Embed Size (px)

Citation preview

Companhia Mineira de Açúcar e Álcool Participações

Management Report – Harvest 14/15

COMPANHIA MINEIRA DE AÇÚCAR E ÁLCOOL

PARTICIPAÇÕES HARVEST 14/15

Management Report.

Uberaba, June 11th 2015.

Dear Shareholders,

We present the Management Report, the Financial Statements and Independent Auditors' Report for

the harvest 2014/2015, ended on March 31st, 2015 in accordance with CPCs and IFRS.

It was crushed 3.511K tons of sugarcane at 12M15, 16% higher than last crop. It was

produced 224K tons of VHP, 144K m³ of Ethanol and 269K MWH of Energy.

Gross Sales was 500.9MR$, 25.5% above than harvest 13/14 that were 399 MR$.

EBITDA of 209.7 MR$, with margin of 44%, increased 19.5% on last harvest.

Features of Harvest 14/15

COMPANHIA MINEIRA DE AÇÚCAR E ÁLCOOL

PARTICIPAÇÕES HARVEST 14/15

(THOUSAND REAIS) 12M14 12M15 Var.(%)

CMAA - CONSOLIDATED

Gross Sales 399.011 500.908 25,5%

Net Sales 372.571 476.430 27,9%

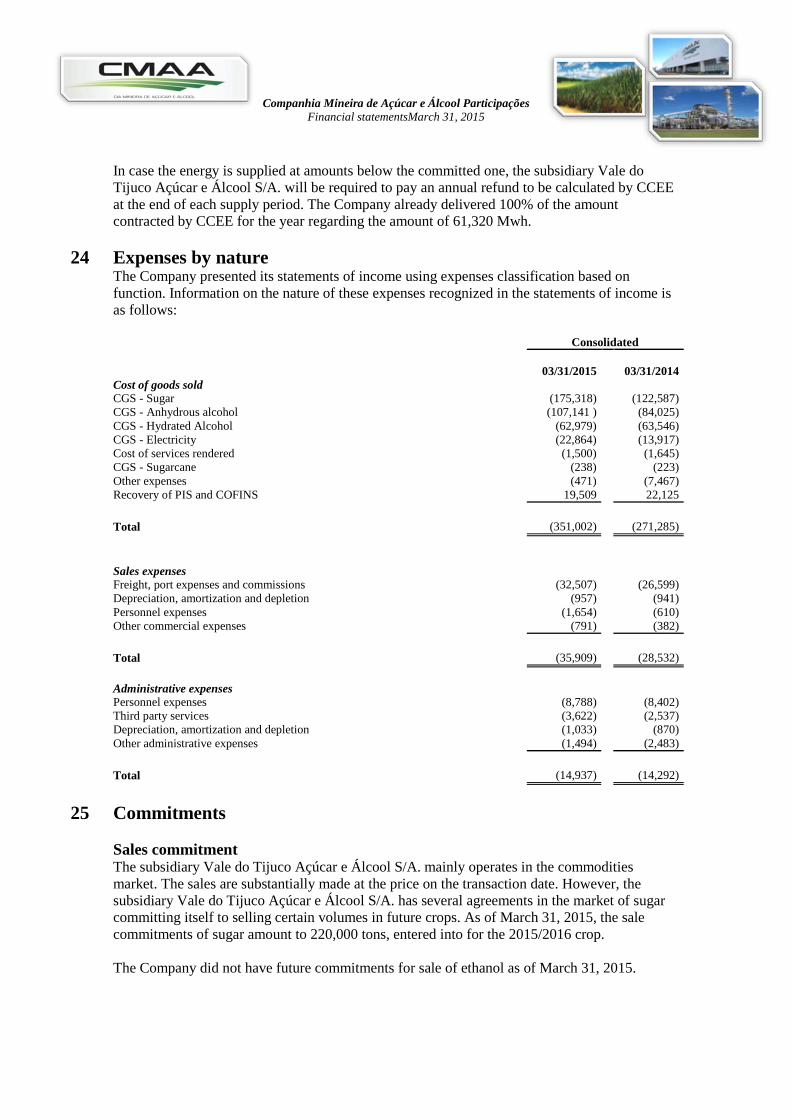

COGS -271.285 -351.002 29,4%

SG&A -37.528 -49.397 31,6%

Depreciation and Planting Amortizantion 111.100 133.692 20,3%

EBITDA* 174.858 209.722 19,9%

EBITDA Margin 46,9% 44,0% -6,2%

Net Income 8.551 6.037 -29,4%

Fair Value of Exchange Variation 100,0%

Net Adjustment Income 8.551 6.037 29,4%

Note: A form of EBITDA calculation includes depreciation, biological assets amortization and off-season amortization. In the season 13-14 the amortization of treatment ratoon cane is inside the biological assets at a value of 12,551 MR$.

Operational Data 12M14 12M15 Var.(%)

CMAA - CONSOLIDATED 12M14 12M15 Var.(%)

Crushing Sugar Cane (Thousand Tons) 3.026 3.511 16,0%

Owner 1.217 1.408 15,7%

Third Parties 1.810 2.103 16,2%

Mechanized Harvesting 100% 100% 0,0%

TRS (Kg/ton of cane) 134,8 131,1 -2,7%

Production

Sugar (Thousand Tons) 187 224 19,5%

Anhydrous Ethanol (Thousand m³) 81 90 11,5%

Hydrous Ethanol (Thousand m³) 56 54 -2,3%

Electric Energy (Thousand Mwh) 206 269 30,1%

Sales

Sugar (Thousand Tons) 187 224 19,3%

Anhydrous Ethanol (Thousand m³) 78 89 14,4%

Hydrous Ethanol (Thousand m³) 58 54 -5,8%

Electric Energy (Thousand Mwh) 206 263 27,5%

Inventory

Sugar (Thousand Tons) 0 0 100,0%

Anhydrous Ethanol (Thousand m³) 4,0 4,5 11,6%

Hydrous Ethanol (Thousand m³) 0,1 0,1 0,9%

Operatinal & Financial Features

COMPANHIA MINEIRA DE AÇÚCAR E ÁLCOOL

PARTICIPAÇÕES HARVEST 14/15

12M14 12M15 Var.(%)

Sugar Cane* 597,06 571,34 -4,3%

TRS (kg/Sugar cane tons) 133,32 136,58 2,4%

Sugar* 34,30 31,99 -6,7%

Ethanol** 25,58 26,15 2,2%

Anhydrous 11,01 10,75 -2,3%

Hydrous 14,57 15,39 5,7%

Sugar (%) 45,22 43,02 -4,9%

Ethanol (%) 54,78 56,98 4,0%

GROSS SALES COMPOSITION 12M14 12M15 Var.(%)

In Thousand Reais 12M14 12M15 Var.(%)

Internal Market 238.312 304.580 27,8%

Hydrous Ethanol 76.009 77.385 1,8%

Anhydrous Ethanol 109.604 126.842 15,7%

Sugar 0 0 0,0%

Electric Energy 48.117 99.748 107,3%

Others 4.583 606 -86,8%

External Market 160.699 196.328 22,2%

Sugar 160.699 196.328 22,2%

Hydrous Ethanol 0 0 0,0%

Total Gross Sales 399.011 500.908 25,5%

Hydrous Ethanol 76.009 77.385 1,8%

Anhydrous Ethanol 109.604 126.842 15,7%

Sugar 160.699 196.328 22,2%

Electric Energy 48.117 99.748 107,3%

Others 4.583 606 -86,8%

Source: FCSTONE/ÚNICA

*million tons

**billion de liters

Receita

According last data form ÚNICA, the Mid-

South production of harvest 14/15 reached

571 MM tons, 4.3% lower than harvest

13/14.

COMPANHIA MINEIRA DE AÇÚCAR E ÁLCOOL

PARTICIPAÇÕES HARVEST 14/15

Sugar Volume (Thousand tons) and Average Price (R$/unit)

18

7

22

4

857

878

17,0015,87

0,00

20,00

40,00

60,00

80,00

100,00

845

850

855

860

865

870

875

880

12M14 12M15

Sale Volume x Price - VHP

Volume 000T R$/ton CMAA Cts/lbp NY

At Harvest 14/15 was sold 224k

tons of sugar with average

price of R$ 878/ton

COMPANHIA MINEIRA DE AÇÚCAR E ÁLCOOL

PARTICIPAÇÕES HARVEST 14/15

Ethanol

58

54

R$ 1,32

R$ 1,42

1

1

1

1

1

2

2

35

40

45

12M14 12M15

Volume x Hydrous Price

Volume´000m³ Price R$/Liter CMAA

78

89

R$ 1,41 R$ 1,42

1

1

1

1

1

1

2

2

2

05

1015202530354045

12M14 12M15

Volume x Anydrous Price

Volume '000m³ Price R$/liter CMAA

Hydrous: it was sold 54k m3 at

harvest 14/15, reduction of 6,9%

from last crop, with average price

of R$ 1.42/liter.

