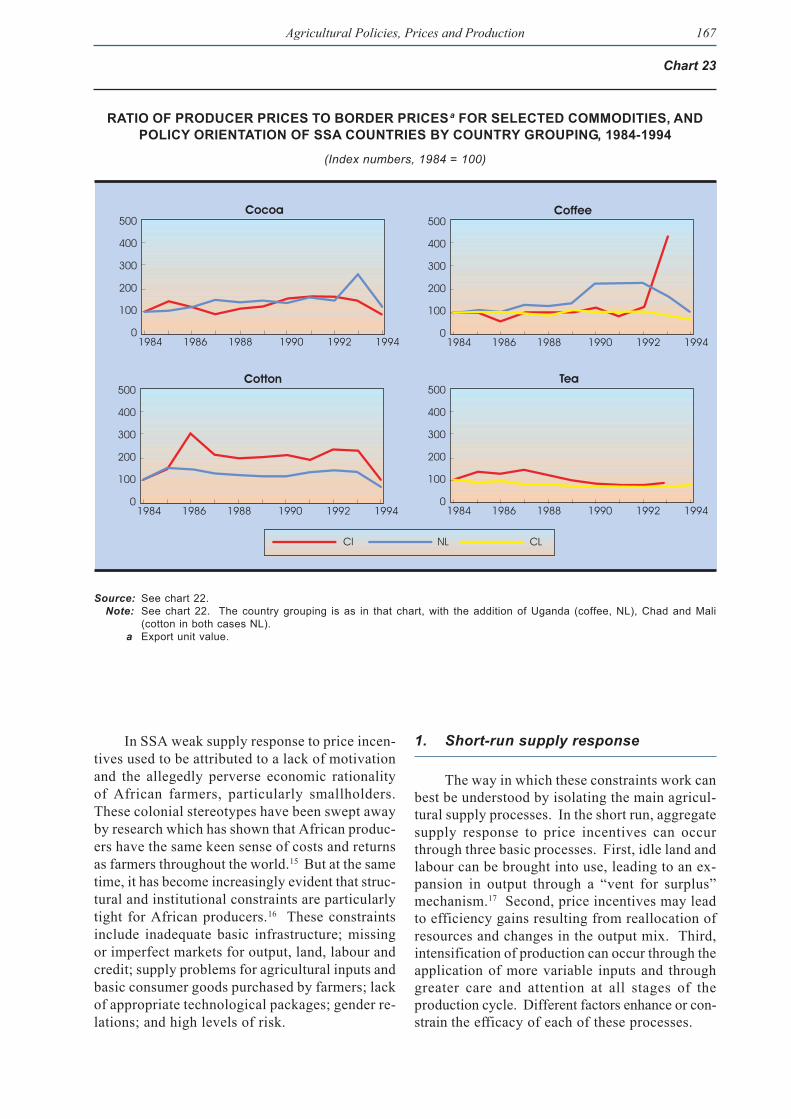

The picture is much the same regarding thetaxation of export crops, as measured by the ratioof prices received by farmers to border prices(chart 23). In countries with ongoing or newlyliberalized marketing arrangements this ratio fellfaster or rose much less rapidly than in countrieswith continued government intervention, withonce again the single exception of cocoa. Theimpact of the policy regime on relative movementsbetween import and producer prices of cereals ismore ambiguous.

163Agricultural Policies, Prices and Production

Chart 19

REAL WORLD MARKET PRICES AND REAL PRODUCER PRICES IN AFRICA FORSELECTED PRIMARY COMMODITIES, 1970-1995

(Index numbers, 1973 = 100)

Source: UNCTAD secretariat calculations, based on UNCTAD, Commodity Price Statistics (tapes); FAO, FAOSTAT; and IMF,International Financial Statistics (tapes).

Note: Real world market prices are nominal prices deflated by the unit value index of exports of manufactures from developedmarket economies. Real producer prices are nominal prices received by farmers deflated by the consumer priceindex. Averages of real producer prices relate to the countries specified in chart 18.

Cocoa

0

50

100

150

200

250

300

I970 I973 I976 I979 I982 I985 I988 I991 I994

Coffee

0

50

100

150

200

250

300

I970 I973 I976 I979 I982 I985 I988 I991 I994

Cotton

0

50

100

150

200

250

300

I970 I973 I976 I979 I982 I985 I988 I991 I994

Tea

0

50

100

150

200

250

300

I970 I973 I976 I979 I982 I985 I988 I991 I994

Wheat

0

50

100

150

200

250

300

I970 I973 I976 I979 I982 I985 I988 I991 I994

Maize

0

50

100

150

200

250

300

I970 I973 I976 I979 I982 I985 I988 I991 I994

Rice

0

50

100

150

200

250

300

I970 I973 I976 I979 I982 I985 I988 I991 I994

World marketprices

Domestic producerprices

Wheat

164 Trade and Development Report, 1998

Chart 20

CHANGE IN REAL PRODUCER PRICES OF MAJOR EXPORT AND FOOD CROPS INSELECTED SUB-SAHARAN AFRICAN COUNTRIES

BETWEEN 1981-1983 AND 1992-1994

(Percentages)

Source: UNCTAD secretariat calculations, based on data from FAO, FAOSTAT database; and IMF, International Financial Statistics.

