Embed Size (px)

Citation preview

OS SISTEMAS DE CONTRAGARANTIA EM PORTUGAL E NA EUROPA

XVIII Fórum Ibero-Americano

Sistemas de Garantia e Financiamento para as MPE

Rio de Janeiro, 26 de Setembro de 2013

José Fernando Figueiredo Presidente da SPGM/SGM/AECM

PM

E

Po

up

an

ça

POTENCIAR MECANISMOS DE MERCADO…

Business Angels Capital de Risco

M & A Capital de Risco

Maturidade

Private Equity Mercado de Capitais

... AO LONGO DO CICLO DE VIDA DA EMPRESA

Face a dificuldades no sistema financeiro convencional em resolver o problema da falha nos mercados de crédito, que não fazem chegar financiamento adequado às empresas, em especial às de pequena dimensão ou em fases particulares do seu ciclo de vida, foram criados mecanismos alternativos de cobertura do risco da banca;

De entre esses mecanismos, merecem destaque os sistemas de garantia de crédito para PME, baseados em instituições especializadas na cobertura (normalmente parcial) do risco de crédito dos bancos, quando estes emprestam dinheiro às empresas;

Em muitos casos esse mecanismos são privados com um resseguro público, noutros casos são inteiramente públicos;

Os Sistemas de Garantia Mútua consistem numa parceria público-privada, baseada nas Sociedades de Garantia Mútua, privadas, e num mecanismo publico de resseguro destas.

PORQUÊ A GARANTIA MÚTUA

As Sociedades de Garantia Mútua (SGM) são instituições de crédito privadas, mutualistas, cujo objectivo é o apoio às empresas, essencialmente às pequenas, médias e micro empresas (PME)*;

Prestam garantias financeiras “on first demand”, para facilitar a obtenção de crédito em condições de preço e prazo adequadas aos ciclos de atividade das PME, e todas as garantias necessárias ao desenvolvimento da sua atividade;

Com o objetivo de impulsionar o investimento, desenvolvimento, modernização e internacionalização das PME;

Beneficiam de uma contragarantia de um fundo público.

* mas também a indivíduos, nomeadamente ENI, agricultores e estudantes

O QUE É A GARANTIA MÚTUA

SPGMServiços Partilhados•Administrativos•Financeiros•Sistemas Informação• Jurídicos

FCGM

Fundo Europeu de

Investimento(FEI)

Acionistas

Norgarante Lisgarante

Garval Agrogarante

• IAPMEI• TP, ip• Instituições de Crédito

• PME’s• Associações Empresariais• Instituições de Crédito• IAPMEI• TP, ip• IFAP

Estrutura de Capital Maioritariamente Pública

Fundo Público

Garantia de 3º nível

Contragarantia Automática e Obrigatória

• Comissões de contragarantia• Contribuições Periódicas

Participa no capital das SGM’s e atua como “holding” do sistema

Estrutura de Capital Maioritariamente Privada

• Garantias• Ações

• Protocolos• Garantias de Carteira

• Contrato• Execução Técnica• Empréstimos Bancários• Etc.

Clientes:• PME’s• Pessoa Individual

Beneficiaries:• Instituições de Crédito• Instituições Públicas• Pessoa Individual

Sociedades de Garantia Mútua

Sociedade Gestora do FCGM

MODELO DE INTERVENÇÃO

As Sociedades de Garantia Mútua (SGM) emitem as garantias Estão em contacto com a Banca e PME, assim como com os representantes das PME;

O capital das SGM é maioritariamente detido pelas PME beneficiárias (>50%), Banca, associações empresariais e SPGM;

As SGM estão estritamente ligadas à SPGM, nomeadamente no que respeita ao desenho de novos produtos com garantia mútua (e contragarantia do FCGM) tornando-se desta forma e, posteriormente, num importante parceiro estratégico mas também pelo facto de a SPGM desenvolver um conjunto de serviços, enquanto centro de serviços partilhados, a todo o Sistema Português de Garantia Mútua;;

