Embed Size (px)

Citation preview

©AmBev

MBA PRESENTATIONJOAO CASTRO NEVES – AMBEV CEOSÃO PAULO, MAY 2009

NELSON JAMEL – AMBEV CFO

JUNE 2009

O conteúdo desta apresentação é de propriedade da AmBev.

O conteúdo desta apresentação é de propriedade da AmBev.

WHO ARE WE?

O conteúdo desta apresentação é de propriedade da AmBev.

• Beer and Soft Drinks

– Start up operations

–Growth potential

• Beer and Soft Drinks

– Market Leader in Argentina,

Bolivia, Paraguay and Uruguay

– EBITDA Margin 08 – 45.2%

• Beer

– EBITDA Margin 08 – 38.7%

– Market Share of 43%

• Beer

– 3 major brands

– EBITDA Margin 08 – 48%

– Market Share of 67.5%

• Soft Drinks and Nanc

– EBITDA Margin 08 – 43.5%

– Market Share of 17.7%

2008• Sales Volumes –147 mm Hl

• EBITDA – R$ 9.0 Billion

• EBITDA Margin – 43.1%

• Market cap – USD 30.8 billion (04/09)

2008

O conteúdo desta apresentação é de propriedade da AmBev.5

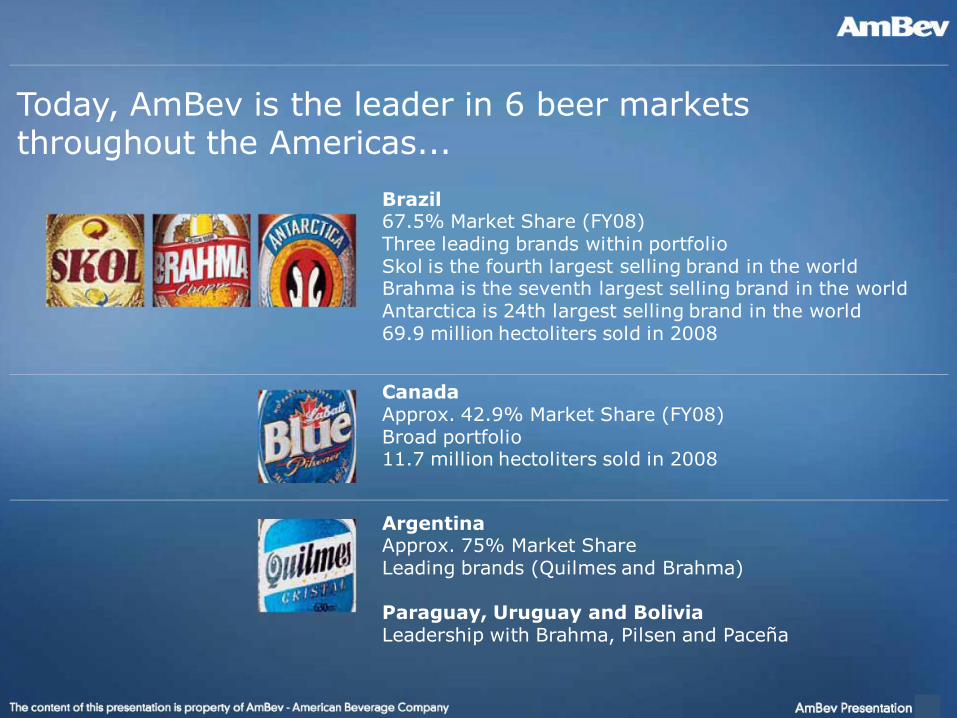

Brazil67.5% Market Share (FY08) Three leading brands within portfolioSkol is the fourth largest selling brand in the worldBrahma is the seventh largest selling brand in the worldAntarctica is 24th largest selling brand in the world 69.9 million hectoliters sold in 2008

ArgentinaApprox. 75% Market ShareLeading brands (Quilmes and Brahma)

Paraguay, Uruguay and BoliviaLeadership with Brahma, Pilsen and Paceña

CanadaApprox. 42.9% Market Share (FY08)Broad portfolio11.7 million hectoliters sold in 2008