Niger - maizeNigeria - rice

Nigeria - maizeNiger - wheat

Ethiopia - maizeEthiopia - wheat

Ghana - riceKenya - maize

Burkina Faso - cottonUnited Rep. of Tanzania - coffee

Niger - riceBurkina Faso - rice

Burundi - maizeKenya - rice

Senegal - maizeMadagascar - coffee

Burkina Faso - maize

Burundi - wheatBurundi - rice

United Rep. of Tanzania - riceMadagascar - rice

Kenya - teaUnited Rep. of Tanzania - maize

Burundi - tea

Burundi - coffeeCôte d'Ivoire - rice

United Rep. of Tanzania - wheatKenya - wheat

Côte d'Ivoire - coffeeEthiopia - coffee

Cameroon - maizeKenya - coffee

Madagascar - maizeCôte d'Ivoire - cocoa

Cameroon - riceCameroon - cocoa

Côte d'Ivoire - maizeUnited Rep. of Tanzania - cotton

Ghana - maizeZambia - rice

Zambia - wheatZambia - maize

SSA average - maize

SSA average - rice

SSA average - wheat

SSA average - tea

SSA average - cotton

SSA average - coffee

SSA average - cocoa

233

188

133

84

41

34

32

14

14

13

8

-1

-2

-3

-5-5

-9

-15

-16

-19

-19

-21

-23

-23

-25

-26

-28-28

-31

-31

-33

-35

-38

-39

-39

-41

-41

-43

-45

-55

-56

-57

-57

-58

-62

-64

-85

-86

-87

-100 -50 0 50 100 150 200 250

Per cent

165Agricultural Policies, Prices and Production

4. Implications

The findings of the foregoing subsections arecause for concern. First of all, they suggest thatthe assumptions about agricultural pricing poli-cies in the 1970s which underlie the subsequentreforms are not entirely valid. It is true that theAfrican governments which depended on export

crops allowed their currencies to appreciate in the1970s, and this was a handicap for African agri-culture. However, while producers of certain exportcrops indeed faced heavy taxation, the marginsbetween export prices and producer prices werenot always higher for African than for non-Africanproducers. Nor is it true that the entire agricul-tural sector was always subject to falling realprices, either for food crops or for export crops.12

The findings also suggest that the pricing re-forms of the 1980s and the market liberalizationand privatization of the 1990s have generally beenassociated with falling real producer prices forexport crops. The domestic terms of trade haveapparently turned against farmers more in thosecountries which have sought to link domestic andworld prices. The shift from public to privatemarketing agents has not increased the proportionof export prices passed on to producers.

Local studies of prices of specific commodi-ties can no doubt refine the general featuresidentified here. However, the dynamics of agri-cultural price formation and the problems facingreformers and export crop farmers cannot be prop-erly understood in the national context alone.When world prices and real producer prices foragricultural commodities are rising, there is scopefor surplus extraction without undermining incen-tives and production. When international pricesand real producer prices for agricultural commodi-ties are falling, it would be difficult for publicmarketing agencies to impose an additional squeezeon farmers through forward market linkages, i.e.by higher margins between border and producerprices. In a sense, low taxation may have been aninevitable response to adverse global conditions.

Competition among traders should limit thescope of surplus extraction from farmers. In par-ticular, the lifting of institutional restrictions onmarketing can benefit farmers in more accessibleand high population density areas. However,whether liberalization is an appropriate approachto agricultural development in a situation of miss-ing and imperfect markets, adverse global conditionsand poor infrastructure is very questionable. Oneclose observer of African agriculture has arguedthat �donor emphasis on precipitating market lib-eralization in the short run may well set back thecause of market development�.13 Policies formulatedwithout paying attention to the characteristics ofdomestic market structures and constraints andglobal conditions court failure.

Chart 21

DOMESTIC TERMS OF TRADE OF AGRICULTUREAND POLICY ORIENTATION OF SSA

COUNTRIES BY COUNTRYGROUPING, 1984-1993

(Index numbers, 1984 = 100)

Source: UNCTAD calculations, based on World Bank, WorldDevelopment Indicators 1997 (CD-Rom).

Note: Data are unweighted averages of countries classi-fied according to their degree of market intervention(see text). Heavy intervention countries are BurkinaFaso, Cameroon, Côte d�Ivoire, Ghana, Kenya,Madagascar, Senegal, United Republic of Tanzaniaand Zambia; light intervention countries are Burundi,Chad, Malawi, Mali, Nigeria, Rwanda and Uganda.The domestic terms of trade of agriculture are meas-ured as the ratio of the implicit sectoral deflator foragriculture to that for manufacturing or industry.

1984 1985 1986 1987 1988 1989 1990 1991 1992 1993

130

120

110

100

90

80

Heavy intervention countries

Light intervention countries

Ind

ex

166 Trade and Development Report, 1998

The response of agricultural production toprice incentives depends on a host of structuraland institutional factors influencing productivityand profitability. Empirical analyses generallysuggest that the aggregate supply response of pro-ducers to price incentives is weaker in low-incomecountries, and show that:

... the magnitude of supply response to eco-nomic reforms depends on the degree to which

Chart 22

REAL PRODUCER PRICES FOR SELECTED COMMODITIES, AND POLICY ORIENTATION OFSSA COUNTRIES BY COUNTRY GROUPING, 1984-1994

(Index numbers, 1984 = 100)

Source: UNCTAD secretariat calculations, based on FAO, FAOSTAT database; and IMF, International Financial Statistics (tapes).Note: Real producer prices are nominal prices received by farmers deflated by the consumer price index. Countries are

classified according to their degree and history of market intervention (see text). The country groupings are: NL =newly liberalized; CI = continued intervention; CL = continued liberalization. Averages are unweighted and includethe following countries: Cocoa: CI: Ghana; NL: Cameroon, Côte d�Ivoire. Coffee: CI: Rwanda; CL: Kenya; NL: Burundi,Côte d�Ivoire, Madagascar, United Republic of Tanzania. Cotton: CI: Burkina Faso; NL: United Republic of Tanzania.Tea: CI: Burundi, Rwanda; CL: Kenya.

C. Agricultural supply behaviour: Sources and constraints

the agricultural economy is developed. Ad-equate rural infrastructure (irrigation, roadsand transport, power, telecommunications),credit, market information, recurrent inputs,research, extension and farmer education andhealth are necessary for agricultural develop-ment. If these are seriously deficient, evengetting the prices right in an ideal enablingenvironment will not suffice to develop agri-culture.14

250

200

150

100

50

01984 1986 1988 1990 1992 1994

Cocoa

250

200

150

100

50

01984 1986 1988 1990 1992 1994

Coffee

250

200

150

100

50

01984 1986 1988 1990 1992 1994

Cotton

250

200

150

100

50

01984 1986 1988 1990 1992 1994

Tea

CI NL CL

167Agricultural Policies, Prices and Production

Chart 23

RATIO OF PRODUCER PRICES TO BORDER PRICESa FOR SELECTED COMMODITIES, ANDPOLICY ORIENTATION OF SSA COUNTRIES BY COUNTRY GROUPING, 1984-1994

(Index numbers, 1984 = 100)

Source: See chart 22.Note: See chart 22. The country grouping is as in that chart, with the addition of Uganda (coffee, NL), Chad and Mali

(cotton in both cases NL).a Export unit value.