Possuem uma análise de risco independente e com capacidade de decisão sobre emitir ou não uma garantia, cobrindo uma parte dos riscos assumidos pela Banca e outras entidades que financiam as PME;

A comissão de garantia é determinada de acordo com a análise de risco efetuada e enquadrada no preçário e matriz interna definida pela SGM (comissão está compreendida entre um minimo de 0,5% e um máximo de 4,5%, por ano e a incidir sobre o valor vivo da garantia);

A comissão de garantia é normalmente paga pela PME mas, excecionalmente, em algumas linhas de crédito especificas lançadas em conjunto com a Banca e com o Estado, este último pode subsidiar a PME e assumir o custo da comissão de garantia (por exemplo: linhas PME Investe e PME Crescimento);

São supervisionadas pelo Banco de Portugal e operam de acordo com uma legislação especifica e dentro das regras gerais aplicáveis às instituições de crédito.

O SISTEMA PORTUGUÊS DE GARANTIA MÚTUA

O Fundo de Contragarantia Mútuo assume uma percentagem do risco assumido pela SGM Não tem contacto direto com as PME e as Instituições Financeiras;

O capital (891,4 millhões €, à data de Julho de 2013) é integralmente público (apesar da legislação permitir dotações privadas no FCGM, particularmente das SGM);

Não implica qualquer análise de risco casuística, uma vez que a contragarantia é automática e obrigatória por lei, contudo existe um controlo, de forma agregada, da evolução do risco global da carteira de garantias;

O preço da contragarantia é determinado de acordo com um modelo especifico, aprovado pelo Conselho Geral do FCGM. Partindo de um preço base de 0,2% sobre a média anual da carteira viva de contragarantias da cada SGM, pode variar de acordo com a evolução da sinistralidade, da maturidade da carteira e do risco médio da mesma (apesar das contragarantias serem automáticas, as SGM devem providenciar toda a informação ao FCGM sobre as caraterisicas de cada operação emtida, especialmente sobre risco e preço)

O nivel da contragarantia oscila entre os 50%-80% da garantia eimtida pela SGM, dependendo da linha de crédito especifica;

O FCGM é gerido pela SPGM.

O SISTEMA PORTUGUÊS DE GARANTIA MÚTUA

SPGM funciona como a “Holding” do Sistema Português de Garantia Mútua. Gere o Fundo de Contragarantia Mútuo (FCGM)

Funciona como um centro de serviços partilhados (back-office) quer para o FCGM, quer para as SGM;

Representa o interesse público no desenho e negociação de novas linhas de crédito ou outros produtos das SGM, contragarantidos pelo FCGM;

Destaca-se pela inovação no pensamento estratégico de politicas de financiamento para PME e constituiu-se como um benchmark no panorama internacional;

Negoceia com institutos públicos (IAPMEI, TP ip, COMPETE, Ministério da Educação e Ciência, IFAP, IEFP, etc) e com organizações internacionais novas linhas de crédito para as PME portuguesas;

Representa institucionalmente o SNGM internacionalmente, nomeadamente na Associação Europeia de Caucionamento Mútuo (AECM) e na rede de gaarantias ibero-americana (REGAR).

O SISTEMA PORTUGUÊS DE GARANTIA MÚTUA

Destinatários Destina-se às PME que cumpram as normas comunitárias e que não se encontrem em situação de dificuldades financeiras.

PMEs dos diferentes ramos de atividade, tais como, serviços, comércio, indústria, eletricidade, transportes, turismo, construção, mas também agricultura, educação e saúde se apresentam como elegíveis.

Produto Montante Máximo de Financiamento: 1,5 millhões de euros (através de uma ou mais SGM).

Prazo de Financiamento: Entre 1 a 10 anos

Finalidade: financiamentos de médio e longo prazo, incluindo operações de leasing com o objetivo de investimento em ativos tangiveis ou intangiveis ou de reforço de fundo de maneio, assim como financiamento de atividades inovadoras.

