Embed Size (px)

Citation preview

1 1

Corporate Presentation March 2012

100% 100% 100% 100% 100% 100% 51% 100% 51% 20%

25.85%

Light

Energia

S.A.

Light

Serviços de

Eletricidade

S.A.

Light Esco Prestação de

Serviços S.A.

Lightcom Comercializadora

de Energia S.A.

Itaocara

Energia

Ltda.

Light

Soluções em

Eletricidade

Ltda.

Instituto

Light

Lightger

S.A.

Axxiom

Soluções

Tecnológicas

S.A.

CR Zongshen

E-Power Fabricadora de

Veículos Ltda.

Renova

Energia S.A.

Light S.A.

(Holding)

25.5%

Amazônia

Energia

S.A.

33%

EBL

Cia de

Eficiência

Energética

S.A

Distribution Generation Commercialization and Service System Electric

Vehicles

Institutional

Light Holdings

Norte

Energia S.A.

9.77%

2

Guanhães

Energia

51%

3 3

Integrated

Net Revenues 2010 – R$ Billion

52.044

43.737 43.345

30.562

22.384 22.358

Distribution

Energy Consumption in Concession Area (2010) - GWh1

Generation Private-owned Companies

Installed Hydro-generation Capacity (MW) – oct.11

5.630

2.660 2.307

2.150 1.790

866

12,9

12,1

8,9 6,9

6.2 5,1

Rankings

Souce: Companies reports

Note: 1 – Captive market + free clients

2 – It doesn’t consider the consumption of CSN and CSA

Among the largest players in Brazil

CEMIG RME LEPSA BNDESPAR MARKET

FIP LUCE

LUCE LLC

PARATI

CEMIG FIP

REDENTOR

REDENTOR

ENERGIA

26.06% 13.03% 13.03% 15.02% 32.85%

100%

75% 25%

13.03% 13.03% 100%

96.80%

75% 9.77%

6.41% 19.23%

BTG

PACTUAL

SANTANDER

VOTORANTIM

BANCO DO

BRASIL

28.57%

5.49%

28.57%

5.49%

28.57%

5.49%

14.29%

2.75%

25%

MINORITY

SHAREHOLDERS

3.20% 0.42%

Free Float 47.9%

100% 25.64%*

FOREIGN NATIONAL

66.94% 33.06%

Percentage in blue: indirect stake in Light

*12.61% (RME) + 13.03%(LEPSA)

Light S.A.

(Holding)

Controlling Shareholders

52.1%

Shareholders Structure

11 Board members: 8 from the controlling

group, 2 independents e 1 employees

nominated

A qualifying quorum of 7 members to

approve relevant proposals such as: M&A

and dividend policy

Indirect stake in blue

4

5 5

Controller discussion

group

Controller group Minority

General Assembly

Fiscal Council

Board of Directors

Auditors

Committee

Governance and

Sustainability

Committee

Human Resources

Committee

Finances

Committee

Management

Committee

Management

Shareholders

Interface

11 Board members: 2 independent

and 1 employees nominated

2 years term

Fiscal Council

Manual of Corporate Governance

Corporate Governance

LGSXY ADR-OTC

6 6

Distribution Business

• 4.0 million clients (serving 10 million people)

• Energy sales (2011) – 22,932 GWh

• 70% of the consumption of Rio de Janeiro state (Brazil’s

2nd GDP)

5th largest energy distribution company in Brazil

LIGHT

Industrial Residencial Comercial outros Livre

ELECTRICITY CONSUMPTION¹

TOTAL MARKET (GWh) - Year

¹ Note: To preserve comparability in the market approved by ANEEL in the tariff adjustment

process, the billed energy of the free customers Valesul, CSN and CSA were excluded in view

of these customers’ planned migration to the core network.