In SSA weak supply response to price incen-tives used to be attributed to a lack of motivationand the allegedly perverse economic rationalityof African farmers, particularly smallholders.These colonial stereotypes have been swept awayby research which has shown that African produc-ers have the same keen sense of costs and returnsas farmers throughout the world.15 But at the sametime, it has become increasingly evident that struc-tural and institutional constraints are particularlytight for African producers.16 These constraintsinclude inadequate basic infrastructure; missingor imperfect markets for output, land, labour andcredit; supply problems for agricultural inputs andbasic consumer goods purchased by farmers; lackof appropriate technological packages; gender re-lations; and high levels of risk.

1. Short-run supply response

The way in which these constraints work canbest be understood by isolating the main agricul-tural supply processes. In the short run, aggregatesupply response to price incentives can occurthrough three basic processes. First, idle land andlabour can be brought into use, leading to an ex-pansion in output through a �vent for surplus�mechanism.17 Second, price incentives may leadto efficiency gains resulting from reallocation ofresources and changes in the output mix. Third,intensification of production can occur through theapplication of more variable inputs and throughgreater care and attention at all stages of theproduction cycle. Different factors enhance or con-strain the efficacy of each of these processes.

500

400

300

200

100

01984 1986 1988 1990 1992 1994

Cocoa500

400

300

200

100

01984 1986 1988 1990 1992 1994

Coffee

500

400

300

200

100

01984 1986 1988 1990 1992 1994

Cotton500

400

300

200

100

01984 1986 1988 1990 1992 1994

Tea

CI NL CL

168 Trade and Development Report, 1998

(a) �Vent for surplus�

Production may be expanded when farmhouseholds make a greater effort and bring idleland into use in response to price incentives orgreater availability of incentive goods. Thismechanism is of historical importance in Africa,and has been widely used to explain the initialsurge in newly introduced export crops � coffee,cotton, cocoa, groundnuts and palm nuts � whichoccurred with the first wave of globalization atthe turn of this century. It is likely that part of theshort-run supply response to policy reforms wasdue to �vent for surplus� effects. There was awidespread tendency among commercially ori-ented smallholders in a number of SSA countriesin the early 1980s to reduce their marketed outputbecause of the unavailability of such consumergoods as soap, textiles, matches, tea, coffee, sugar,cooking oil, tinned milk, fish, cement, metal roofsheeting, radios and bicycles, due to foreign ex-change shortages and the collapse of the domesticmanufacturing industry. The negative effects ofsuch shortages on recorded market output havebeen extensively studied in Ghana, Madagascar,Mozambique and the United Republic of Tanzania.18

When trade liberalization, import expansion, reformof the exchange rate policy and the dismantlingof price controls made incentive goods less scarcein rural areas, productive capacity was broughtback into use.

However, there are limits to such expansion.First, it is a one-off response. As a World Bank re-port on the United Republic of Tanzania remarked,agricultural growth during 1983-1990 was �a one-time phenomenon associated with a return to amarket-clearing situation in the rural economy thatcannot be expected to sustain growth in the 1990s�.19

Secondly, there may not always be unutilized re-sources. In both high and low population densitycountries, the land tenure system means that thereare pockets of high-density settlement alongsidelow-density areas where the entry of outsiders intothe local community can be limited or fraught withsocial problems. Even where there are commu-nity land resources available, poorer farmerssimply cannot farm extra land because they can-not mobilize the necessary complementary inputs.High levels of poverty mean that �farmers in mostof SSA cannot afford to keep either their labouror land idle even at very unattractive prices�.20

Nevertheless, because part of their basic con-sumption needs are market-mediated, falling realproducer prices can cause already hard-working

farmers to work even longer hours simply to sustainminimal subsistence. For the richer farmers, whatis important is the thinness of rural markets for wagelabour, which makes it difficult to hire extra labour.

An important part of the total labour in agri-culture is provided by women, and time allocationstudies show a strong gender dimension to house-hold labour constraints. Women, who are responsiblefor directly productive agricultural work as wellas for maintaining the household and reproduc-tion, have heavy work burdens. This situation isnot simply due to cultural norms, but is closelyassociated with lack of infrastructure and trans-port means, with much time being spent in fetchingwater and firewood, and carrying goods.21 Also,both men and women are affected by morbidity(sickness), which reduces production and produc-tivity; and evidence shows that the distance of therural population from health facilities reduces theiruse and leads to increases in the number of dayslost through illness.22 When there has been aswitch from food crops to export crops, inadequatenutrition can constrain supply response. As aWorld Bank report on Malawi observed, the �nu-tritional implications of extensive switching ofproduction away from non-tradable food crops intoexport crops have impeded adjustment�.23

(b) Output mix adjustment

Three main factors influence the ability offarmers to achieve efficiency gains through a re-allocation of resources. The first is the level ofcapitalization of farm operations. In semi-aridAfrica the key element for farmers is animal trac-tion (oxen or a donkey with a plough), which allowshouseholds not only to cultivate more land andenhance yields, but also to have greater flexibil-ity in reorienting production. Micro-analysis ofrecent supply behaviour in Burkina Faso shows thatfarm households responded positively to increasesin the prices of cotton and maize, two key cashcrops. By contrast, increased prices for these cropsled to a decrease in aggregate supply for farmerslimited to hoe cultivation, because cotton and maizedemand more labour than millet and sorghum.24

The second factor, which limits changes inoutput mix, is the commitment of households tomeet part of their subsistence needs through theirown production. This behaviour results from thefact that the rural food markets are thin, foodprices in rural markets are highly volatile, andthere are large margins between rural producer