Exclusões: O financiamento não se pode destinar à reestruturação de dívida ou à substituição de crédito.

LINHA FEI 2013 – PROGRAMA-QUADRO PARA A COMPETITIVIDADE E INOVAÇÃO (CIP)

Apesar da atual reduzida taxa de emissão de garantias, considerámos que a implementação do Programa-Quadro para a Competitividade e Inovação (CIP) tem decorrido de forma positiva.

Tendo em consideração de que estamos no primeiro ano do Programa-Quadro para a Competitividade e Inovação (CIP), o impacto deste tem-se revelado ainda reduzido:

Financiamento: 1,4 milhões de euros

Garantias Emitidas:1,1 milhões de euros

Contra-Garantias Emitidas: 900 mil euros

Programa-Quadro para a Competitividade e Inovação (CIP) é e irá ser no curto prazo um instrumento de grande utilidade e que irá permitir ao SNGM a emissão de garantias após o fecho de algumas linhas especiais, compensando a atual escassez de fundos.

A força do programa reside na possibilidade de potenciar o crédito às PME. Ao fazer parte deste programa, o SNGM permitirá, até ao fim de 2015, o acesso ao financiamento até ao montante acumulado de 200 milhões de euros.

SPGM E PROGRAMA-QUADRO PARA A COMPETITIVIDADE E INOVAÇÃO (CIP)

DADOS ESTATISTICOS SNGM (1994-2012)

DADOS ESTATISTICOS SNGM (1994-2013Julho)

EVOLUÇÃO DA ATIVIDADE DAS SOCIEDADES DE GARANTIA MÚTUA

0 €500 €

1 000 €1 500 €2 000 €2 500 €3 000 €3 500 €4 000 €4 500 €5 000 €5 500 €6 000 €6 500 €

7 000 €

7 500 €

8 000 €

8 500 €

9 000 €

20032004

20052006

20072008

20092010

20112012

2013-07-31

201 € 254 € 408 € 651 € 966 €1 631 €

3 904 €

5 779 €

6 624 €

7 561 €

8 207 €

126 € 142 € 227 € 358 € 491 €913 €

2 749 €

3 762 €

3 240 €2 968 €

2 930 €

Sociedades de Garantia Mútua

Garantias Emitidas (inclui renovações e plafonds) Carteira Viva

EFEITOS MULTIPLICADORES DO INVESTIMENTO NO SISTEMA

Investimento Privado

Investimento Público

Garantias das SGM (2)

€ 8 207

Financiamento Bancário € 16 493

Investimento Induzido na Economia € 16 966

Contragarantia do FCGM (1)

€ 6 257

€ 1 080

€ 148

VALORES EM MILHÕES DE €UROS

NOTA: (1) Contragarantias emitidas - inclui renovações(2) Garantias emitidas - inclui renovações e plafonds

www.spgm.pt Obrigado!

AECM Guarantees and Counter-guarantees in

Europe

AECM: Today

founded in 1992 by 6 Members

In 2013:

39 Members

21 EU-countries

+ Turkey, Montenegro & Russia

Volume of Outstanding Guarantees/Counter-guarantees in portfolio 2012*: over 79 bn. EUR

Number of Outstanding Guarantees/Counter-guarantees in portfolio 2012*: over 2.08 mn. Active guarantees

* Provisional figures

AECM: Global Figures

0 5 10 15 20 25 30 35 40 45

1992

1995

1996

1997

2000

2001

2002

2003

2004

2005

2006

2007

2009

2010

2011

2012

2013

6

8

11

13

15

17

21

23

27

28

30

33

34

36

39

39

6 2

3 2

2 2

4 2

5 1

2 3

2 2

3 1 1

1

1

1

Existing members Adhesion date Exiting members

AECM Members – Evolution over the past 20 years

AECM: Guarantee activity in Europe

Average size of guarantee amount (values en €’000)