Anhydrous: increase on sales

volume at 14% compared

previous harvest, being 89k m3

with average price of R$

1.42/liter.

COMPANHIA MINEIRA DE AÇÚCAR E ÁLCOOL

PARTICIPAÇÕES HARVEST 14/15

COGS 12M14 12M15 Var.(%)

In Thousand Reais 12M14 12M15 Var.(%)

Sugar 114.541 167.282 46,0%

Ethanol 135.138 160.258 18,6%

Electric Energy 13.024 21.699 66,6%

Others 8.583 1.764 -79,5%

Total COGS 271.285 351.002 29,4%

TRS Sold (Thousand Tons) 402 452 12,5%

Unit Cost (Sugar&Ethanol COGS/TRS) 622 725 16,6%

Cost of goods sold shows at the end season 14/15 an increase of 29.4% in absolute values over from

season 13/14. The variation reflexes an increase of 12.5% in sales volume. When comparing the unit cost of sugar

/ ethanol on the TRS sold, the increase is 16.6%, reflecting inflation in the costs and especially the fall of the

TRS/ton/Cana.

Costs

COMPANHIA MINEIRA DE AÇÚCAR E ÁLCOOL

PARTICIPAÇÕES HARVEST 14/15

Sales Expenses 12M14 12M15 Var.(%)

In Thousand Reais

Freight of transfers and sales 19.635 24.352 24,0%

Port Charges 5.380 6.884 28,0%

Comissions and Sales fees 1.586 1.418 -10,6%

Personnel expenses 610 864 41,6%

Depreciation 941 957 1,7%

Rent 38 77 101,7%

Others Expenses 341 1.355 297,9%

Total 28.532 35.909 25,9%

Administrative Expenses 12M14 12M15 Var.(%)

In Thousand Reais

Personnel expenses 8.415 8.342 -0,9%

General expenses and Outsourced Services 4.542 5.229 15,1%

Depreciation 926 1.033 11,6%

Tax, fees and contribuitions 260 213 -18,1%

Rent 149 121 -18,2%

Total 14.292 14.937 4,5%

Vendas: At harvest 14/15 had an increase of 25.9% compared harvest 13/14. The variation is due 19.3% of increase of transported volume of VHP to port and increasing of price of freight and port.

Administrativas: Increase of 4.5% at 12M15 compared 12M14. The variation is a result of inflation in the expenses.

Expenses

COMPANHIA MINEIRA DE AÇÚCAR E ÁLCOOL

PARTICIPAÇÕES HARVEST 14/15

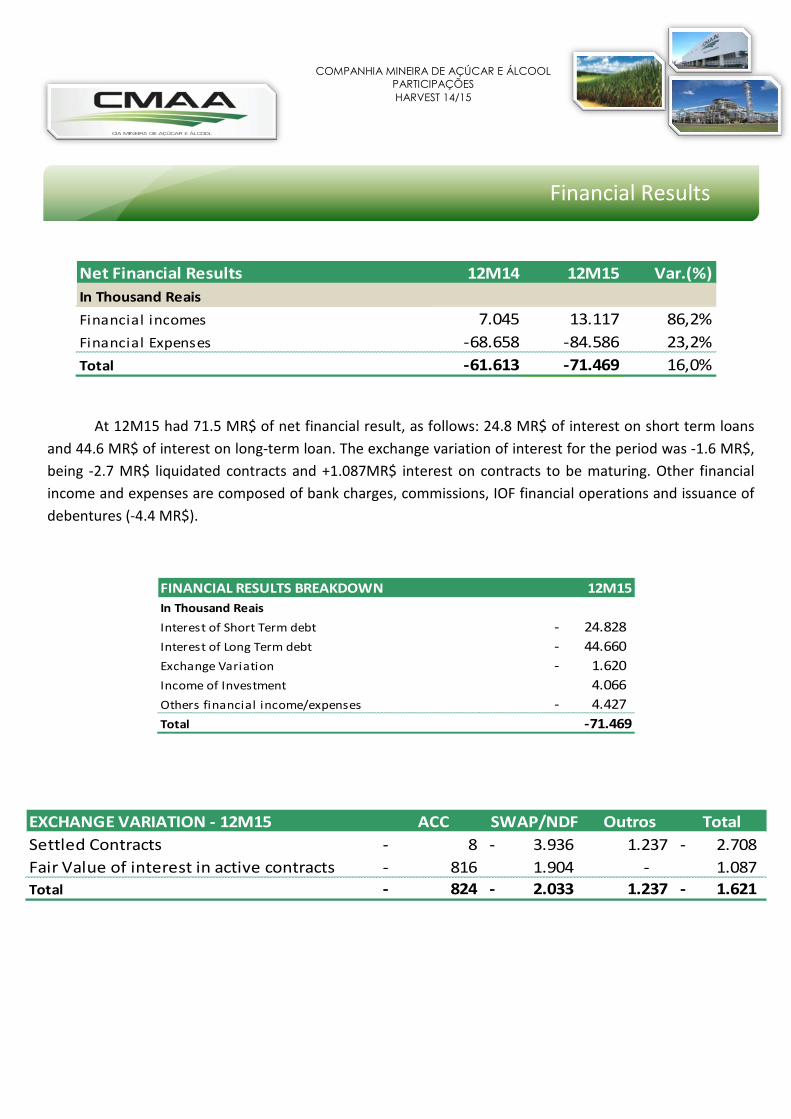

Net Financial Results 12M14 12M15 Var.(%)

In Thousand Reais

Financial incomes 7.045 13.117 86,2%

Financial Expenses -68.658 -84.586 23,2%

Total -61.613 -71.469 16,0% At 12M15 had 71.5 MR$ of net financial result, as follows: 24.8 MR$ of interest on short term loans

and 44.6 MR$ of interest on long-term loan. The exchange variation of interest for the period was -1.6 MR$,

being -2.7 MR$ liquidated contracts and +1.087MR$ interest on contracts to be maturing. Other financial

income and expenses are composed of bank charges, commissions, IOF financial operations and issuance of

debentures (-4.4 MR$).

FINANCIAL RESULTS BREAKDOWN 12M15

In Thousand Reais

Interest of Short Term debt 24.828-

Interest of Long Term debt 44.660-

Exchange Variation 1.620-

Income of Investment 4.066

Others financial income/expenses 4.427-

Total -71.469

EXCHANGE VARIATION - 12M15 ACC SWAP/NDF Outros Total

Settled Contracts 8- 3.936- 1.237 2.708-

Fair Value of interest in active contracts 816- 1.904 - 1.087

Total 824- 2.033- 1.237 1.621-

Financial Results

COMPANHIA MINEIRA DE AÇÚCAR E ÁLCOOL

PARTICIPAÇÕES HARVEST 14/15

The asset and liability position of harvest 14/15 demonstrates a negative variation in asset account due

higher volume of inventories,recoverable taxes and lower receivable accounts from clients. Negative variation

in liabilities was due suppliers account to be paid.

INDEBTEDNESS 31/3/14 31/3/15 Var.(%)

In Thousand Reais

ACC 101.111 178.996 77,0%

FINAME 212.158 193.078 -9,0%

Working Capital 187.096 147.406 -21,2%

CRA 0 99.754 100,0%

Debentures 120.923 94.181 -22,1%

Diferred Expenses -3.619 -8.916 146,4%

Gross Indebtedness 617.669 704.499 14,1%

Cash 60.562 141.409 133,5%

Net Indebtedness 557.107 563.090 1,1%

Social Capital + Reserves 203.364 203.364 0,0%

Index (Net Indebtedness/Social Capital) 2,74 2,77 1,1%

The position of net debt remained stable.

OPERATION WORKING CAPITAL 31/3/14 31/3/15 Var.(%)

In Thousand Reais

ASSETS 86.502 72.771 -15,9%

Receivables 31.253 7.369 -76,4%

Inventory 39.747 49.277 24,0%

Recoverable Taxes 15.502 16.125 4,0%

LIABILITIES 98.104 84.075 -14,3%

Suppliers 77.724 59.500 -23,4%

Salaries and Social Security Contribuitions 16.106 19.392 20,4%

Payables Taxes 4.274 5.183 21,3%

WORKING CAPITAL -11.602 -11.304 2,6%

Operational Working Capital

Indebtedness

COMPANHIA MINEIRA DE AÇÚCAR E ÁLCOOL

PARTICIPAÇÕES HARVEST 14/15

CMAA - CONSOLIDATED 12M14 12M15 Var.(%)

In Thousand Reais 12M14 12M15 Var.(%)

Sugar Cane Planting 46.593 27.378 -41,2%

Agricultural Machinary and Building 17.034 16.219 -4,8%

Industrial Equipments and Building 29.236 18.112 -38,1%

Administrative equipments/System and Others 2.295 1.903 -17,1%

Total 95.158 63.611 -33,2%

The reduction in level of investments is reflection the stability in the company growth, having almost

reached the level of full capacity in the last year.