169Agricultural Policies, Prices and Production

prices and consumer prices. The opportunity costof export crop production is thus the retail priceof food in rural markets. As a consequence, poorfarmers tend to grow food crops with low risksand low returns. It makes economic sense to meethousehold food needs through one�s own produc-tion, even though shifting to export crops appearsto be more rational. Evidence shows that �con-sumer prices for staple food must fall by 5-30 percent to stimulate cash cropping incentives in mostgrain deficit areas of Zimbabwe�.25

The third factor is gender relationships, whichcan reduce the flexibility of household units toreallocate resources. The rigidity of the genderdivision of labour in Africa is now perhaps over-accentuated, but it is certainly true that asymmetriesin the provision of household labour and the con-trol of income from specific crops and plots ofland significantly reduce flexibility. A typicalexample is the adoption of rice production innorthern Cameroon, where income from rice salesis controlled by men. It has been shown that manywomen preferred to work on subsistence cropseven though returns from rice cultivation werehigher.26

(c) Agricultural intensification

Another form of response to price incentives� agricultural intensification � can either be labour-based or involve both additional labour and othervariable inputs such as organic and chemical fer-tilizer on a given unit of land. The observationthat the transition from extensive slash-and-burnproduction methods to intensive farming tech-niques occurs with rising population densityhas led to the suggestion that intensification is con-strained by low population density and theconsequent lack of inducement to intensifyproduction. But although this process of intensi-fication promoted by high population density maybe relevant in a subsistence economy, in most cur-rent African conditions sustainable intensificationrequires additional capital and hence depends onassessment of profitability and risk, as well as onthe availability of credit, skills and appropriateintensification packages. All of the latter can beinfluenced by policy and, whether market-drivenor state-administered, are characterized by gen-der biases.

An important trend which has been observedin many African countries during the policy re-form is the decline in the use of purchased inputs,

particularly fertilizers. Firstly, input prices haverisen sharply with the removal of subsidies;27 andsecondly, fertilizer distribution systems have bro-ken down as private traders have not adequatelyreplaced marketing boards, particularly in supply-ing farmers in need of small quantities of fertilizerin remote areas. Once again infrastructure is akey constraint. There are also problems related tocredit markets. The marketing boards had offeredan institutional response to the problem of miss-ing private credit markets. As they had a legalmonopsony over marketed output, they could pro-vide seasonal inputs on credit against the potentialcrop as collateral. Through the interlocking ofinput supply and output marketing a larger numberof small farmers had access to both inputs andworking capital. With privatization, this systemof seasonal credit has broken down.28

These factors have had adverse consequencesso far for the maize revolution which was devel-oping in East and Southern Africa. In the 1980smajor increases in food grain production wereachieved in Kenya, Zambia and Zimbabwe throughpricing and market support policies which encour-aged farmers to adopt hybrid maize seed, resultingfrom decades of agricultural research, and toincrease fertilizer use. Policies included the ex-pansion of marketing board buying stations insmallholder areas, expansion of state credit dis-bursed to smallholders, and subsidies on inputs.In the 1990s, however, this approach came to beregarded as fiscally unsustainable. With the dis-mantling of state marketing services, reducedavailability of credit and rising real fertilizerprices, yields and production per capita stagnated,even when allowance is made for the adverse ef-fects of drought. Remoter areas of large, lowpopulation density countries can be particularlyaffected by the policy change. The transition frompan-territorial to market pricing has reduced grainprices received by smallholders in the more re-mote grain-surplus areas in the United Republicof Tanzania and Zambia. In Madagascar foodmarket liberalization has been associated with anincrease in price volatility and greater regional andseasonal price dispersions.29

In high-density areas, declining use of pur-chased inputs raises questions about the sustainabilityof intensification. Evidence from the Senegalesegroundnut basin, for example, shows that with theabolition of fertilizer subsidies and the increas-ingly difficult access to fertilizer credit, aggregateannual use of fertilizer has declined from a high

170 Trade and Development Report, 1998

of 80,000 tons in the mid-1970s to a range of20-30,000 tons during the 1980s and 1990s. Farm-ers have compensated by increasing the seed perhectare, a solution that may make sense in the shortterm, given prevailing prices of groundnuts andfertilizer, but that will have adverse ecologicalconsequences over the longer term.30

2. Investment and productivity growth

Both the removal of various structural obsta-cles to agricultural supply response and long-runtrends in productivity and output depend on thepace of investment and technological progress. Inpredominantly agricultural economies, the net ag-ricultural surplus (i.e. the agricultural value-addedminus agricultural producers� total consumption)is the major source of funding for investment bothwithin agriculture and outside. In extreme condi-tions where productivity is very low, the value-addedof the sector is barely sufficient to meet the basicsubsistence and simple reproduction needs ofagricultural producers, and there may even be in-sufficient surplus to maintain the natural resourcebase. Because of the undercapitalization of Afri-can agriculture, many African farmers are in thislow-productivity, hand-to-mouth situation. In suchsituations there can be no agricultural growth with-out an external injection of resources to increaseproductivity.

Greater understanding of how more success-ful African farmers have been able to create anagricultural surplus, and of what they do with thatsurplus, is vital to successful agricultural policiesin Africa. There is unfortunately a general lackof knowledge of private farm investment behav-iour, and the general omission of this issue inpolicy analysis which underpins agricultural re-forms has been highlighted in a recent report bythe World Bank Operations Evaluation Depart-ment with regard to its own agricultural sectorstudies:

There is no analysis of the constraints onprivate sector investment in any of the re-ports. Nevertheless all the reports stress theneed to develop an effective enabling envi-ronment that would help to induce privateinvestment. Unlike the old public produc-tion paradigm, the new market friendlypolicy line depends on private investmentto achieve rapid growth, in agriculture as inother sectors. In many countries, achieving

the needed rate of private investment in ag-riculture is a problem the Bank has notaddressed in its sector work on agriculture.31