RESIDENTIAL

35.5%

INDUSTRIAL 8.1% OTHERS

15.3%

FREE

14.0%

COMMERCIAL

27.2%

+2.5%

22.1 ºC 21.7 ºC

22.0 ºC 21.7 ºC

+3.1% a.a

Energy Consumption

Distribution

7

24.5 ºC 23.9 ºC

2011 2010 2009 2008

25.0 ºC 23.8 ºC

15,5

17,5

19,5

21,5

23,5

25,5

27,5

2008 2009 2010 2011

Série1

22,932 22,384 21,491 20,928

2010 20112010 2011 2010 2011 2010 2011 2010 2011

ELECTRICITY CONSUMPTION (GWh)

TOTAL MARKET - YEAR

2011 2010 2011 2010 2011 2010 2011 2010 2011 2010

+2.5%

19,459 19,877

22,384

2.924 3.056

22,932

+2.5%

3,342 3,417

3,516

185

3,603

+4.3%

6,157 6,310

6,679

523

6,967

0.0%

3,945

1,717 1,731

3,944

+2.1%

8,243 8.418

174

657

2,228 2,213

RESIDENTIAL INDUSTRIAL COMMERCIAL OTHERS TOTAL

CAPTIVE FREE

Total Market

9

Prospects for Rio de Janeiro

R$ 181 billion in investments¹

2011-2013

¹Source: Firjan (Industry Federation of Rio de Janeiro)

Oil

R$ 107.9 bn

59.5%

Tourism

R$ 0.9 bn

0.5%

Others

R$ 6.7 bn

29.5%

Transformation Industry

R$ 29.5 bn

16.3%

Infrastructure

R$ 36.3 bn

20.0%

10

-Maracanã (ND)

-Port Maravilha (ND)

-Morar Carioca (ND)

- International Airport (5MW)

- Inhauma Shipyard (ND)

-Atento (2MW)

-Expansion Nova América (4MW)

-Expansion Norteshopping (3MW)

S Ã O

P A U L O

M

I

NA S

G

E R

A

I

S

Be lfordRoxo

S.J .Me riti

Nilópolis

Ca xias

NovaIgua çu

Magé

Niterói

São Gonçalo

Petrópolis

Pati do Alferes

Migu el Pe re ira

Sapuc aia

Sumidouro

Ca rmo

Duas Barras

de FrontinEng. Paulo

Vassouras

Me nde s

Paracambi

Ita gua i

Que imados

Japeri

Qua tisPorto Re alRe send e

Pinhe iral

Volta R edonda

Ba rra d o Piraí

Valença

R es tinga de Mar amba ia

Rio Cla ro

Piraí

Ba rra Mansa

Banan al

Passa Vinte

Santa Rita de Jacutinga

Rio Preto

Rio da s Flores

Chia dor

Santana do De se rto

Além Paraíba

dos R eisAngra

Ma nga ratiba B a í a de S e p e t i b a

ILHA GRANDE

Volta Grande

Seropedica

Paraiba do Sul

Três Rios

Com.Levy Gasparian

Teresópolis

Areal

do Rio PretoSão José do Vale

RIO DE JANEIR O

-Petrobras (15MW)

-CSN (100MW)

-Gerdau (30MW)

-Usiminas (20MW)

-LLX (40MW)

-Base Naval(25MW)

-Hotel Comfort (3MW)

-Gerdau (90MW)

-Shop.CampoGde(3MW)

-Nestlé (3MW)

Rio Janeiro

-Bio Manguinhos (ND)

-Hermes (3MW)

-Votorantin (ND)

-Ongoing (ND)

-Bunge (ND)

-AMBEV (2MW)

-GE (6MW)

-Shop. Metropolitano (10MW)

-RHI (5MW)

-Lavazza (3MW)

-Ajebras (5MW)

-Reluz (ND)

-Embelleze (5MW) -MRS (ND)

-AMBEV (ND)

-Coquepar (42MW)

-Procter & Gamble (10MW)

-Alpargatas (ND)

Economic activity leading to more demand

2009 2010 2011

Total Varejo Grandes Clientes Poder Público

2010 2011

PDD / GROSS REVENUE COLLECTION RATE BY SEGMENT

YEAR

97.9% 97.4% 94.3% 94.1% 100.8% 101.0%

107.1% 102.6%

2010 2011

3.2% 3.2%

2009 2010 2011

3.1%

Total Retail Large

Customers Public Sector

Collection

11

2010 2011

2010 2011

dez/10 mar/11 jun/11 set/11 dez/11

INCORPORATION

GWh

2011 2010

169.3 178.2 -12.0%

RECOVERY

GWh

2011 2010

140.4

67.6

LOSS (12 MONTHS)