The statements contained herein relating to the prospects of the business, estimates for operating and

financial investments are based on management's expectations and these depend substantially on changes in market conditions, the performance of the Brazilian economy and international markets and therefore are subject to change without notice.

Non-financial information, as well as other operating information has not been reviewed by the independent auditors.

Opinions of Directors on the Annual Information – 12M15

The Directors declare that reviewed, discussed and agreed with the annual Information – 12M15 and also with the conclusions expressed in the report of the independent auditors, in accordance with Article 25 of CVM Instruction 480/09.

CVM Instruction 381/03

In accordance with CVM Instruction No. 381, the Company announced that its independent auditors, KPMG, have not provided during last nine months of 2014 and first quarterly of 2015, ended March 31st of 2015, others services than those related to external audit.

The Company's policy on hiring of others services than external audit ensures that there is no conflict

of interest or loss of independence of auditors .

Investments

Legal Notice

COMPANHIA MINEIRA DE AÇÚCAR E ÁLCOOL

PARTICIPAÇÕES HARVEST 14/15

The CMAA is a public company registered with the CVM and was created to be a hub for three milling of ethanol, sugar and energy, crushing a total of 12.9 million tons per year. It is located in a region close to major consumption centers (in Triângulo Mineiro). Currently operation is Vale do Tijuco Mill, in Uberaba(MG), which was designed with total processing capacity of 4 Million Tons of sugarcane and export up to 210 MW. This plant started its first season in April 2010 with a grinding of 1.2 million tons, with the second season in 2011, with a grinding of 1.66 million tons of sugarcane, producing VHP, anhydrous ethanol, hydrous ethanol and electric energy. For the season 2013/2014 was crushed 3.026 million tons and for harvest 2014/15 crushed 3.511 million tons of sugarcane.

About CMAA

KPDS 122206

Companhia Mineira de Açúcar e Álcool Participações

Financial statements March 31, 2015

(A free translation of the original report in Portuguese)

Companhia Mineira de Açúcar e

Álcool Participações Financial statements

March 31, 2015

Contents Independent auditors' report on the financial statements 3 Balance sheets 5 Statements of income 6 Statements of comprehensive income 7 Statements of changes in shareholders' equity 8 Statements of cash flows - Indirect method 9 Statements of value added 10 Notes to the financial statements 11

KPMG Auditores Independentes, uma sociedade simples brasileira e firma-membro da rede KPMG de firmas-membro independentes e afiliadas à KPMG International Cooperative (“KPMG International”), uma entidade suíça.

KPMG Auditores Independentes, a Brazilian entity and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity.

KPMG Auditores Independentes Rua Sete de Setembro, 1.950 13560-180 - São Carlos, SP - Brasil Caixa Postal 708 13560-970 - São Carlos, SP - Brasil

Central Tel 55 (16) 2106-6700 Fax 55 (16) 2106-6767 Internet www.kpmg.com.br

Independent auditors' report on the financial statements To the Board Members and Shareholders of Companhia Mineira de Açúcar e Álcool Participações Uberaba - Minas Gerais We have examined the individual and consolidated financial statements of Companhia Mineira de Açúcar e Álcool Participações ("Company"), identified as Parent Company and Consolidated, respectively, comprising the balance sheet as of March 31, 2015 and the related statements of income, comprehensive income, changes in shareholders' equity and cash flows, for the year then ended, as well as the summary of the significant accounting practices and other explanatory notes. Management’s responsibility for the financial statements The Company's management is responsible for the preparation and adequate presentation of the individual financial statements in accordance with the accounting practices adopted in Brazil and of the consolidated financial statements in accordance with the International Financial Reporting Standards (IFRS) issued by the International Accounting Standards Board - IASB, and in accordance with the accounting practices adopted in Brazil as well as for the internal controls that it deemed necessary to enable the preparation of these financial statements free of significant distortions, regardless of whether the latter were caused by fraud or error. Responsibility of the independent auditors Our responsibility is to express an opinion on these financial statements based on our audit, undertaken in accordance with Brazilian and international auditing standards. These standards require compliance with ethical requirements by the auditors and that the audit be planned and executed with the objective of obtaining reasonable assurance that the financial statements are free from significant distortions. An audit involves the carrying out of procedures selected to obtain evidence related to the amounts and disclosures presented in the financial statements. The procedures selected depend on the auditor's judgment, including an assessment of the risks of significant distortion in the financial statements, regardless of whether the latter are caused by fraud or error. In this risk assessment, according to auditing standards, the auditor considers relevant internal controls for the preparation and adequate presentation of the financial statements of the Company, to plan the audit procedures that are appropriate in the circumstances, but not for purposes of expressing an opinion on the efficacy of these internal controls of the Company. An audit also includes the evaluation of the adequacy of adopted accounting practices and reasonability of accounting estimates made by Management, as well as an assessment of the presentation of financial statements taken as a whole. We believe that the audit evidence obtained is sufficient and appropriate to support our opinion.

Opinion on the individual financial statements In our opinion, the individual and consolidated aforementioned financial statements present fairly, in all material respects, the financial position of Companhia Mineira de Açúcar e Álcool Participações as of March 31, 2015, the performance of its operations and its cash flows, for the year then ended, in accordance with the accounting practices adopted in Brazil. Opinion on the consolidated financial statements In our opinion, the individual aforementioned financial statements present fairly, in all material respects, the financial position of Companhia Mineira de Açúcar e Álcool Participações as of March 31, 2015, the performance of its operations and its cash flows, consolidated for the year then ended, in conformity with International Financial Reporting Standards - IFRS issued by the International Accounting Standards Board (IASB) and the accounting practices adopted in Brazil. Emphasis Without modifying our opinion, we draw attention to note 1 to the consolidated financial statements, which demonstrates that the Company's consolidated current liabilities exceeded total consolidated current assets by R$ 492,938 thousand as of March 31, 2015. This condition, together with other matters, as described in note 1, indicate that a significant uncertainty exists and may raise significant doubts on the Company's going concern capacity as a going concern. Other issues Statements of added value We have also examined the individual and consolidated statements of value added (DVA) for the year ended March 31, 2015, prepared under responsibility of Company's management, whose presentation is required by Brazilian Corporate Law for publicly-held companies and as supplementary information under IFRS that do not require the presentation of a statement of value added. These statements were submitted to the same audit procedures previously described and, in our opinion, these supplementary statements are adequately presented, in all material respects, in relation to the basic financial statements taken as a whole. São Carlos, June 11, 2015 KPMG Auditores Independentes CRC 2SP014428/O-6 Original report in Portuguese signed by André Luiz Monaretti Accountant CRC 1SP160909/O-3

Com

panh

ia M

inei

ra d

e A

çúca

r e

Álc

ool P

artic

ipaç

ões

Bal

ance

she

ets

at M

arch

31,

201

5 an

d 20

14

(In

thou

sand

s of

Rea

is)