Smallholder farm investment is primarilyfounded on the surplus generated by both on-farmand off-farm activities. The absence of individualrights to land has meant that few farm householdshave collateral for loans from formal banking in-stitutions. Private traders provide seasonal credit,tying their loans to purchase of crops, but this usu-ally entails high implicit rates of interest and islikely to be avoided unless a farmer is desperateand seeking a �hungry season� loan to guaranteethe survival of the household.32 Small farmers inthe past had access to credit provided by market-ing boards or special directed credit agencies, butwith the implementation of reforms these sourcesstarted to disappear. What is more, special directedcredit arrangements, which were an importantcomponent of donor lending, particularly by theWorld Bank, have been replaced by liberalizedfinancial intermediation and market-based inter-est rates. The previous arrangements did not reachthe poorest smallholders for whom they were of-ten designed. However, available evidence onfinancial liberalization suggests that these reformshave also been unable to increase the volume ofsavings or access to credit in rural areas exceptby those who can offer collateral.33

Under these conditions non-farm income hasbecome an even more important source for on-farm investment, directly or as collateral. Hownon-farm earnings derived from the public andprivate sector wage bill can propel agrarian capi-tal accumulation has been shown historically forKenya.34 But where urban unemployment is onthe increase, such opportunities are diminishing.Moreover, whether non-farm income is reinvestedin agriculture depends on a delicate balance of in-centives and capital requirements. These areaffected by the physical and economic environ-ment, including infrastructure and market structures,the scale and timing of non-farm income flows inrelation to farm investment needs, and intra-house-hold distribution and control of both non-farm andon-farm incomes. The persistence of a high de-gree of intersectoral dualism, which is rooted inlow agricultural productivity, has been only mar-ginally affected by agricultural price reforms.35

An important tendency observed in Africaamongst successful farmers is the diversificationof their portfolios, using net incomes from farm-

171Agricultural Policies, Prices and Production

ing to invest in trade and urban real estate, or intheir children�s education, rather than for expan-sion of agricultural production. This behaviourreflects both the relative profitability and theriskiness of investment in different sectors. Di-versification of activities in different sectorsresults from high levels of risks associated witheach of them, while shifting resources out of ag-riculture reflects the higher risks of agriculturaloperations based on climate, markets and publicpolicy. Moreover, market price risks of agricul-tural activity appear to have increased as a resultof deregulation of crop markets.36

How customary land tenure arrangements af-fect incentives for private farm investment is acritical issue. According to one view, since ten-ure insecurity undermines investment incentivesand diverts resources into unproductive litigationcosts, land registration and freehold titles are nec-essary in order to unleash agricultural investment.However, other analyses of the effects of such landreforms indicate that �in the absence of profitabletechnological options, registration will have littleeffect on investment and productivity in agricul-ture�37 and suggest that investments to improveland are actually increased under the indigenoustenure system because they can increase securityof use rights. This debate is still open, but it iscertain that the tenure system does affect the op-eration of rural labour and capital markets, andone legacy of the multiplication of land rightswhich occurred in the colonial period is that agri-cultural surplus and entrepreneurial energies aredeployed to build up access to, and command over,land and labour resources rather than to increasetheir productivity.38

The profitability of private investment inagriculture depends on public investment in in-frastructure. This includes institutional supportfor specific crops (see box 6), as well as location-specific investments in safe water, electricity,health and education facilities, and also transport.The rural transport bottleneck is a particularly im-portant constraint on private farm investmentbecause it reduces real returns and is also a sourceof product market imperfections. The density ofrural roads in Africa is very low, particularly whencompared with Asia.39 Moreover, many of theroads are in a poor state of repair because of lackof proper maintenance, motorized transport serv-ices are often in short supply and expensive, andthere is a dearth of non-motorized off-road trans-

port equipment, which is particularly importantfor delivering produce to the first point of sale.The experience of the Northern Guinea Savannaof Nigeria, a country where the rural road networkexpanded by 45 per cent between 1985 and 1992,shows how rural road investment can, in associa-tion with the discovery of locally adapted hybridvarieties of maize and demonstration effects ofrural development projects, facilitate expansionof food production.40

Because of lack of data, it is not always pos-sible to gauge how public expenditure supportingfarm investment has developed under adjustmentprogrammes. However, in many SSA countries,much of public investment expenditure in agri-culture was externally financed, often in the formof integrated rural development projects, but suchexpenditure has been declining. From availableevidence it appears that the proportion of gov-ernment expenditure going to agriculture hasremained under 10 per cent of total expenditureon average.41 This is a better indicator of urbanbias in Africa than agricultural pricing policy.

The rate of technological change in agricul-ture depends ultimately on agricultural research.Most of the problems with that research, pointedout a decade ago, are still unsolved: costs of R&Din Africa are higher than elsewhere, owing in partto the fact that programmes are still largely for-eign-funded, and the small size of countries andresearch stations, dispersion and high staff turno-ver impede the attainment of a �critical mass�. Asa result, with the notable exception of maize,�most of SSA now offers smallholders no dra-matic, immediately applicable new technology thatmight (with adequate price incentives) safely andsubstantially increase the profitability of foodfarming over large areas. While this is so, theelasticity of total farm output to currently recom-mended policy changes, including price changes,can seldom be very large�.42 These observationsare probably as true to a large extent now as theywere ten years ago. Evidence for 19 countries inSSA shows that real agricultural expenditures,which had been growing rapidly in the 1960s andmoderately in the 1970s, ceased to grow in the1980s and early 1990s. In 1991, the research ex-penditure in these countries was 0.7 per cent ofagricultural GDP. However, estimates of the re-turns to investment in maize research indicate highannual rates of return, usually in excess of 40 percent.43

172 Trade and Development Report, 1998

Box 6

PRICE AND NON-PRICE FACTORS IN COTTON DEVELOPMENT IN SSA

A comparative analysis of cotton production and exports in SSA was carried out in the late 1980sfor Cameroon, Kenya, Malawi, Nigeria, Senegal and the United Republic of Tanzania.1 It illus-trated the role of price and non-price factors in agricultural development, starting from the obser-vation that there had been a clear tendency since the early 1970s for francophone African countriesto perform better in cotton production and exports than anglophone countries (with the exceptionof Zimbabwe).

In two countries (Nigeria and the United Republic of Tanzania) price factors were found to haveplayed a major role in determining the volume of cotton production. In both countries abnormallylow relative prices of tradables favoured the production of food crops. The Dutch-disease-inducedincrease in labour cost in Nigeria and the dearth of consumer goods in the United Republic ofTanzania acted as further disincentives for the production of agricultural exportables.