41.6%

35.1%

5,278 5,326

2,231

7,493 7,543

41.8%

+107.8% Mar/11 Dec/10

2,215

5,312

41.3%

5,299

2,293

7,619

Jun/11 Sep/11

7,627

40.7%

1S10 1S11

Dec/11

5,256

2,328

7,591

40.5%

1S10 1S11

2,335

% Non-technical losses / Low

voltage market

Technical losses GWh

% Non-technical losses / Low

voltage market - Regulatory

Non-technical losses GWh

Dec/11

Loss prevention

12

13

New Technology Program

Technology used in regions in which conventional measures are not effective

Areas that present high levels of non-technical losses

Light aims to reduce losses through investments in new technologies, integration of operational

activities, increase of public awareness and institutional partnerships with interested agents

Grid shielding projects

75 412

REDE ATUAL

75 412

REDE BLINDADAActual grid Shielded grid

Control room

3 m

9 m

Low

voltage

Mechanical

Meter

Medium

voltage

Display

Low

voltage

Medium

voltage

Centralized

meter

14

New Technology Program

Monitoring, reading, cutting and

reconnection of customers telemetry–

MCC (Measuring Center Centralized)

Prioritization in areas of high losses and

aggressiveness to the network

Technology hindering inappropriate

interference in networks

Meters Installed (as of Dec, 2011)

TOTAL INDIVIDUAL CENTRALIZED

38,000

208,000

160,000

(ITRON) (LANDIS GYR

CAM and

ELSTER)

15

Losses (before): 26%

Losses (current): 5%

New Technology Results - Individual

16 16

New Technology Results - Centralized

Losses (before): 53%

Losses (current): 11%

17

Program Gains – An example

300 kWh

100 kWh

REAL

CONSUMPTION

BILLED

CONSUMPTION

NEW METER

INSTALLATION

200 kWh

LOST ENERGY

ENERGY SAVED

100 kWh

BILLED CONSUMPTION

INCREASE

100 kWh

OTHER EFFECTS (BY-PRODUCTS):

CAPEX GOES TO

THE RAB

BAD DEBT

PROVISION

REDUCTION

OPERATIONAL

COSTS

REDUCTION

18

Transformation of risky areas

19

Outcome of Actions in Pacified Communities

Before After Before After

Clients 80 1.593 Clients 1.054 1.635

Losses 90% 1% Losses 68% 51%

Delinquency 70% 3% Delinquency 79% 36%

Clients 408 600 Clients 295 1.281

Losses 56% 2% Losses 50% -

Delinquency 74% 3% Delinquency 70% 21%

Clients 2.800 3.826 Clients 199 1.673

Losses 61% 7% Losses 50% -

Delinquency 68% 9% Delinquency 70% 22%

Clients 389 1.017 Clients 2.241 3.135

Losses 73% 7% Losses 55% -

Delinquency 54% 13% Delinquency 48% -

Clients 470 807 Clients 199 1.673

Losses 58% 9% Losses 61% -

Delinquency 52% 14% Delinquency 48% -

Clients 0 423

Losses 100% 8%

Delinquency 100% 10%

Formiga

Borel

Community Community

Cantagalo

Tabajaras

Cabritos

Santa Marta

Chapéu

Mangueira

Cidade de

Deus

Babilônia

Casabranca

Batan

20 20

Generation Business

21

Installed Capacity

HPP Santa Branca

56 MW

HPP Ilha dos Pombos

187 MW

HPP Fontes Nova

132 MW

HPP Underground Nilo Peçanha - 380 MW

HPP Pereira Passos 100 MW

SP

RJ

HPP Santa Branca

Paraiba do Sul River

HPP Ilha dos Pombos

Installed Capacity

855 MW

100% 100%

100% 100% 100%

Lajes

Complex

22

Re-pricing of existing energy

2008-2012

27

2013

27

2014

27

510

146

234

130

276

234

Contracted Energy

Uncontracted Energy

New Contracts

Hedge

GENERATION

Assured energy: 537MW average

Capacidade Atual

(+) PCH Paracambi

(+) PCH Lajes

(+) UHE Itaocara

(+) Renova (+) Belo Monte

Capacidade após

expansão

Installed Capacity (MW)