Ass

ets

Not

e03

/31/

2015

03/3

1/20

1403

/31/

2015

03/3

1/20

14Li

abili

ties

Not

e03

/31/

2015

03/3

1/20

1403

/31/

2015

03/3

1/20

14

Cas

h a

nd

cas

h e

qu

ival

ents

91

41

.40

9

60

.56

2

12

2

11

6

Loan

s an

d fi

nan

cin

g1

64

48

.17

2

33

8.7

18

-

-

T

rad

e ac

cou

nts

rec

eiva

ble

an

d o

ther

rec

eiva

ble

s1

07

.36

9

3

1.2

53

-

-

D

eben

ture

s1

79

3.0

42

2

7.4

04

-

-

In

ven

torie

s1

14

9.2

77

3

9.7

47

-

26

1

Der

ivat

ive

finan

cial

inst

rum

ents

22

31

.99

9

-

-

-

R

eco

vera

ble

taxe

s an

d c

on

trib

utio

ns

12

16

.12

5

15

.50

2

75

74

Su

pp

liers

an

d o

ther

acc

ou

nts

pay

able

18

59

.50

0

77

.72

4

18

-

O

ther

cu

rren

t ass

ets

4.8

89

1.6

34

7

6

Pro

visi

on

an

d la

bo

r ch

arge

s1

9.3

92

1

6.1

06

6

2

-

Tax

liab

ilitie

s5

.18

3

4

.27

4

1

.44

9

1

.23

0

T

otal

cur

rent

ass

ets

21

9.0

69

1

48

.69

8

20

4

45

7

Ad

van

ces

fro

m c

lien

ts4

6.7

61

2

60

-

-

O

ther

cu

rren

t lia

bili

ties

7.9

58

2.4

41

10

0

10

1

Long

-ter

m a

sset

sIn

ven

torie

s1

17

.90

8

8

.37

7

-

-

T

otal

cur

rent

liab

ilitie

s7

12

.00

7

46

6.9

27

1

.62

9

1

.33

1

T

rad

e ac

cou

nts

rec

eiva

ble

an

d o

ther

rec

eiva

ble

s1

0-

-

5

43

4

1.1

81

Ju

dic

ial d

epo

sits

88

0

41

0

-

-

Loan

s an

d fi

nan

cin

g1

61

63

.54

6

15

8.0

28

2

.85

6

4

1.3

70

R

eco

vera

ble

taxe

s an

d c

on

trib

utio

ns

12

29

.81

7

30

.10

9

-

-

Deb

entu

res

17

-

9

3.5

19

-

-

D

efer

red

inco

me

and

so

cial

co

ntr

ibu

tion

taxe

s2

02

8.1

42

3

48

-

-

D

eriv

ativ

e fin

anci

al in

stru

men

ts2

2-

6.9

09

-

-

Pro

visi

on

for

loss

in in

vest

men

ts1

3-

-

8

.60

0

8

.03

8

T

otal

non

-cur

rent

ass

ets

66

.74

7

39

.24

4

54

3

41

.18

1

Pro

visi

on

s fo

r co

ntin

gen

cies

19

81

8

1.2

08

-

-

Inve

stm

ents

13

2

2

83

.72

7

12

9.0

20

T

otal

non

-cur

rent

liab

ilitie

s1

64

.36

4

25

9.6

64

1

1.4

56

4

9.4

08

B

iolo

gica

l ass

ets

14

19

0.3

28

1

78

.41

0

-

-

Pro

pert

y, p

lant

and

equ

ipm

ent

15

46

7.2

09

4

76

.77

6

36

-

S

hare

hold

ers'

equ

ity2

1In

tang

ible

ass

ets

5.7

63

3.3

80

1.3

22

-

C

apita

l2

03

.36

4

20

3.3

64

2

03

.36

4

20

3.3

64

C

apita

l res

erve

4.1

64

4.1

64

4.1

64

4.1

64

Tot

al n

on-c

urre

nt a

sset

s7

30

.04

9

69

7.8

12

8

5.6

28

1

70

.20

1

Eq

uity

eva

luat

ion

ad

just

men

t(5

9.0

00

)

(5

.79

1)

(5

9.0

00

)

(5

.79

1)

A

ccu

mu

late

d lo

ss(7

5.7

81

)

(8

1.8

18

)

(7

5.7

81

)

(8

1.8

18

)

Tot

al s

hare

hold

ers'

equ

ity7

2.7

47

1

19

.91

9

72

.74

7

11

9.9

19

Tot

al li

abili

ties

87

6.3

71

7

26

.59

1

13

.08

5

50

.73

9

Tot

al a

sset

s9

49

.11

8

84

6.5

10

8

5.8

32

1

70

.65

8

Tot

al li

abili

ties

and

shar

ehol

ders

' equ

ity9

49

.11

8

84

6.5

10

8

5.8

32

1

70

.65

8

-

-

-

S

ee th

e ac

com

pan

yin

g n

ote

s to

the

finan

cial

sta

tem

en

ts.

Con

solid

ated

Par

ent c

ompa

nyC

onso

lidat

edP

aren

t com

pany

Companhia Mineira de Açúcar e Álcool Participações

Statements of income

Years ended March 31, 2015 and 2014

(In thousands of reais)

Note 03/31/2015 03/31/2014 03/31/2015 03/31/2014

Net operating income 23 476.430 372.571 - - Variation of the biological asset's fair value 14 1.223 7.040 - - Cost of sales and services 24 (351.002) (271.285) - -

Gross income 126.651 108.326 - -

Sales expenses 24 (35.909) (28.532) - - Administrative expenses 24 (14.937) (14.292) (1.054) (626) Other operating income 1.449 5.296 - -

(49.397) (37.528) (1.054) (626)

Income (loss) before net financial income (loss), equity in net income of subsidiaries and taxes 77.254 70.798 (1.054) (626)

Financial expenses 26 (84.586) (68.658) (273) (770) Financial income 26 13.117 7.045 10 10

Net financial income (expenses) 26 (71.469) (61.613) (264) (760)

Equity income (loss) 13 - - 7.355 9.937

Income (loss) before taxes 5.785 9.185 6.037 8.551

Current income and social contribution taxes 20 (121) (249) - - Deferred income and social contribution taxes 20 373 (385) - -

252 (634) - -

Net income for the year attributable to controlling shareholders 6.037 8.551 6.037 8.551

See the accompanying notes to the financial statements.

Consolidated Parent company

Com

panh

ia M

inei

ra d

e A

çúca

r e

Álc

ool P

artic

ipaç

ões

Sta

tem

ents

of c

ompr

ehen

sive

inco

me

Yea

rs e

nded

Mar

ch 3

1, 2

015

and

2014

(In

thou

sand

s of

Rea

is)

03/3

1/20

1503

/31/

2014

03/3

1/20

1503

/31/

2014

Inco

me

(loss

) fo

r th

e ye

ar6

.03

7

8

.55

1

6

.03

7

8

.55

1

Cas

h fl

ow

hed

ge

loss

es,

net

(53

.20

9)

(5.7

91

)

(53

.20

9)

(5.7

91

)

Tot

al c

ompr

ehen

sive

inco

me

(47

.17

2)

2.7

60

(4

7.1

72

)

2

.76

0

See

the

acco

mp

anyi

ng

no

tes

to th

e fin

anci

al s

tate

me

nts

.

Con

solid

ated

Par

ent c

ompa

ny

Com

panh

ia M

inei

ra d

e A

çúca

r e

Álc

ool P

artic

ipaç

ões

Sta

tem

ents

of c

hang

es in

sha

reho

lder

s' e

quity

Yea

rs e

nded

Mar

ch 3

1, 2

015

and

2014

(In

thou

sand

s of

Rea

is)

Not

eNot

e

Bal

ance

s at

Apr

il 1,

201

3##

192.

612

4.16

4

-

(9

0.36

9)

10

6.40

7

Oth

er c

ompr

ehen

sive

inco

me:

Net

loss

es fr

om c

ash

flow

hed

ge r

efle

cted

24-

-

(5

.791

)

-

(5

.791

)

10.7

52

-

-

-

10

.752

Net

inco

me

(loss

) fo

r th

e ye

ar-

-

-

8.55

1

8.55

1

Bal

ance

s at

Mar

ch 3

1, 2

014

##20

3.36

4

4.

164

(5

.791

)

(81.

818)

119.

919

Oth

er c

ompr

ehen

sive

inco

me:

-

N

et lo

sses

from

cas

h flo

w h

edge

ref

lect

ed24

-

-

(53.

209)

-

(5

3.20

9)

Net

inco

me

(loss

) fo

r th

e ye

ar -

-

-

6.03

7

6.03

7

Bal

ance

s at

Mar

ch 3

1, 2

015

1820

3.36

4

4.

164

(5

9.00

0)

(7

5.78

1)

72

.747

See

the

acco

mpa

nyin

g no

tes

to th

e fin

anci

al s

tate

me

nts.

Tot

al

shar

ehol

ders

' eq

uity

Cap

ital i

ncre

ase

thro

ugh

paid

-up

capi

tal p

ursu

ant t

o m

inut

es o

f mee

ting

held

on

Dec

embe

r 25

, 201

3

Cap

ital

Cap

ital

rese

rves

Equ

ity e

valu

atio

n ad

just

men

tA

ccum

ulat

ed

loss

es

Companhia Mineira de Açúcar e Álcool Participações

Statements of cash flows - Indirect method

Years ended March 31, 2015 and 2014

(In thousands of reais)

Note

03/31/2015 03/31/2014 03/31/2015 03/31/2014Cash flow from operating activitiesIncome (loss) for the year 6.037 8.551 6.037 8.551 Adjustments to reconcile income (loss):Change in fair value of biological assets (1.223) (7.040) - - Depreciation and amortization 37.809 32.816 1 - Decrease in biological assets for the crop of sugarcane 59.091 38.235 - - Off-season amortization 36.792 27.498 - - Equity income (loss) - - (7.355) (9.937) Residual value of written-off fixed assets 9.647 7.509 - - Interest on loans and financing 64.921 55.323 - - Unrealized foreign exchange variation on loans and financing (5.092) 20.268 - - Monetary variation on loans receivable from supplier - (50) - - Unrealized losses on derivative financial instruments 19.608 (974) - - Formation (reversal) of allowance for doubtful accounts 3 4 - - Formation (reversal) of provision for contingencies (390) 486 - - Deferred income and social contribution taxes (373) 385 - -

226.830 183.011 (1.317) (1.386)

Decrease/(Increase) in trade receivable and other receivables 23.881 (3.862) - - Decrease/(increase) in inventories (9.061) 4.426 261 (261) Decrease/(Increase) in loan receivable from supplier - 1.793 - - Decrease/(increase) in taxes and contributions recoverable (331) (1.777) (1) 18 Decrease/(increase) in other current assets (3.725) 4.562 - (1) Increase/(decrease) in suppliers and other accounts payable (33.586) 20.105 18 (123) Decrease/(Increase) in provision and labor charges 3.286 6.082 62 - Increase/(Decrease) in tax liabilities 909 - 219 - Decrease (increase) in advances from clients 46.501 - - - Decrease/(increase) in other current liabilities 5.505 (1.458) - 783

Cash (used in) from operating activities 260.209 - 212.882 (758) (970)

Payment of interest on loans and financing (64.992) (57.489) - -

Net cash used in operating activities 195.217 155.393 (758) (970)

Cash flow from investment activitiesFormation of biological assets (69.786) (83.862) - - Acquisition of fixed assets 31.b (44.708) (53.975) (1.359) - Acquisition of intangible assets (3.007) (1.537) - - Receipt from disposal of fixed assets 9.764 - - - Credit granting to related parties - - 40.638 (23.739)

Net cash (used in) from investment activities (107.737) (139.374) 39.279 (23.739)

Cash flow from financing activitiesLoans and financing 242.354 711.363 - - Payment of principal of loans and financing (248.987) (686.594) - - Funding with related parties - - (38.515) 24.708

Net cash (used in) from financing activities (6.633) 24.769 (38.515) 24.708

Increase (decrease) in the balance of cash and cash equivalents 80.847 40.788 6 (1)

Statement of cash and cash equivalentsCash and cash equivalents at April 1 60.562 19.774 116 117

Cash and cash equivalents em March 31 141.409 60.562 122 116

See the accompanying notes to the financial statements.