However, apart from these extreme cases, differences in cotton production performance could notbe explained by differences in the evolution of real producer prices. Rather, and particularly in themore successful countries (Cameroon and Senegal), non-price factors (including research, creditand subsidized inputs) explained most of the production increase. In Senegal, they more thancompensated for the negative effect of declining producer prices.

The analysis also found that much of the difference in performance amongst the sample countrieswas due to institutional factors. In general, francophone countries appeared to benefit from bettercoordination between upstream and downstream agents in the cotton industry, thanks to the pres-ence of the Compagnie Française pour le Développement des Fibres Textiles (CFDT). The CFDTimproved vertical integration in the countries where it operated, and provided positive inputs interms of professionalism, know-how and experience with technological, market and finance condi-tions.

As a result of this key institutional difference, a distinct high-input/high-yield technological pat-tern prevailed in cotton production in the francophone countries, while the anglophone ones werestuck in a low-input/low-yield pattern. Despite the relative success of the former, the CFDT-in-spired approach was not immune to criticism, because it led to high production and administrativecosts and to an excessive and even monopolistic focus on cotton. In the anglophone countries, onthe other hand, lack of technological progress was making cotton cultivation increasingly unattrac-tive, except as a diversification and risk-minimization strategy.

The main conclusion of the analysis was that, notwithstanding the relevance of macroeconomic andsectoral pricing policies, institutional factors had been paramount in explaining inter-countrydifferences in cotton production growth. The unsatisfactory performance of cotton in an otherwiserelatively successful economy such as Kenya underlined the importance of crop- and sector-specific institutional arrangements, often rooted in part in the colonial legacy of the various coun-tries. The political influence of cotton producers was also important. Future priorities for cottondevelopment were identified as follows: to strengthen research and extension systems; to eliminateinput supply and finance bottlenecks; and to build institutions, including through regional coopera-tion and coordination.

1 U. J. Lele, N. van de Walle and M. Gbetibouo, �Cotton in Africa: An analysis of differences in perform-ance�, MADIA Discussion Paper No. 7 (Washington, D.C.: World Bank, 1989).

173Agricultural Policies, Prices and Production

As noted in the previous chapter, agriculturalproduction grew so slowly in the 1970s and early1980s that output per capita was falling. For manycountries, there was also a dip in agricultural ex-port volumes. In the mid-1980s, output picked upand the downward trend in exports was reversed,but despite these improvements, agricultural pro-duction per capita has stagnated and exportvolumes have not yet recovered to their 1970 lev-els in most countries.

How these trends are related to various poli-cies pursued under structural adjustmentprogrammes introduced in the 1980s is difficultto ascertain since these programmes combine threeelements (financing, policy design and imple-mentation). While the reduction of agriculturaltaxation through output pricing and market deregu-lation has been at the centre of adjustment policies,the reforms have also involved a wider range ofmeasures which have affected not only outputprices, but also a host of other elements such as:prices and the availability of agricultural inputs,incentive goods and rural credit; the quantity andquality of rural transport infrastructure and trans-port means; the quality and costs of health andeducation services for farmers; agricultural re-search and extension systems; opportunities forand remuneration of off-farm employment; and thelevel of food demand. The performance of Afri-can agriculture reflects the influence of thispackage of measures, as well as of the externalfinancing associated with adjustment programmes,on incentives and structural constraints on agri-cultural production, investment and productivitygrowth.

Agricultural performance is also affected bythe weather, changes in international prices andexternal demand. It is notable that the accelera-tion in the growth of agricultural output and therecovery of export volumes in the mid-1980s co-

incided with a reversal in the downward trend innet resource transfers, in large part on account ofsubstantial increases in ODA (see chapter I, chart 7).This was also associated with a shift from declin-ing to rising import volumes.

As already discussed, reforms have not al-ways succeeded in altering price structures asintended. They have often failed to reduce thetaxation of export crops or to improve the agri-cultural terms of trade and real producer prices.Moreover, reforms have not effectively tackled keystructural constraints which impede the accelera-tion of agricultural growth in many countries. Ithas been suggested that �SSA suffers from struc-tural handicaps that are impossible to remove orreduce through the standard policy reform pro-grams�.44 There are indications that some ingredientsof reforms have actually aggravated constraintson the growth of smallholder production. Majorexceptions to this situation are those countrieswhere, in the past, attempts were being made tofoster domestic capitalist agribusinesses or statefarms. In such cases, important restrictions onsmallholder choices and access to resources wereremoved. But elsewhere access to inputs and credithas not improved because input subsidies and pub-lic agricultural services (input provision, productdistribution, credit and extension) have been re-duced, and the private sector has not adequatelytaken over these functions. Moreover �the declinein donor support to rural development projects andintegrated commodity projects was accompaniedby a decline in investment in rural health, educa-tion and infrastructure facilities�,45 the more sobecause governments have been unwilling or un-able to provide the operation and maintenancefunds required to sustain investment. The declinein external aid to sub-Saharan African agriculturewas very steep during 1987-1994, when it droppedfrom $4,609 million to $1,322 million (at constant1990 prices).46

D. Adjustment policies and agricultural performance

174 Trade and Development Report, 1998

The upturn in agricultural production andexport volumes reflects greater utilization of ex-isting resources rather than an acceleration ofinvestment and productivity growth. Productionand export expansion in the mid-1980s coincidedwith a recovery in external resource flows andimports. Exchange rate adjustments and trade lib-eralization also appear to have contributed byshifting the incentives towards exports and reduc-ing shortages of incentive goods in the countryside.Moreover, given the declines in real producerprices and per capita incomes, it is possible thatthere has been a more intensive utilization ofhousehold labour.47

Currency depreciations can be expected tocause a shift from food crops to export crops sincemany food crops are not tradable. Again, incen-tives for food production vis-à-vis export cropsare weakened by the removal of subsidies and bydepressed food demand due to contractionarymonetary and fiscal policies. However, higherfood import costs associated with devaluations atthe same time encourage consumers to substitutelocal food for imports. The effects of devalua-tions on output mix between export and food cropsfor domestic consumption thus depend on the de-gree of tradability of food crops and reliance onfood imports. It appears that where a currencywas grossly overvalued and parallel currency mar-kets were pervasive, exports either declined orwere diverted into unofficial channels. In suchcases, exchange rate adjustments supported byexport promotion measures have achieved posi-tive results in spite of the downward trend in realproducer prices.48