+ 75.4%

866 13 9 74

277

1,519 280

(+) Renova² (+) Belo

Monte³

SHP

Paracambi¹

SHP

Lajes¹

Current

Capacity HPP

Itaocara¹

Capacity

After

Expansion

Investments in Renova and Belo Monte, in line with our strategy of growing

in the generation business

¹ Considering 51% stake

² Considering 25.9% stake

³ Considering 2.5% stake

New Generation Projects

23

24

Co

ntr

act

Sit

es

Term

(years

)

Ind

ex

Op

era

tio

n S

tart

up

(Esti

mate

d)

Insta

lled

Cap

acit

y

(MW

)

Av

era

ge L

oad

Facto

r (%

)

Esti

ma

ted

En

erg

y

(MW

av

era

ge)

To

tal C

AP

EX

(R$ M

N)

Realized

CA

PE

X

(R$ M

N)

Lo

an

Tari

ff

(R$/M

W)

SHPP 3 20 IGPM In operation

since 2008 41.8 61.3 24.2 189 -

BNB

Contracted 185.17

LER 2009 14 20 IPCA Jul - 2012 293.6 50.7 148.9 (*) 1,170 761.7 BNB

Contracted 145.81

LER 2010 6 20 IPCA Sep - 2013 162 53.6 86.8 (*) 599 14.1 BNDES

application 121.25

Y-3 2011 9 20 IPCA Mar - 2014 212.8 50.8 108.1 (*) 702 - BNDES

application 98.53

PPA Light 1 10 (E) 20 IPCA 2015 200 50.0 (E) 100 (E) 660 - - -

PPA Light 2 10 (E) 20 IPCA 2016 200 50.0 (E) 100 (E) 660 - - -

Renova – Contracts

* Does not considered the network basic losses.

25

Belo Monte Overview

51.0% CS

0.0% PS 49.0% CS

100.0% PS

Amazônia Energia

Participações S.A

Norte Energia S.A

(Belo Monte)

9.77%

74.5% of total stock 25.5% of total stock

Technical data on the concession:

Concession period – 35 years

End of concession – August 25, 2045

Technical data on the project:

Installed capacity - 11,233 MW

– Main engine room – 11,000 MW

– Auxiliary engine room – 233 MW

Assured Energy (Average MW) – 4,571 MW

Reservoir – 516 Km²

Flooded area/generation ratio of 0.05 Km²/MW

5,000 families affected

Estimated project cost (April 2010) – R$ 25.8 billion

Other Informations:

Amazônia Energia will own 9.77% of the enterprise.

– Construction works estimated to take 9 years.

– Transaction does not affect Light ‘s dividend flow

BNDES loan ensures leverage at low cost on favorable terms.

– Tender 30 years, fixed installments, 85% of items financiable, PSI line.

Amazônia Energia’s equity in the project estimated at R$ 150 million (Apr.

2010), to be disbursed over 6 years.

Expansion of generation portfolio:

– Increases Light’s total generation portfolio by 280 MW

Terms for sale of electricity generated already set.

− Regulated Market: 70%; Free Market: 20%; Self-producers: 10%.