Consolidated Parent company

Companhia Mineira de Açúcar e Álcool Participações

Statements of value added

Years ended March 31, 2015 and 2014

(In thousands of Reais)

03/31/2015 03/31/2014 03/31/2015 03/31/2014

IncomeSale of merchandise, products and services 500.909 399.011 - - Other income 4.895 27.354 - - Allowance for doubtful accounts (3) (4) - -

505.801 426.361 - -

Inputs acquired from third parties (including PIS and COFINS)Cost of products, goods, and services sold (88.909) (59.120) (4) - Materials, energy, outsourced services and other (59.234) (53.229) (880) (433)Other (37.367) (20.372) (49) -

(185.510) (132.721) (933) (433)

Gross added value 320.291 293.640 (933) (433)

Depreciation and amortization (96.900) (70.656) - -

Net added value generated by the Company 223.391 222.984 (933) (433)

Added value received as transferEquity income (loss) - - 7.355 9.937 Financial income 13.117 7.045 10 10

Total added value payable 236.508 230.029 6.432 9.514

Personnel 86.481 75.178 5 2 Direct remuneration 54.850 49.910 - - Benefits 25.952 20.067 5 2 FGTS 5.679 5.201 - -

Taxes, rates and contributions 26.241 28.816 88 30 Federal 23.505 23.984 55 - State 1.049 3.140 18 30 Other taxes 1.687 1.692 15 -

Third-party capital remuneration 117.749 117.484 302 931 Interest 69.666 55.661 - - Rents 266 335 22 - Other 47.817 61.488 280 931

Remuneration of own capital 6.037 8.551 6.037 8.551 Income for the year 6.037 8.551 6.037 8.551

See the accompanying notes to the financial statements.

Consolidated Parent company

Companhia Mineira de Açúcar e Álcool Participações

Financial statementsMarch 31, 2015

Notes to the financial statements

Note Preparation basis 1 Operations 12 2 Group entities 13 3 Preparation basis 13 4 Functional currency and presentation currency 14 5 Use of estimates and judgments 14

Accounting policies 6 Measuring basis 15 7 Changes in accounting policies 16 8 Significant accounting policies 16

Assets 9 Cash and cash equivalents 26 10 Trade accounts receivable and other receivables 27 11 Inventories 27 12 Recoverable taxes and contributions 28 13 Investments 28 14 Biological assets 31 15 Property, plant and equipment 33

Liabilities and shareholders’ equity 16 Loans and financing 34 17 Debentures 36 18 Suppliers and other accounts payable 37 19 Provision for contingencies 37 20 Deferred income and social contribution taxes 38 21 Shareholders' equity 39

Financial instruments 22 Financial instruments 40

Performance of the year 23 Net operating income 49 24 Expenses by nature 51 25 Commitments 51 26 Net financial income (expenses) 52

Other information 27 Related parties 53 28 Earnings per share 54 29 Operating segments 54 30 Insurance coverage 55 31 Statements of cash flows 55 32 Environmental risks 55 33 56

Companhia Mineira de Açúcar e Álcool Participações Financial statementsMarch 31, 2015

Notes to the financial statements (In thousands of Reais)

1 Operations The Company, located at Rodovia BR 050 (KM 121) - Distrito Industrial I of Uberaba/MG, is a limited-liability company engaged in holding interest in other companies that produce, sell and export sugar, ethanol, power and other products derived from the processing of sugarcane. It obtained its registry of publicly-traded company on March 4, 2009, by means of CVM/SEP/RIC Circular Nº 001/2009, for trading of common shares on the non-organized over-the-counter market. The Company is the parent company of the following companies:

• Triângulo Mineiro Açúcar e Álcool S/A. (Triângulo Mineiro);

• Vale do Tijuco Açúcar e Álcool S/A. (Vale do Tijuco); and

• Rio Tijuco Agropecuária S/A. (Rio Tijuco). The subsidiary Triângulo Mineiro Açúcar e Álcool S/A., with head offices in Uberlândia, and the subsidiaries Vale do Tijuco Açúcar e Álcool S/A. and Rio Tijuco Agropecuária S.A., both with head offices in Uberaba, are engaged in the production, sale and export of sugar, ethanol and other products derived from the processing of sugarcane; the provision of services to third parties and the industrialization by order of the latter; the co-generation and sale of electric power, and it may exploit the planting of sugarcane in their own or third-party land; the sale of their own or third-party sugarcane; the intermediation of sale of sugarcane, and holding interest in other companies, as partner or shareholder. The subsidiary Triângulo Mineiro Açúcar e Álcool S/A. is at pre-operating phase with estimated grinding of 2.2 million tons per year for the first phase and 5.5 million for the final phase of expansion, according to the business plan. The operations of the subsidiary Vale do Tijuco Açúcar e Álcool S/A. began on April 12, 2010. The industrial plant of Vale do Tijuco Açúcar e Álcool S/A. has grinding capacity of around 4 million tons of sugarcane per year, producing sugar, anhydrous ethanol, hydrated ethanol and power, as well as the by-products fusel oil and sugarcane bagasse. The subsidiary Rio Tijuco Agropecuária S/A. is in the operating phase and its main activity is the cultivation and trading of sugarcane both in own lands and third party lands. The planting of sugarcane requires a period of up to 18 months for maturation and beginning of harvest, which usually occurs between April and November. The sale of the production occurs throughout the year and it does not suffer variations due to seasonality, but only variation of the usual market offer and demand (commodity price and foreign exchange).

Companhia Mineira de Açúcar e Álcool Participações

Financial statementsMarch 31, 2015

As a way of improving the debt profile of the Company, which, on March 31, 2015, presents the consolidated current liabilities in excess of the consolidated current assets, amounting to R$492,938, the Management is already renegotiating the balances of financing and funding to finance the activity as well as improvement of debt profile, with the main bank creditors whose debt is classified in the current liabilities in order to readjust its operating cash flow, among the main actions taken, the following measures are worth highlighting:

• Debenture debts amounting to R$93,079 were renegotiated with the banks that are classified in current liabilities of the consolidated reason why contractual clauses were not complied with. However, as mentioned in note 33 (Subsequent Events), the Group obtained a waiver from the banks in June 2015, maintaining the original classification in non-current liabilities again.

• Search for a long-term line of R$80,000 with the first-tier banks for adequacy of working capital and decrease in financial expenses.

• Obtaining the partial waiver of the ICSD index of Banco do Brasil dated March 09, 2015 and is in negotiation with the Bradesco and BDMG. The amount classified to current liabilities of this operation is R$126,734, which must be reclassified as non-current liabilities as soon as the Group obtains the waiver with the other Banks.

• If the Group needs financial resources necessary for going concern in addition to funds from banks and third parties, Shareholders may make a financial contribution.

The purpose of the strategic planning the Company has been implementing is to generate positive results in the coming years. These strategies were approved by the Company’s shareholders.

2 Group entities The consolidated financial statements include the financial statements of the Parent company Companhia Mineira de Açúcar e Álcool Participações and the following subsidiaries:

Ownership

Interest

Subsidiaries Country 2015 2014 Triângulo Mineiro Açúcar e Álcool S/A. (Triângulo Mineiro) Brazil 99.99% 99.99% Vale do Tijuco Açúcar e Álcool S/A. (Vale do Tijuco) Brazil 99.99% 99.99% Rio Tijuco Agropecuária S/A. (Rio Tijuco) Brazil 100% 100%

The individual and consolidated financial statements for the year ended March 31, 2015 comprise the Company and its subsidiaries (collectively referred to as the “Group”).