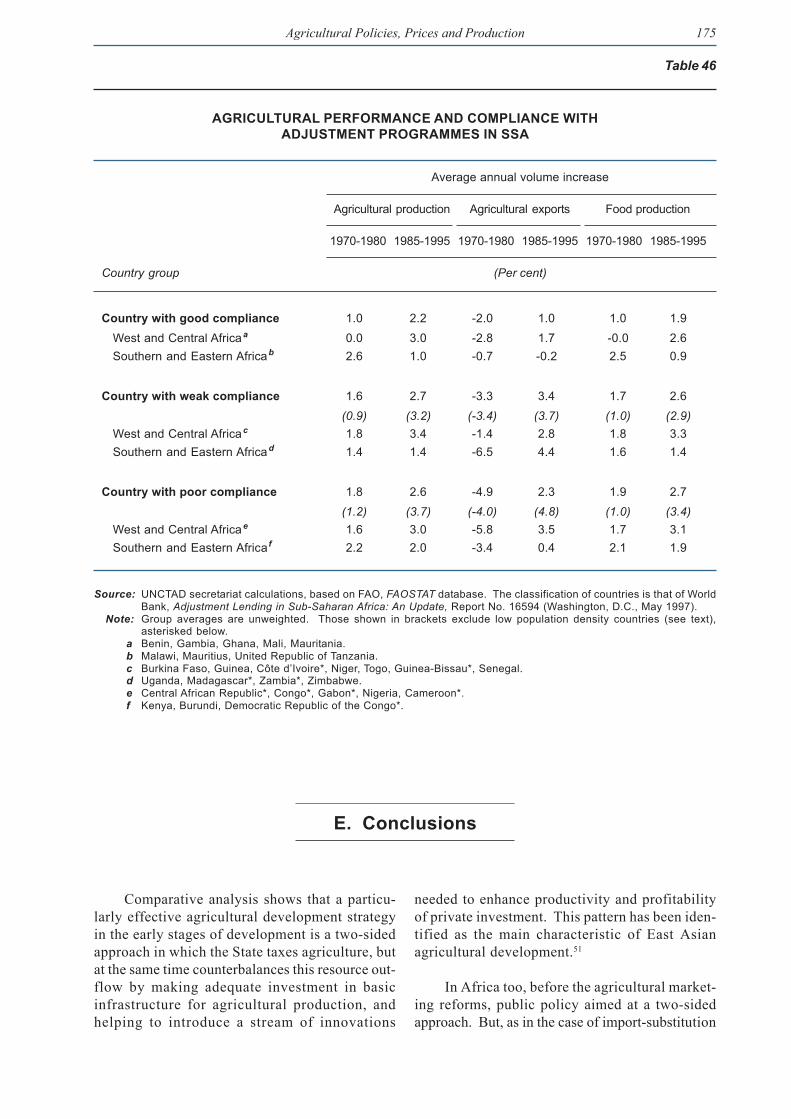

Table 46 compares post-1984 trends in totalagricultural production, export volume and foodproduction with average growth rates in the 1970sfor three groups of countries defined according tothe degree of compliance with adjustment pro-grammes. These groups are not defined simplyon the basis of pricing policies, but of their over-all compliance with conditionality with regard tomacroeconomic policy (fiscal deficit reduction,public expenditure levels, exchange rates, etc.),of their public sector management (including civilservice reform, public expenditure reform andpublic enterprise restructuring and privatization),and of their private sector development (includingfinancial sector reform, trade policy reform, regu-

latory environment, and pricing and incentives).49

Three generalizations can be made from the table:

� First, it is apparent that for all groups of coun-tries, the most significant change is in thevolume of agricultural exports. This reflectsthe partial recovery from the dip of the 1970sand early 1980s and the return of exports toofficial marketing channels. However, theimprovement in export performance is actu-ally weakest for the good compliers.

� Second, there is little difference between thegroups in terms of improvements theyachieved in growth rates of total agriculturaland total food production. However, this re-sult changes when low population densitycountries (which are not found amongst thegood compliers) are excluded. There is aclear tendency for the aggregate agriculturalgrowth rates to be lower in the post-1985period than in the 1970s in these countries.50

When the sample is limited to high and me-dium population density countries, weak andpoor compliers have a better overall perform-ance in terms of agricultural growth.

� Third, there is a major divide between South-ern and East African countries, on the onehand, and West and Central African countrieson the other. In the former, the growth ofagricultural output is lower in the post-1984period than in the 1970s in both good andpoor compliers, but it is markedly lower inthe good compliers. For West and CentralAfrica it is faster in all cases, but particu-larly so in the good compliers. Also, inSouthern and East Africa, the recovery ofagricultural exports appears to be associatedwith a decline in the rate of growth of foodproduction. Although drought may be partof the reason, the decline also reflects, asnoted above, the immediate impact of thedismantling of the state-centred approach toexpanding food grain production.

As with all exercises of this type, these re-sults must be interpreted with caution. However,they do not provide much support to the idea thatadjustment programmes have generally brought abetter policy mix for tackling incentives and struc-tural and institutional constraints across Africa.