-8,00%

-6,00%

-4,00%

-2,00%

0,00%

2,00%

4,00%

6,00%

8,00%

€ 30,00

€ 31,00

€ 32,00

€ 33,00

€ 34,00

€ 35,00

€ 36,00

€ 37,00

€ 38,00

€ 39,00

€ 40,00

€ 41,00

2006 2007 2008 2009 2010 2011 2012***

Average size of guarantees (in portfolio) per year (values in €'000) and year-to-year progression

Average size of guarantee per member & year (in portfolio)

y-o-y progression

Lineal (Average size of guarantee per member & year (in portfolio)) *** Provisional figures

Average size of guarantee amount per country 2012

AECM: Guarantee activity in Europe

€ 0,00

€ 50,00

€ 100,00

€ 150,00

€ 200,00

€ 250,00

Average size of guarantee amount for each country (p.a. / in €'000) 2012***

*** Provisional figures

Average size of guarantee amount per country 2011

AECM: Guarantee activity in Europe

€ 0,00

€ 50,00

€ 100,00

€ 150,00

€ 200,00

€ 250,00

Average size of guarantees for each country (p.a. / in €'000) 2011

AECM Members – Evolution over the past 20 years

AECM Members receive counter- guarantees: EU Counter-guarantees through:

CIP program Structural fund programs (i.e.

ERDF and JEREMIE) National public and/or private counter-guarantees Regional public and/or private counter-guarantees

AECM Members issue counter-guarantees AECM Members guarantee activity:

In terms of volumes in portfolio for 2012, represents: 81,51% towards counter-guarantee activity (18,49%)

In terms of number in portfolio for 2012, represents: 91,30% towards counter-guarantee activity (8,70%)

AECM: Guarantee vs Counter-guarantee activity in Europe

AECM: Guarantee vs Counter-guarantee in activity in Europe

- €

10.000.000 €

20.000.000 €

30.000.000 €

40.000.000 €

50.000.000 €

60.000.000 €

70.000.000 €

2012

14.025.999 €

64.485.393 €

Volumes of guarantees and counter-guarantees in portfolio (values in € '000)

Volume of counter-guarantees in portfolio (in '000EUR)

Volume of guarantees in portfolio (in '000EUR)

Provisional figures 2012

Proportion of counter-guarantee activity towards AECM total volumes in portfolio represents 18,5%

AECM: Guarantee ans Counter-guarantee activity in Europe

Proportion of counter-guarantee activity towards AECM total number of guarantees in portfolio represents 8,7%

-

500.000

1.000.000

1.500.000

2.000.000

2012

174.540

1.899.112

Number of guarantees and counter-guarantees in portfolio (in units)

Number of counter-guarantees in portfolio (in units)

Number of guarantees in portfolio (in units)

Provisional figures 2012

Counter-guarantee draft report

AECM: Counter-guarantee activity in Europe

Presentation of the main findings: General facts

EU counter-guarantees received

National/federal public and private counter-guarantees received

Regional public and private counter-guarantees received

Counter-guarantor: counter-guarantees issued by AECM members

AECM: Counter-guarantee activity in Europe

General Facts

0 5 10 15 20 25 30 35

31

9

9 3

0

8

1

2

1

9

Overall responses on Counter-guarantees received & issued

Counter-guarantee provider

Regional Private

Regional Public

National Private

National Public

Progress-Program

Structural Funds Programs

CIP-Program

EU counter-guarantees received

AECM: Counter-guarantee activity in Europe

Competitiveness and Innovation programme (CIP): 9 out of 31 respondents Represent: 48% of total SMEs supported through CIP Volumes issued with CIP counter-guarantees: €4,6bn CAP rate: confidentiality agreement with the EIF, but can range from 3 to 10 %

Microfinance facility – Progress: No respondents uses Progress counter-guarantees

AECM: Counter-guarantee activity in Europe

EU counter-guarantees received

Structural funds:

3 out of 31 respondents

SOCAMUT-Belgium: receive ERDF funds (40%) co-financed with

regional sources (60%), amounting to €10,28 million;

INVEGA – Lithuania: receive ERDF funds (€37,36 million) co-financed by

the Lithuanian National programme;

BGK – Poland: receiving counter-guarantees through the Structural fund

programme called, JEREMIE;

AECM: Counter-guarantee activity in Europe

National/federal public and private counter-guarantees received

National/federal public: 8 out of 31 respondents: receive national

public counter-guarantees For all respondents: counter-guarantees cover direct guarantees and for 2 respondents

portfolio guarantees Overall volume received by all respondents (from 2010 until 2012): over €16bn 4 out of 8 respondents: no counter-guarantee fee

charged National/federal private:

2 out of 31 respondents: receive national private counter-guarantees Confidi soci have framework agreement with both national private counter-guarantor

AECM: Counter-guarantee activity in Europe

Regional public and private counter-guarantees received

Regional public: 2 out of 31 respondents: VDB – Germany and AssoConfidi – Italy:

AssoConfidi: 4 Confidis receiving counter-guarantees from 4 Regional funds (i.e. Marche, Piemonte, Sardinia & Pordenone)

VDB – Germany: the risk is shared between the federal state (Bund) and the regions (Länder)

Regional private: 1 out of 31 respondents: AssoConfidi – Italy:

Eurofidi SCPA: receiving regional private counter-guarantees, only for the region of Lombardi

AECM: Counter-guarantee activity in Europe

Counter-guarantor: counter-guarantees issued by AECM members

AECM members issuing counter-guarantees are: 9 out of 31 respondents:

4 out of 9 respondents: 100% public shareholders 2 out of 9 respondents: 100% private 3 out of 9 respondents: public-private mixed

The main beneficiaries are: Mutual Guarantee Societies, Regional Guarantee Schemes, Banks, etc.

AECM members cover: Direct guarantees & portfolio guarantees

Counter-guarantee coverage rate: mainly fixed

AECM: Counter-guarantee activity in Europe

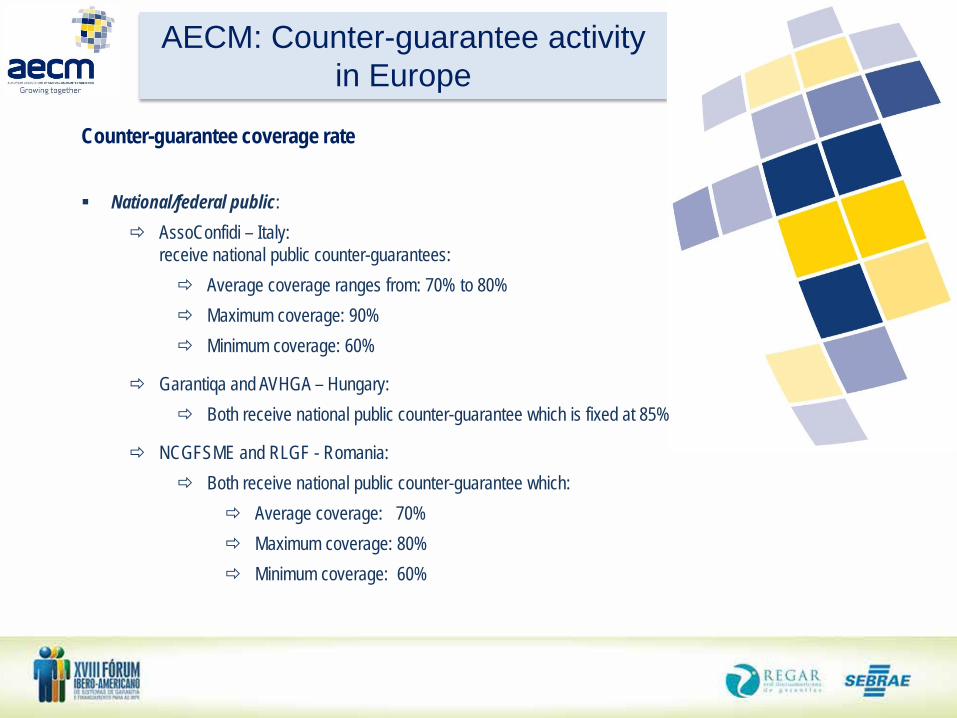

Counter-guarantee coverage rate

National/federal public: AssoConfidi – Italy:

receive national public counter-guarantees: Average coverage ranges from: 70% to 80% Maximum coverage: 90% Minimum coverage: 60%

Garantiqa and AVHGA – Hungary: Both receive national public counter-guarantee which is fixed at 85%

NCGFSME and RLGF - Romania: Both receive national public counter-guarantee which:

Average coverage: 70% Maximum coverage: 80% Minimum coverage: 60%

AECM: Counter-guarantee activity in Europe

Counter-guarantee coverage rate

National/federal and regional public: VDB - Germany:

receive a public counter-guarantee composed of a national/federal (Bund) and a regional (Länder) component:

AECM: Counter-guarantee activity in Europe

National/federal and regional public: VDB - Germany:

For Eastern Germany: - National/federal (Bund): covering 45% - Regional (Länder): covering 30% - German Guarantee Bank: covering 25%

For Western Germany: - National/federal (Bund): covering 39% - Regional (Länder): covering 26% - German Guarantee Bank: covering 35%

Counter-guarantee coverage rate

AECM: Counter-guarantee activity in Europe

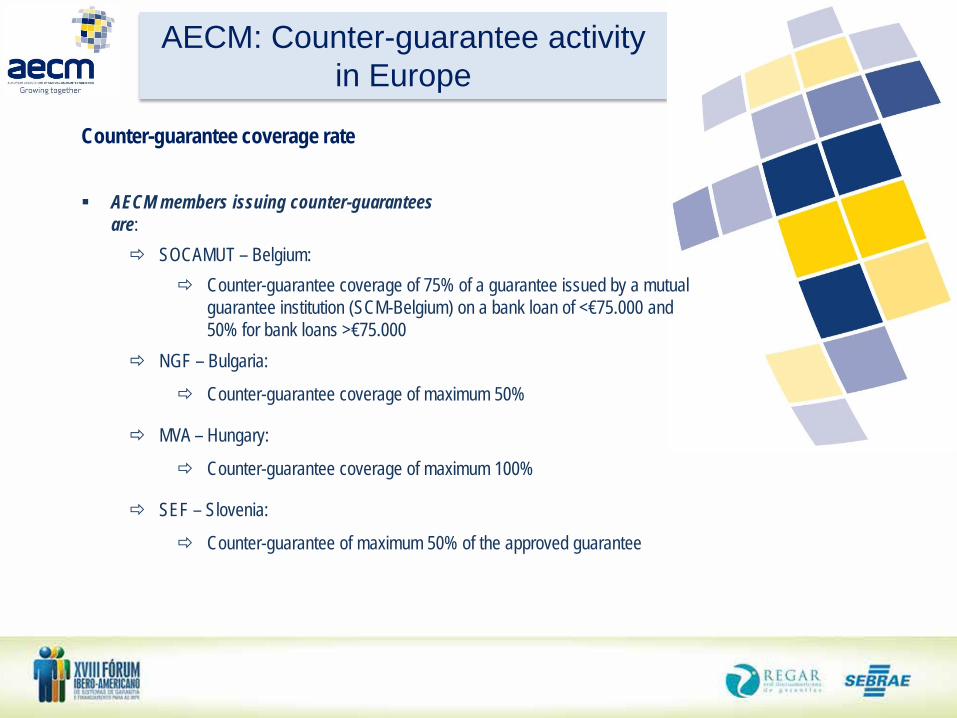

AECM members issuing counter-guarantees are: SOCAMUT – Belgium:

Counter-guarantee coverage of 75% of a guarantee issued by a mutual guarantee institution (SCM-Belgium) on a bank loan of <€75.000 and 50% for bank loans >€75.000

NGF – Bulgaria:

Counter-guarantee coverage of maximum 50%

MVA – Hungary:

Counter-guarantee coverage of maximum 100%

SEF – Slovenia:

Counter-guarantee of maximum 50% of the approved guarantee

Counter-guarantee coverage rate

PORTUGUESE GUARANTEE SCHEME THE PUBLIC COUNTER-GUARANTEE FUND

The Counterguarantee Fund (FCGM) automatically covers a part of the risk taken by the MGS.

It is a losses fund endowed with the money (cash and state guarantee) needed to cover the expected

losses on the counterguarantees issued;

It has no direct contact with both SME and Banks as this is done at field level by the MGS;

The subscribed share capital (of around 900 million €, by July 2013) is fully owned by the state

(although the legislation also foresees private endowments to the Fund, namely from the private

MGS in case of necessity). The equity came both from national budget, ministries specific

budgets and structural funds programmes;

PORTUGUESE GUARANTEE SCHEME THE PUBLIC COUNTER-GUARANTEE FUND

Is doesn’t carry individual risk analysis per file, as counter-guarantees are by law automatic

and compulsory, but controls “the MGS global portfolio risk evolution” in an aggregated way,

through its managing society (that performs risk analysis of the portfolio every semester

using recognised external entity) and the General Council. The last is chaired by a

representative of the Minister of Finance and has representatives of all Ministries involved

and defines not only the products and lines that can be counter-guaranteed by the FCGM

but also the specific price changes for the counter-guarantee according to the evaluation

of the risk profile of the MGS;

The price of the counter-guarantees is set according the a specific model, approved by the general council of

the Fund. From a basic fee of 0,2% on the average annual portfolio of counter-guarantees of each

MGS, the price can then be increased taking into consideration the default rates evolution, the

average term of the guarantees portfolio, the average risk levels of the portfolio (although counter-guarantees are automatic,

the MGS must provide to the fund full information on the characteristics of each file and operations issued, namely ratings and prices);

PORTUGUESE GUARANTEE SCHEME THE PUBLIC COUNTER-GUARANTEE FUND

The counter-guarantee levels goes from 50% to 80% of the guarantees issued by the MGS,

depending on the type of product;

The Fund is managed by a managing company (SPGM), set by the funds law;

The Fund is audited by internal auditors, being the external auditor the Auditor Body

of the Central Bank. It is submitted to specific auditing from fiscal authorities (IGF)

and court of auditors, namely in specific programmes supported by structural funds and/or national

budget endowments and/or under a third level partial coverage of the EIF/EU programmes;

Gets a third level guarantee that partially covers its issued counter-guarantees from the EIF under the

EU different SME supporting programmes like CIP.

PORTUGUESE GUARANTEE SCHEME THE PUBLIC COUNTER-GUARANTEE FUND

Proportion of counter-guarantee activity towards volumes in portfolio represents 81,2%.

0,00 €

500 000,00 €

1 000 000,00 €

1 500 000,00 €

2 000 000,00 €

2 500 000,00 €

3 000 000,00 €

2012

Volumes of guarantees and counter-guarantees in portfolio(values in €'000)

Volume of guarantees in portfolio

Volume of counter-guarantees in portfolio

PORTUGUESE GUARANTEE SCHEME THE PUBLIC COUNTER-GUARANTEE FUND

0,00 €

5 000,00 €

10 000,00 €

15 000,00 €

20 000,00 €

25 000,00 €

30 000,00 €

35 000,00 €

40 000,00 €

2012

39 667,07 €

32 205,38 €

Average size of guarantees and counter-guarantees in portfolio(values in €'000)

Average size of guarantees in portfolio

Average size of counterguarantee in porfolio

www.spgm.pt Thank You!