3 Preparation basis

a. Statement of conformity (regarding the International Accounting Standards Board - IFRS standards and CPC [Accounting pronouncements committee] standards) These financial statements include:

Companhia Mineira de Açúcar e Álcool Participações Financial statementsMarch 31, 2015

• The consolidated financial statements prepared according to the International financial reporting standards- IFRS issued by the International accounting standards board (IASB) and also in accordance with accounting practices adopted in Brazil in conformity with the pronouncements issued by the Accounting Pronouncement Committee - CPC; and

• The individual financial statements of the Parent company were prepared according to the accounting practices adopted in Brazil in conformity with the pronouncements issued by the Accounting pronouncement committee - CPC.

The issue of individual and consolidated financial statements was authorized by the Board of Directors in a meeting held on June 11, 2015.

b. Measuring basis The individual and consolidated financial statements were prepared based on the historical cost, except for the following items recognized in the balance sheets:

• Financial instruments measured at fair value through profit or loss, and

• Biological assets measured at fair value less sales expenses.

4 Functional currency and presentation currency These individual and consolidated financial statements are being presented in reais, functional currency of the Company and its subsidiaries. All financial information presented in Brazilian Reais has been rounded to the nearest value in thousands, except otherwise indicated.

5 Use of estimates and judgments In the preparation of individual and consolidated financial statements according to IFRS and CPC standards requires Management to make judgments, estimates and assumptions that affect the application of accounting principles and the reported amounts of assets, liabilities, income and expenses. Actual results may differ from these estimates. Estimates and assumptions are revised on an ongoing basis. Revisions to accounting estimates are recognized in the year in which the estimates are revised and in any future periods affected. The information on critical judgments that refer to accounting policies adopted that have effects on amounts recognized in the financial statements is presented in the following notes:

• Note 20 - Deferred tax assets and liabilities; and

• Note 22 - Financial instruments.

a. Uncertainties on assumptions and estimates Information on uncertainties as to assumptions and estimates that pose a significant risk of resulting in a material adjustment within the next financial year are included in the following notes:

• Note 10 - Trade accounts receivable and other receivables;

• Note 14 - Biological assets;

Companhia Mineira de Açúcar e Álcool Participações

Financial statementsMarch 31, 2015

• Note 15 - Property, plant and equipment; and

• Note 19 - Provision for contingencies.

Measurement of fair value A series of company accounting policies and disclosures requires the measurement of fair values, for financial and non-financial assets and liabilities. The Company established a control structure related to measurement of fair values. This includes a valuation team which has overall responsibility for overseeing all significant fair value measurements. The Company periodically reviews unobservable data considered significant and valuation adjustments. If third-party information, such as broker quotes or pricing services, is used to measure fair values, then the management assesses the evidence obtained from the third parties to support the conclusion that such valuations meet the CPC requirements, including the level in the fair value hierarchy in which such valuations should be classified. When measuring fair value of an asset or liability, the Company uses observable data as much as possible. Fair values are classified at different levels according to hierarchy based on information (inputs) used in valuation techniques, as follows:

• Level 1: Prices quoted (not adjusted) in active markets for identical assets and liabilities.

• Level 2: Inputs, except for quoted prices, included in Level 1 which are observable for assets or liabilities, directly (prices) or indirectly (derived from prices).

• Level 3: Inputs, for assets or liabilities, which are not based on observable market data (non-observable inputs).

The Company recognizes transfers between fair value hierarchic levels at the end of the financial statements period in which changes occurred. Additional information on the assumptions adopted in the measurement of fair values is included in the following notes:

• Note 14 - Biological assets; e

• Note 22 - Financial instruments.

6 Measuring basis The financial statements of the Company were prepared based on the historical cost, except for non-derivative financial instruments at fair value through profit or loss.

Companhia Mineira de Açúcar e Álcool Participações Financial statementsMarch 31, 2015

7 Changes in accounting policies The Company evaluated the following new pronouncements and reviews of pronouncements, with initial application on January 1, 2014:

(a) ICPC 19 / IFRIC 21 - Taxes;

(b) CPC 38/IAS 36 (Amended) - Disclosures on impairment of non-financial assets; and

(c) OCPC 7 - Notes.

The application of these amendments did not have any impact on these financial statements.

8 Significant accounting policies The accounting policies described in detail below have been consistently applied to all the years presented in these individual and consolidated financial statements.

a. Basis of consolidation

(i) Business combination among entities under joint control The measurement of transactions relating to acquisitions of subsidiaries under common control is carried out book value.

(ii) Subsidiaries The financial statements of subsidiaries are included in the consolidated financial statements as from the date they start to be controlled by the Group until the date such control ceases. The accounting policies of the subsidiaries are aligned with the policies adopted by the Group. The Company’s financial information of subsidiaries is recognized under the equity method in the individual financial statements. The financial statements of the subsidiaries on the same base date of submittal of the financial statements are used to calculate equity in the earnings and consolidation. Subsidiaries are consolidated in the consolidated financial statements.

(iii) Transactions eliminated in the consolidation Balances and transactions with subsidiaries, and any income or expenses derived from transactions with subsidiaries, are eliminated in the preparation of the consolidated financial statements. Unrealized gains originating from transactions with investee company recorded using the equity method, are eliminated against the investment in the proportion of the Company's interest in the investee company. Unrealized losses are eliminated in the same way as unrealized gains, but only up to the point where there is no evidence of loss due to impairment.

Companhia Mineira de Açúcar e Álcool Participações

Financial statementsMarch 31, 2015

b. Operating income

(i) Sale of products The operating income from sales of products in the normal course of business is measured by the fair value of the installment received or receivable. Operating income is recognized when there is convincing evidence that the risks and rewards inherent to the ownership of the assets have been transferred to the purchaser, it is probable that the financial economic benefits will flow to the Group, the related costs and potential return of goods can be reliably estimated, there is no continued involvement with the goods sold, and the amount of operating income can be reliably measured. The correct moment for the transfer of risks and benefits varies depending on the individual conditions of each sales agreement. For sugar and ethanol sales in the domestic market, transfer is normally carried out when the product is delivered in the client's premises of when it is picked up by the client in the Group's premises. For sales in the foreign market, the transfer occurs upon loading of goods in the transportation company of the seller harbor.

(ii) Sale of electricity The operating income in the ordinary course of business of the Company and its subsidiaries is measured at fair value of the consideration received or receivable. Operating income is recognized when there is convincing evidence that the most significant risks and rewards have been transferred to the purchaser, it is probable that the financial economic benefits will flow to the entity, the related costs can be reliably estimated, and the amount of operating income can be reliably measured. Income from the sale of power generation is recorded based on the guaranteed energy and tariffs specified in the terms of supply agreements or the prevailing market price, as applicable.

c. Financial income and expenses The financial income and expenses of the Company comprises the following:

• Interest on interest earning bank deposits and other investment;

• Bank fees;

• Discounts obtained; and

• Expenses with interest on loans and financing.

Financial income and expenses are recognized in the income (loss) through effective interest method.

d. Foreign currency Foreign currency transactions Transactions in foreign currency are translated into the functional currency of the Group at the exchange rates on the dates of the transactions. Monetary assets and liabilities denominated in foreign currencies at the reporting date are retranslated into the functional currency at the exchange rate at that date. Exchange gain or loss in monetary items is the difference between the amortized cost of the functional currency at the beginning of the period, adjusted by interest

Companhia Mineira de Açúcar e Álcool Participações Financial statementsMarch 31, 2015

and effective payments during the period, and the amortized cost in foreign currency at the exchange rate at the end of the presentation period. Non-monetary items measured at historical costs in foreign currencies are converted by the exchange rate prevailing on the transaction date. Exchange differences arising from the reconversion are charged to income.

e. Employee benefits

(i) Short-term employee benefits Obligations for short-term employee benefits are recognized as personnel expenses as the related service is rendered. The liability is recognized at the amount expected to be paid, if the Company has a legal or constructive obligation to pay this amount as a result of prior service rendered by the employee, and the obligation can be reliably estimated.

(ii) Defined contribution plan Obligations for contributions to defined contribution pension plans are recognized in the income (loss) as personnel expenses when the services are rendered by the employees. Prepaid contributions are recognized as an asset to the extent that a cash refund or a reduction in the future payments is available. The Company has no other post-employment benefits.

f. Income and social contribution taxes The income and social contribution taxes, both current and deferred, are calculated based on the rates of 15% plus a surcharge of 10% on taxable income in excess of R$ 240 (annual basis) for income tax and 9% on taxable income for social contribution on net income, and consider the offsetting of tax loss carryforward and negative basis of income tax and social contribution, limited to 30% of the annual taxable income. The income tax and social contribution expense comprises the current and deferred installments. Current taxes and deferred taxes are recognized in profit or loss unless they are related to the business combination, or items directly recognized in shareholders' equity or other comprehensive income.

(i) Current tax Current taxes are the taxes payable or receivable on the taxable income or loss for the year and any adjustments to taxes payable in relation to prior years. It is measured based on rates enacted or substantively enacted at the balance sheet date. Current tax also includes any tax liability arising from the declaration of dividends. Current tax assets and liabilities are offset only if certain criteria are met.