Public sector

49,98%

Others privates30,25%

Amazônia Energia9,77%

Self prod.10,00%

Norte Energia S.A. – Shareholders Profile

26

Guanhães

TOTAL CAPEX

R$ Million

PCH

Dores de

Guanhães

Senhora do

Pôrto Jacaré Fortuna II Total

Installed Capacity

(MW) 14 12 9 9 44

Assured Energy

(MWaverage) 8 6.77 5.15 5.11 25.03

ANEEL Authorization 11/22/2002 10/08/2002 10/29/2002 12/21/2001

Operation - Start up Dec/13 Dec/13 Feb/14 Oct/13

Authorization Term 30 years (with renewal for 20 years)

269.2

60.2

57.8

151.2

Equity

Debt

Light Energia

Cemig GT

BNDES

27 27

Results

28

NET REVENUE BY SEGMENT (2011)*

NET REVENUE FROM DISTRIBUTION (2011)

Commercial 30.3%

Industrial 8.4%

Others (Captive) 13.5%

Network Use (TUSD) 2.3%

Residential 45.6%

Distribution 91.6%**

Commercialization 3.0% Generation 5.4%

(Free + Concessionaires) 4T10 4T11 2010 2011

NET REVENUE

(R$ MN)

+4.7%

1,733.1

1,815.1

4Q11 4Q10 2011 2010

6,508.6 6,944.8

+6.7%

195.8 237.8

1,537.3 1,577.3

794.6

5,955.8

6,150.1

552.8

91,57%

5,38% 3,05%

2011

2011

3.3%

2.6%

Construction revenue

Revenue w/out construction revenue

*Eliminations not considered ** Construction revenue not considered

Net Revenue

4T10 4T11 2010 2011

Manageable

(distribution): R$ 1,252.7

(23.4%)

Generation and

Commercialization: R$ 323.9

(6.1%)

Non – Manageable

(distribution): R$ 3,772.2

(70.5%)

DISTRIBUTION MANAGEABLE COSTS (R$MN)

COSTS (R$MN)*

2011

4Q11 4Q10 2011 2010

-15.6%

330.1 278.7

1,136.0 1,252.7

+10.3%

R$ MN 4Q10 4Q11 Var. 2010 2011 Var.

PMSO 198.8 149.6 -24.8% 637.4 646.5 1.4%

Provisions 57.2 56.8 -0.8% 208.4 299.4 43.7%

PDD 49.3 35.3 -28.5% 254.8 251.3 -1.4%

Contingencies 7.9 21.5 171.8 -46.4 40.8 -

Depreciation 74.0 72.3 -2.3% 290.2 306.8 5.7%

Total 330.1 278.7 -15.6% 1,136.0 1,252.7 10.3%

Não gerenciáveis; 3.772,2; 70,52%

Gerenciáveis; 1.252,7; 23,42%

Geração e Comercialização;