175Agricultural Policies, Prices and Production

Comparative analysis shows that a particu-larly effective agricultural development strategyin the early stages of development is a two-sidedapproach in which the State taxes agriculture, butat the same time counterbalances this resource out-flow by making adequate investment in basicinfrastructure for agricultural production, andhelping to introduce a stream of innovations

needed to enhance productivity and profitabilityof private investment. This pattern has been iden-tified as the main characteristic of East Asianagricultural development.51

In Africa too, before the agricultural market-ing reforms, public policy aimed at a two-sidedapproach. But, as in the case of import-substitution

Table 46

AGRICULTURAL PERFORMANCE AND COMPLIANCE WITHADJUSTMENT PROGRAMMES IN SSA

Average annual volume increase

Agricultural production Agricultural exports Food production

1970-1980 1985-1995 1970-1980 1985-1995 1970-1980 1985-1995

Country group (Per cent)

Country with good compliance 1.0 2.2 -2.0 1.0 1.0 1.9West and Central Africaa 0.0 3.0 -2.8 1.7 -0.0 2.6Southern and Eastern Africab 2.6 1.0 -0.7 -0.2 2.5 0.9

Country with weak compliance 1.6 2.7 -3.3 3.4 1.7 2.6(0.9) (3.2) (-3.4) (3.7) (1.0) (2.9)

West and Central Africac 1.8 3.4 -1.4 2.8 1.8 3.3Southern and Eastern Africad 1.4 1.4 -6.5 4.4 1.6 1.4

Country with poor compliance 1.8 2.6 -4.9 2.3 1.9 2.7(1.2) (3.7) (-4.0) (4.8) (1.0) (3.4)

West and Central Africae 1.6 3.0 -5.8 3.5 1.7 3.1Southern and Eastern Africa f 2.2 2.0 -3.4 0.4 2.1 1.9

Source: UNCTAD secretariat calculations, based on FAO, FAOSTAT database. The classification of countries is that of WorldBank, Adjustment Lending in Sub-Saharan Africa: An Update, Report No. 16594 (Washington, D.C., May 1997).

Note: Group averages are unweighted. Those shown in brackets exclude low population density countries (see text),asterisked below.

a Benin, Gambia, Ghana, Mali, Mauritania.b Malawi, Mauritius, United Republic of Tanzania.c Burkina Faso, Guinea, Côte d�Ivoire*, Niger, Togo, Guinea-Bissau*, Senegal.d Uganda, Madagascar*, Zambia*, Zimbabwe.e Central African Republic*, Congo*, Gabon*, Nigeria, Cameroon*.f Kenya, Burundi, Democratic Republic of the Congo*.

E. Conclusions

176 Trade and Development Report, 1998

strategy in industry, there were serious problemsof policy design and implementation. Many gov-ernments sought to raise revenue by taxing exportcrops without ploughing part of the money backinto the sector to increase productivity. Instead,they concentrated on the promotion of food cropproduction, often subsidizing marginal areasthrough pan-territorial price support. A significantproportion of public expenditure in agriculturewent into financial subsidies, particularly for in-puts (e.g. fertilizers), credit and marketing, ratherthan into infrastructure investment and agri-cultural research to enhance agrarian capitalformation and productivity growth. More impor-tant, a large share of revenues obtained fromexport crops went into urban consumption.

The success of market-based agricultural de-velopment in Africa requires on-farm privateinvestment. This can occur only through a policywhich increases the profitability of investment andlowers risks by providing a stable environment andremoving technical and financial constraints onthe capacity and willingness to invest. Agricul-tural reforms have not succeeded in this respect.They have sought to improve profitability throughaction on one side of the equation, namely throughhigher output prices. But in practice, because theyhave been implemented in the context of imper-fect private markets and falling internationalcommodity prices, they have failed to reverse thedownward trend in real producer prices. The biasof agricultural policy reforms in favour of exportproduction has also ignored the fact that for manyfarmers it is lower food prices and improved food

distribution systems that would encourage themto grow high-value crops.

Farmers have also been squeezed because keyproduction and marketing costs � the other sideof the profitability equation � have risen rapidly:prices of fertilizers and transport costs have soaredwith devaluations and removal of subsidies. Lowerwages have not been much help because hired la-bour generally accounts for less than 20 per centof the total labour force. The dismantling of market-ing boards has increased price risks, adding to theuncertainties of rain-fed agriculture. The interlock-ing marketing systems centred on marketing boardswhich provided inputs and credit have been onlypartially replaced by private sector arrangements.

Analysis of supply behaviour has identifiedmany institutional and structural constraints.Some of these, such as low population density andagro-climatic conditions, are legacies of geogra-phy and history, and out of reach of policy, at leastin the short to medium term. Some, notably thegender division of labour and control of resources,can be quite intractable and give rise to complexpolicy decisions. But other structural constraintscan be reduced through public investment in agri-cultural research and infrastructure, and throughmeasures designed to increase farmers� skills, accessto finance and capacity to invest. The importance oftackling these policy-based constraints is now wellestablished by analysis and empirical evidence.Reorienting development policy in this directionwill require a shift from an approach based on ide-ology to one governed by pragmatism.

Notes

1 Adjustment in Africa (Washington, D.C.: WorldBank, 1994), p. 76. For an earlier formulation ofthis view see Accelerated Development in Sub-Sa-haran Africa: An Agenda for Action (Washington,D.C.: World Bank, 1982) and World DevelopmentReport 1986 (Washington, D.C.: World Bank, 1986).

2 See, in particular, H. Binswanger, �The policy re-sponse of agriculture�, in Proceedings of the WorldBank Annual Conference on Development Econom-ics (Washington, D.C.: World Bank, 1989), pp. 231-

258, together with comments by A. Braverman andA. Valdes and the floor discussion of the paper, pp.259-271.

3 See J. Meerman, Reforming Agriculture: The WorldBank Goes to Market, World Bank Operations Evalu-ation Department Study (Washington, D.C.: WorldBank, 1997), p. 70.

4 These are indeed old questions raised as part of thecriticism of the reform process described as �pricist�,i.e. something that proceeds �as if correct pricing

177Agricultural Policies, Prices and Production

policy � for farm inputs, outputs, and foreign ex-change � were (a) readily definable and attainable,(b) in general best approached by reducing state in-volvement in agricultural markets, (c) at least themost important component in, probably in most casesnecessary and sufficient for, rapid and equitable ag-ricultural growth� (M. Lipton, �Limits of price policyfor agriculture: Which way for the World Bank?�,Development Policy Review, Vol. 5, 1987, p. 201).

5 Part of the empirical results discussed in this sectionare from K. Boratav, �Movements in relative pricesin sub-Saharan Africa� (Geneva: UNCTAD, 1998),mimeo. Detailed information on the methodologyand the data used can be obtained from the UNCTADsecretariat.