(ii) Deferred tax Deferred taxes are recognized in relation to the temporary differences between the book values of assets and liabilities for financial statement purpose and the related amounts used for taxation purposes. A deferred income and social contribution tax asset is recognized in relation to tax losses, unused tax credits and deductible temporary differences, to the extent that it is probable that future taxable income will be subject to taxation will be available against which they will be used. Deferred income and social contribution tax liabilities are reviewed at each balance sheet date and reduced when their realization is no longer probable.

Companhia Mineira de Açúcar e Álcool Participações

Financial statementsMarch 31, 2015

Deferred taxes are measured at tax rates expected to be applied to temporary differences when they are reversed, based on rates enacted or substantively decreed up to the date of balance sheet. The measurement of deferred tax reflects the tax consequences that would follow the manner in which the Company expects to recover or settle the book value of its assets and liabilities.

Deferred tax assets and liabilities are offset only if certain criteria are met.

g. Biological assets Biological asset is measured at fair value less sales expenses. Changes in fair value less sales expenses are recognized in results. Sale costs include all costs that are necessary to sell the assets. Sugarcane is transferred to the cost of production at their fair value, minus estimated selling expenses determined on the cutoff date.

h. Inventories Inventories are measured at the lower of cost and net realizable value. Inventory costs are valued at the average cost of purchase or production and include expenses incurred in the acquisition of inventories, production and conversion costs and other costs incurred in bringing them to their current locations and conditions. The net realizable value is the estimated price at which inventories can be realized in the normal course of business, less the estimated completion costs and selling expenses. The sugarcane consumed in the production process is measured at its fair value, net of sales expenses determined on the cutoff date.

i. Property, plant and equipment

(i) Recognition and measurement PP&E items are stated at historical acquisition or construction cost, net of accumulated depreciation and impairment losses, when applicable. The cost includes expenditures that are directly attributable to the acquisition of assets. The cost of assets constructed by the Company itself and its subsidiaries include:

• The cost of materials and direct labor;

• Any other costs directly attributable to bringing the assets to the location and condition required for them to operate in the manner intended by the Management;

• The costs for dismantling and restoration of the site where these assets are located;

• Borrowing costs on qualifying assets.

• Purchased software that is integral to the functionality of a piece of equipment is capitalized as part of that equipment.

• When parts of a property, plant and equipment item have different useful lives, they are accounted for as separate items (major components) of PP&E.

Companhia Mineira de Açúcar e Álcool Participações Financial statementsMarch 31, 2015

• Gains and losses on disposal of a property, plant and equipment item are determined by comparing the proceeds from disposal with the carrying amount of Property, plant and equipment and are recognized net within "Other income" in the income (loss).

(ii) Subsequent costs Subsequent expenses are capitalized only when it is probable that associated future benefits may be earned by the Company and its subsidiaries. Maintenance expenses and recurring repairs are recognized in the income when incurred.

(iii) Maintenance costs The maintenance cost of a component of property, plant and equipment is recognized in the book value of the item when it is probable that the future economic benefits embodied in the component will flow and its cost can be reliably measured. The book value of the component that has been replaced by another is written off. Costs of normal maintenance on property, plant and equipment are charged to the income statement as incurred. The subsidiary Vale do Tijuco Açúcar e Álcool S/A. performs annual maintenance at its manufacturing unit, approximately in the period from December to March. The main maintenance costs include costs of labor, materials, outsourced services and overhead allocated during the off-season period. Said costs are accounted for as a component of the cost of the equipment and depreciated during the following harvest. Any other type of expenditure, which does not increase the useful life or maintain the grinding capacity, is recognized as an expense.

(iv) Depreciation Items of property, plant and equipment are depreciated from the date they are installed and are available for use, or, in the case of assets constructed by the Company, as of the date the construction is concluded and the asset is available for use. Depreciation is calculated to amortize the cost of property, plant and equipment items using the straight-line method based on estimated useful lives of items. Depreciation is generally recognized in income (loss), unless the amount is included in the book value of another asset. Land is not depreciated. The estimated useful lives such as weighted average rates, for the current and comparative years are as follows: Consolidated

Years Rates

Industrial equipment 19 5.40% Constructions and buildings 36 2.75% Agricultural machinery and tractors 5 18.75% Paving 10 10% Vehicles 5 20% Agricultural equipment 6 17.06% Machinery, equipment and tools 6 18.06% Furniture and fixtures 7 15.12% Computers and peripherals 5 19.85% Other 6 16.10%

Companhia Mineira de Açúcar e Álcool Participações

Financial statementsMarch 31, 2015

The depreciation methods, useful lives and residual values are reviewed at each reporting date and potential adjustments will be recognized as a change in accounting estimates.

j. Intangible assets

(i) Other intangible assets Other intangible assets acquired by the Group with finite useful lives are carried at cost, less accumulated amortization and accumulated impairment losses, when applicable.

(ii) Subsequent expenses Subsequent expenses are capitalized only when they increase the future economic benefits embodied in the specific asset to which they relate. All other expenditures are recognized in profit or loss as incurred.

(iii) Amortization Amortization is recognized in income on a straight-line basis over the estimated useful lives of the intangible assets as of the date they are available for use. The estimated useful life for the current periods and comparative are presented below:

Software 5 years The depreciation methods and useful lives and residual values are reviewed at each reporting date and potential adjustments will be recognized as a change in accounting estimates.

k. Investments The financial statements of the subsidiaries are included in the consolidated financial statements as from the date they start to be controlled by the Company until the date such control ceases. The accounting policies of the subsidiaries are aligned with the policies adopted by the Parent company. The Individual financial information of the Parent company, financial information of subsidiaries are recognized under the equity method.

l. Financial instruments The Group classifies non-derivative financial instruments in the following categories: financial assets measured at fair value through profit or loss, and loans and receivables. The Group classifies non-derivative financial liabilities in the category of other financial liabilities.

(i) Non-derivative financial assets and liabilities - Recognition and derecognition The Group initially recognizes the loans, receivables and debt instruments on the date that they were originated. All other financial assets and liabilities are initially recognized on the date of negotiation.

Companhia Mineira de Açúcar e Álcool Participações Financial statementsMarch 31, 2015

The Group fails to recognize a financial asset when the contractual rights to the cash flow of the asset expire, or when the Group transfers the rights to the reception of contractual cash flows over a financial asset in a transaction in which essentially all the risks and benefits of ownership of the financial asset are transferred. Any interest in such transferred financial assets that is created or retained by the Group is recognized as a separate asset or liability. The Group derecognizes a financial liability when its contractual obligations are discharged or canceled or expire. Financial assets and liabilities are offset and the net amount reported in the balance sheet only when there is a legally enforceable right of the Group to set off and there is intention to settle on a net basis, or to realize the asset and settle the liability simultaneously.

(ii) Non-derivative financial assets - Measurement Financial assets measured at fair value through profit or loss A financial asset is classified as measured at fair value through profit or loss if it is held for trading or is designated as such upon initial recognition. The transaction costs are recognized in income (loss) as incurred. Financial assets recorded at fair value through profit or loss are measured at fair value and changes in the fair value of such assets, including gains with interest and dividends, are recognized in the income for the year. Loans and receivables Such assets are initially recognized at fair value plus any transaction costs directly assignable. After their initial recognition, loans and receivables are measured at amortized cost using the effective interest rate method. Cash and cash equivalents Cash and cash equivalents comprise balances of cash and financial investments with original maturities of three months or less as of the contracting date, which are subject to an insignificant risk of change in value and are used to manage short-term obligations.

(iii) Non-derivative financial liabilities - Measurement Non-derivative financial liabilities are initially recognized at fair value less any transaction costs directly assignable. After their initial recognition, these financial liabilities are measured at amortized cost using the effective interest rate method. The Group has the following non-derivative financial liabilities: loans and financing, debentures and suppliers and other accounts payable.

(iv) Capital - Parent company Common shares Common shares are classified as shareholders' equity. Additional costs directly attributable to the issue of shares are recognized as a deduction from shareholders' equity, net of any tax effects. The Company’s bylaws determines a percentage higher than 25% to payment of compulsory minimum dividends.