323,9; 6,06%

2011

*Eliminations not considered

Operating Costs and Expenses

29

Distribuição ; 994,3; 79,29%

Geração; 244,0; 19,46%

Comercialização; 15,7; 1,25%

2011

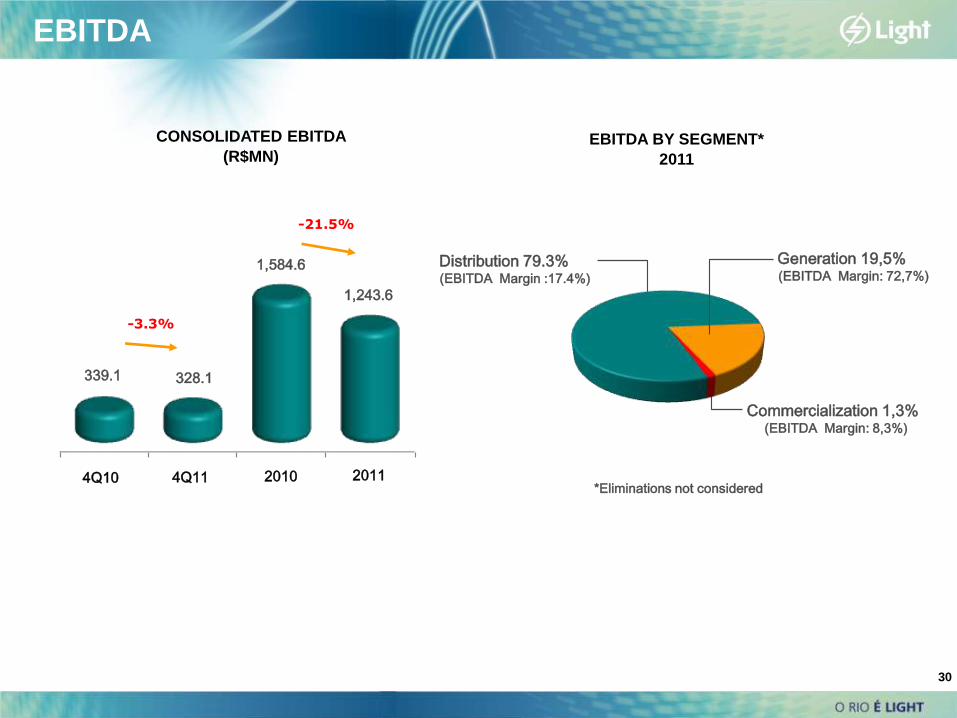

4T10 4T11 2010 2011

CONSOLIDATED EBITDA

(R$MN) EBITDA BY SEGMENT*

2011

Generation 19,5% (EBITDA Margin: 72,7%)

Commercialization 1,3% (EBITDA Margin: 8,3%)

Distribution 79.3% (EBITDA Margin :17.4%)

339.1 328.1

-3.3%

4Q11 4Q10 2011 2010

1,584.6

1,243.6

-21.5%

*Eliminations not considered

EBITDA

30

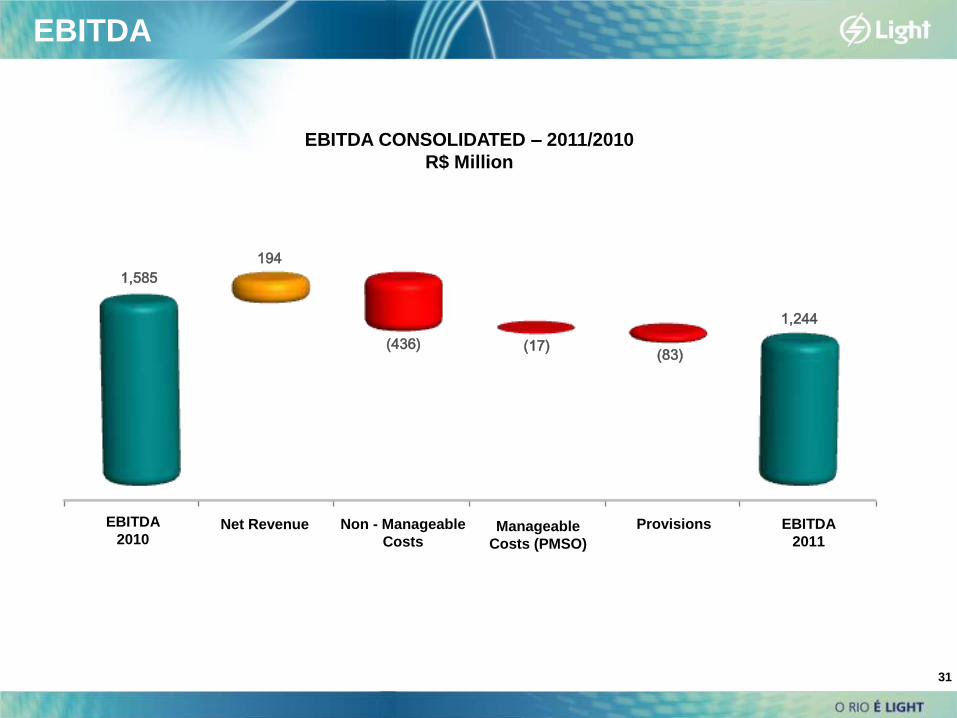

EBITDA - 2010 Receita Líquida Custos Não Gerenciáveis

Custos Gerenciáveis

(PMSO)

Provisões EBITDA - 2011

EBITDA - 2011/2010 - R$ Milhões

EBITDA CONSOLIDATED – 2011/2010

R$ Million

EBITDA

2010 Non - Manageable

Costs

Provisions EBITDA

2011

1,585

194

(436) (17) (83)

1,244

Net Revenue Manageable

Costs (PMSO)

31

EBITDA

2010 EBITDA Resultado Financeiro

Impostos Outros 2011

Lucro Líquido - Semestre

R$ MilhõesNET INCOME

R$ MILLION

2010 EBITDA Financial

Result Taxes Others 2011

575

(341)

(138)

243

(28)

311

Net Income

32

2007 2008 2009 2010 2011

33

PAYOUT AND DIVIDEND POLICY

Dividends (R$ MN) Dividend Yield*

DIVIDENDS AND DIVIDEND YIELD

Dividends

•Based on the closing price of the day before the announcement •Based on Net Income of the year, before IFRS adjustments

1H08 2H08 2H09 1H11 1H09 1H10 2H10 2H11

Interest on Equity (R$ MN)

1S08 2S08 1S09 2S09 1S10 2S10 1S11 2S11 1S121H12

203

351 408

187

432

363 351

205

87

118

182

4.2%

8.2%

1.7%

6.1%

9.9% 8.1% 8.1%

3.4% 3.3%

100% 100%

76.3%

2007 2008 2009*

Payout

50%

2010

81.0%

Dividend Policy

2007 2008 2009 2010 9M112011

100%

2007 2008 2009 2010 2011

2007 2008 2009 2010 2011

DL/EBITDA

DL/EBITDA

34

Indebtedness leverage

¹ Net debt = total debt (excludes pension fund liabilities) – cash

² EBITDA Pro Forma, not considering costs of profit sharing costs in 2007.

Net Debt¹ (R$ MM) and Net Debt / EBITDA

Net Debt Net Debt/ EBITDA

Rating

(brA - )

Investment

Grade

(brA)

20072

1,580

2008

1,637

2009

1,947

1,462

2010

1.3 1.1 1.2 1.2

2011

3,383

2.7

Rating

(brA + )

Rating

(Aa2.br)

Rating

(AA-(bra))

Dec/11

2011

2008 2009 2010 2011

Custo Nominal Custo Real

2012 2013 2014 2015 2016 Após 2016

jan/10 jan/11

Maturity: 2.8 years

AMORTIZATION * (R$ MN)

421

541

778

581 680 598

2010 2009 2008

Dec/11 Dec/10

3,383.2

1,947.4

NET DEBT EVOLUTION

1.2 2.7

2007 2008 2009 set/10

Custo Real Custo Nominal

2007 2008 2009 set/10

Custo Real Custo Nominal

2007 2008 2009 set/10

Custo Real Custo Nominal

4.51%

11.01%

7.62%

13.97%

5.30%

9.84%

4.88%

11.08%

COST OF DEBT

2011

US$/Euro

0.7%*

CDI/Selic

69.0%

TJLP

30.3%

After 2016

* Only Principal

Nominal Cost Real Cost

* Considering Hedge

Indebtedness

35

2007 2008 2009 2010 2011

CAPEX BREAKDOWN (R$MM)

2011

2009 2008 2007

563.8 546.7

CAPEX (R$MN)

700.6

2010 2011

+32.5%

354.7

928.6

Transfer of funds (R$MN)

2011

RENOVA 360.0

BELO MONTE 37.7

AXXIOM 1.0

LIGHT SOLUÇÕES 1.3

E-POWER 0.3

ITAOCARA 7.2

LIGHTGER 4.6

TOTAL 412.1

Develop. of Distribution

SystemR$ 390.1

Losses CombatR$ 184.3

Quality Improvements

R$ 200.5

New Generation

Projects

R$ 60.8

Generation Maintenance

R$ 29.0

OthersR$ 63.9

Investments

36

37

This presentation may include declarations that represent forward-looking statements according to Brazilian regulations and

international movable values. These declarations are based on certain assumptions and analyses made by the Company in

accordance with its experience, the economic environment, market conditions and future events expected, many of which

are out of the Company’s control. Important factors that can lead to significant differences between the real results and the

future declarations of expectations on events or business-oriented results include the Company’s strategy, the Brazilian and

international economic conditions, technology, financial strategy, developments of the public service industry, hydrological

conditions, conditions of the financial market, uncertainty regarding the results of its future operations, plain, goals,

expectations and intentions, among others. Because of these factors, the Company’s actual results may significantly differ

from those indicated or implicit in the declarations of expectations on events or future results.