Companhia Mineira de Açúcar e Álcool Participações

Financial statementsMarch 31, 2015

(v) Derivative financial instruments, including hedge accounting The Group holds derivative financial instruments to hedge its exposure to foreign currency and interest rate changes. Upon initial designation of the derivative as a hedging instrument, the Group formally documents the relationship between the hedge instruments and the hedgeable items, including the risk management goals and the strategy in the execution of the hedge transaction and the hedgeable risk, together with the methods that will be used to assess the effectiveness of the hedge relationship. The Group evaluates the hedge relationship, initially and then continuously, to conclude if hedge instruments are expected to be "highly effective" in the offset of variations in fair value or cash flows of items subject to hedge during the period for which hedge is assigned whether the actual results of each hedge are within the range of 80%-125%. For a cash flows hedge of a planned transaction, the transaction should have its occurrence as highly probable and should present exposure to variations in the cash flows that at the end could affect the reported income (loss). Derivatives are initially recognized at fair value. Any attributable transaction costs are recognized in profit or loss when incurred. After the initial recognition, derivatives are measured at fair value and changes in fair value are recorded as described below. Cash flow hedge When a derivative is designated as a hedge instrument to hedge cash flow variability attributed to a specific risk associated with a recognized asset or liability or a highly probable foreseen transaction that could affect the net income, the effective portion of variation in the derivative's fair value is recognized in other comprehensive income and disclosed in “equity evaluation adjustments” caption in shareholders' equity. Any non-effective portion of the variations in the fair value of the derivative is recognized immediately in net income. When the hedged item is a non-financial asset, the accumulated amount held in other comprehensive income is reclassified to income (loss) in the same year or years during which the non-financial asset does not affect income (loss). In other cases, the amount accumulated in other comprehensive income is transferred to income (loss) in the same year in which the hedgeable item affects income (loss). If the hedge instrument no longer satisfies the hedge accounting criteria, expires or is sold, wound up, exercised or has its designation revoked, then the hedge accounting is discontinued prospectively. If there are no more expectations regarding the occurrence of the planned transaction, then the balance in other comprehensive income is reclassified to income (loss).

m. Impairment

(i) Non-derivative financial assets Financial assets not classified as financial assets at fair value through income, including investments accounted for under the equity method, are evaluated at each balance sheet date to determine if there are objective impairment evidence. Objective evidences of financial assets’ impairment include:

• Debtor’s default or delays;

• Restructuring of an amount owed to the Group under conditions that are considered as abnormal;

Companhia Mineira de Açúcar e Álcool Participações Financial statementsMarch 31, 2015

• Indications that the debtor or issuer will face bankruptcy;

• Negative changes in payment situation of debtors or issuers;

• The disappearance of an active market for an instrument; or

• Observable data indicating that expected cash flow measurement of a group of financial assets decreased.

For investments in membership certificates, objective impairment evidences include a significant or prolonged decline in fair value, below cost. Financial assets measured at amortized cost The Group considers as evidence of impairment of assets measured by amortized cost both individually and on an aggregate basis. All individually significant receivables are assessed for impairment. Those identified as non-impaired on an individual basis are collectively assessed for any impairment loss not yet identified. Assets that are not individually significant are assessed on an aggregate basis in relation to impairment by grouping the assets with similar risk characteristics. When assessing impairment on an aggregate basis the Group makes use of historical trends of the recovery term and the amounts of losses incurred, adjusted to reflect the management's judgment if the current economic and credit conditions are such that the actual losses will probably be higher or lower than those suggested by historical trends. An impairment is calculated as the difference between the asset's book value and the present value of estimated future cash flows discounted at the financial asset's original effective interest rate. The losses are recognized in income and reflected in an account for allowance for losses. When the Group considers that it is not possible to reasonably expect recovery, amounts are written-off. When a subsequent event causes the amount of the impairment loss to decrease, the impairment loss is reversed through profit or loss. Investees recorded under the equity method of accounting A loss by a reduction to recoverable value referring to an investee valued under the equity method is measured by comparing the investment’s recoverable value to its book value. An impairment loss is recognized in the statement of income and is reversed if there has been a favorable change in the estimates used to determine the recoverable value.

(ii) Non-financial assets The carrying amounts of the Group's non-financial assets, except for inventories and deferred income tax and social contribution assets, are reviewed at each balance sheet date for indication of impairment. If such indication exists, the asset's recoverable amount is estimated. In case of goodwill, recoverable value is tested on an annual basis. For tests of reduction in recoverable value, assets are grouped into the smallest identifiable group of assets that can generate cash inflows by continuous use that are largely independent of cash flows from other assets, or Cash Generating Units (CGU).

Companhia Mineira de Açúcar e Álcool Participações

Financial statementsMarch 31, 2015

Recoverable value or CGU of an asset is the higher of value in use and fair value less selling costs. Value in use is based on estimated future cash flows discounted to present value using a discount rate before taxes that reflects current market evaluations of times value of money and the specific risks of the assets or CGU. An impairment loss is recognized when the carrying amount of an asset or its CGU exceeds its recoverable value.

n. Provisions Provisions are determined by discounting the estimated future cash flows at a pre-tax rate which reflects the current market evaluations as to the value of the cash over time and the specific risks of the liability. The effects of discounting to present value are recognized in net income as expense.

o. Statement of added value (“DVA”) The Group prepared individual and consolidated statements of added value in accordance with the rules of technical pronouncement CPC 09 - Statement of Added Value, which are presented as an integral part of the financial statements under accounting practices adopted in Brazil applicable to publicly-held companies, whereas under IFRS they represent additional financial information.

p. New standards and interpretations not yet adopted Several new standards, amendments to standards and interpretations will be effective for the years started after January 1, 2014, and have not been adopted to the preparation of these financial statements. Those that may be relevant to the Company are listed below. The Company does not plan to adopt these standards in advance. IFRS 9 Financial Instruments IFRS 9, published in July 2014, replaces guidelines of IAS 39 Financial Instruments: Recognition and Measurement (Financial Instruments: Recognition and Measurement). IFRS 9 presents reviewed guidelines on classification and measurement of financial instruments, including a new model for expected credit loss to calculate impairment of financial assets, and new requirements on hedge accounting. This rule maintains IAS 39 guidelines on financial instruments’ recognition and de-recognition. IFRS 9 is effective for periods beginning on or after January 1, 2018, with early adoption allowed. IFRS 15 - Income from Contracts with Clients The IFRS 15 requires an entity to recognize the amount of income reflecting the consideration that it expects to receive in exchange for control of these goods or services. The new standard will replace most of the detailed guidance on income recognition that currently exists in IFRS. The new standard is applicable beginning on or after January 1, 2017, with early adoption permitted by the IFRS. The standard may be adopted retrospectively, adopting a cumulative effects approach. The Company is evaluating the effects IFRS 15 will have on its financial statements and disclosures. The Company has not yet chosen the transition method to the new standard or determined the effects of the new standard in today's financial reports.

Companhia Mineira de Açúcar e Álcool Participações Financial statementsMarch 31, 2015

Agriculture: Production Plants (changes to IAS 16 and IAS 41) These changes require that production plants, defined as live plants, be recognized as property, plant and equipment and included in the ambit of IAS 16 Property, plant and equipment, instead of IAS 41 Agriculture. These changes are to be enforced in years starting on or after January 1, 2016, and early adoption is permitted. In addition, the following new rules or changes are not expected to have a significant impact on the Group’s consolidated financial statements.

• IFRS 14 - Regulatory Deferral Accounts

• Accounting for Acquisitions of Interests in Joint Operations (change of IFRS 11)

• Clarification of Depreciation and Amortization Acceptable Methods (changes to IAS 16 and IAS 38)

• Defined Benefit Plans: Employee Contributions (Defined benefit plan: Employees’ contribution) (change of IAS 19)

• Annual improvements of 2010-2012 IFRS’s

• Annual improvements of 2011-2013 IFRS’s

The Accounting Pronouncements Committee has not yet issued any accounting pronouncement or amendments in current pronouncements corresponding to these standards. Adoption in advance is not allowed.

9 Cash and cash equivalents Consolidated Parent company

03/31/2015 03/31/2014 03/31/2015 03/31/2014

Cash and banks 21,021 39,880 - - Interest earning bank deposits 120,388 20,682 122 116

141,409 60,562 122 116

The cash balance arises from receipts of business transactions and are resources available to meet the immediate cash needs of the Company and its subsidiaries. All funds are deposited in prime bank institutions. Interest earning bank deposits are cash equivalents since they are promptly convertible into a known sum of cash and subject to an insignificant risk of change of value. These interest earning bank deposits refer to Bank Deposit Certificates (CDB) in several financial statements, remunerated at rates that vary from 95% to 100% of the CDI - Interbank Deposit Certificate. Interest earning bank deposits have no monthly maturity and may be redeemed at any time.

Companhia Mineira de Açúcar e Álcool Participações

Financial statementsMarch 31, 2015

The Group's exposure to interest rate risks and a sensitivity analysis of financial assets and liabilities are disclosed in Note 22.

10 Trade accounts receivable and other receivables Consolidated Parent company

03/31/2015 03/31/2014 03/31/2015 03/31/2014

From the sale of ethanol 728 3,114 - - From the sale of energy 4,322 16,746 - - From the sale of sugar - 2,913 - - From service rendering - 1,587 - - From the sale of sugarcane 1,257 2,219 - - Other 1,062 4,674 - -

Trade accounts receivable 7,369

31,253 - - Related party credits (Note 27) - - 543 41,181

Other receivables - 543

41,181 Total 7,369 31,253 543 41,181

Current assets 7,369 31,253 - - Non-current assets - - 543 41,181