The information and opinions herein do not have to be understood as recommendation to potential investors, and no

investment decision must be based on the veracity, the updated or completeness of this information or opinions. None of the

Company’s assessors or parts related to them or its representatives will have any responsibility for any losses that can

elapse from the use or the contents of this presentation.

This material includes declarations on future events submitted to risks and uncertainties, which are based on current

expectations and projections on future events and trends that can affect the Company’s businesses. These declarations

include projections of economic growth and demand and supply of energy, in addition to information on competitive position,

regulatory environment, potential growth opportunities and other subjects. Various factors can adversely affect the estimates

and assumptions on which these declarations are based on.

Important Notice

38

Annex

39

Highlights

Geographic Distribution

Energy Auctions

Inventaries

Basic projects

Wind projects

1st listed renewables company on

BM&FBovespa

Former prospections assured one of the best

spots for wind projects

1.461 MW in SHPs projects

2.042 MW in Wind projects

Top of the class suppliers and strong

financial sponsors

Origination and organization of project

finance

42 MW operating trough 3 SHPs (2008)

1.096 MW wind energy already contracted

1.096 MW of

wind energy in

implementation

42MW of SHPs

in operation

The largest seller in 2009 reserve

energy auction

Renova

The largest seller in 2010 reserve

energy auction

The second largest seller in 2011

reserve energy auction

Tariff Readjustment

Financial

Additions

2010

Economic

Readjustmen

t

Average

Perception for

Consumers

-1.33%

+7.90% +7.21%

~ +

Financial

Additions

2011

- 0.64%

-

Total

Readjustmen

t

+6.57%

=

Captive 7.79%

HV 4.64%

MV 7.77%

LV 7.98%

Free 8.06%

HV 7.14%

MV 9.65%

LV 11.07%

Gen. 7.27%

Distr. 11.92%

Starting November , 7, consumers will notice, on average, an increase of 7.90% on tariffs

40

3rd Tariff Review – Final Proposal

41

X Factor Formula: X = Pd + Q + T

Formula: Pd (i=Light) = 1.11% + 0.313 x (VarMWh (Light) – 4.25%) – 0.260 x (VarUC (Light) – 3.58%)

Q = Crossing matrix: Quality Index.i = ½ x (ELC realized/ELC limit + EFC realized/EFC limit) – Comparison with peers over quartiles =

general rule, best and worst performance with the annual quality evolution. Result between +1.0% and -1.0%;

T: Trend between the update of the operating costs defined in the second Tariff Review, considering the productivity gains and real

costs updated - Interval = 99% and 119%. Result between +2.0% and -2.0%.

Accounting: Special Obligation account;

Due date: It will be deducted of the RAB (Regulatory Asset Base) from the 4th Tariff Review on, in the case of Light in 2018

Main objective: These revenues would become investment in the concession area with no regulatory remuneration, instead of reducing

the company’s required revenue.

Others Revenues

WACC Component Formula 3rd Tariff Revision 2nd Tariff Revision

Business and financial risk premium b.(rm-rf) 4.31% 4.70%

Country risk rb 4.25% 4.91%

Nominal cost of equity rp 13.43% 16.71%

Real cost of equity 10.72% 13.75%

Cost of Debt

Credit risk rc 2.14% 2.96%

Nominal cost of debt rd 11.26% 14.97%

Real cost of debt 8.60% 12.06%

Weighted Average Cost (with 34% of taxes)

Nominal WACC after tax rwacc 10.13% 12.81%

Real WACC after tax rwacc 7.50% 9.95%

Capital Structure

Equity 45.00% 42.84%

Debt 55.00% 57.16%

42

Contacts

João Batista Zolini

Carneiro CFO and IRO

Gustavo Werneck IR Manager

+ 55 21 2211 2560

www.light.com.br/ri