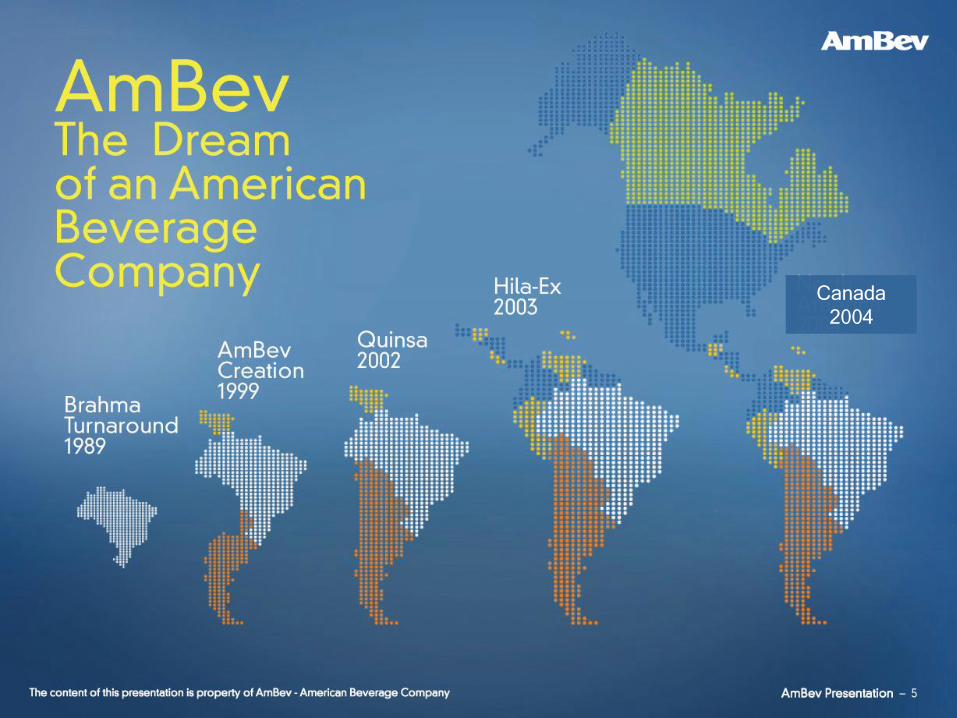

Today, AmBev is the leader in 6 beer markets throughout the Americas...

O conteúdo desta apresentação é de propriedade da AmBev.

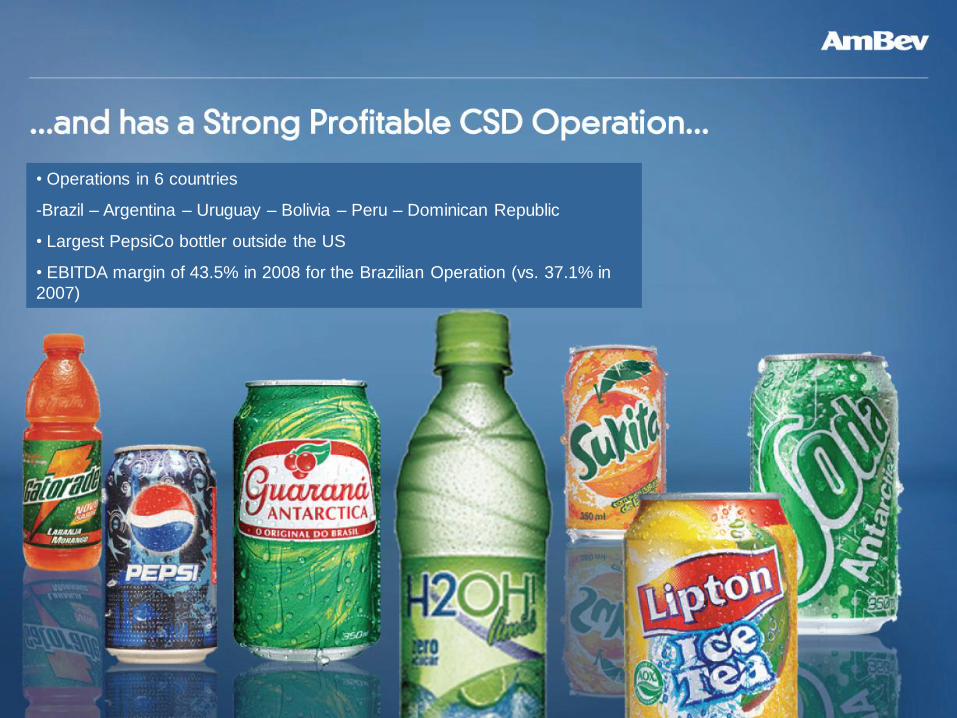

• Operations in 6 countries

-Brazil – Argentina – Uruguay – Bolivia – Peru – Dominican Republic

• Largest PepsiCo bottler outside the US

• EBITDA margin of 43.5% in 2008 for the Brazilian Operation (vs. 37.1% in

2007)

O conteúdo desta apresentação é de propriedade da AmBev.7

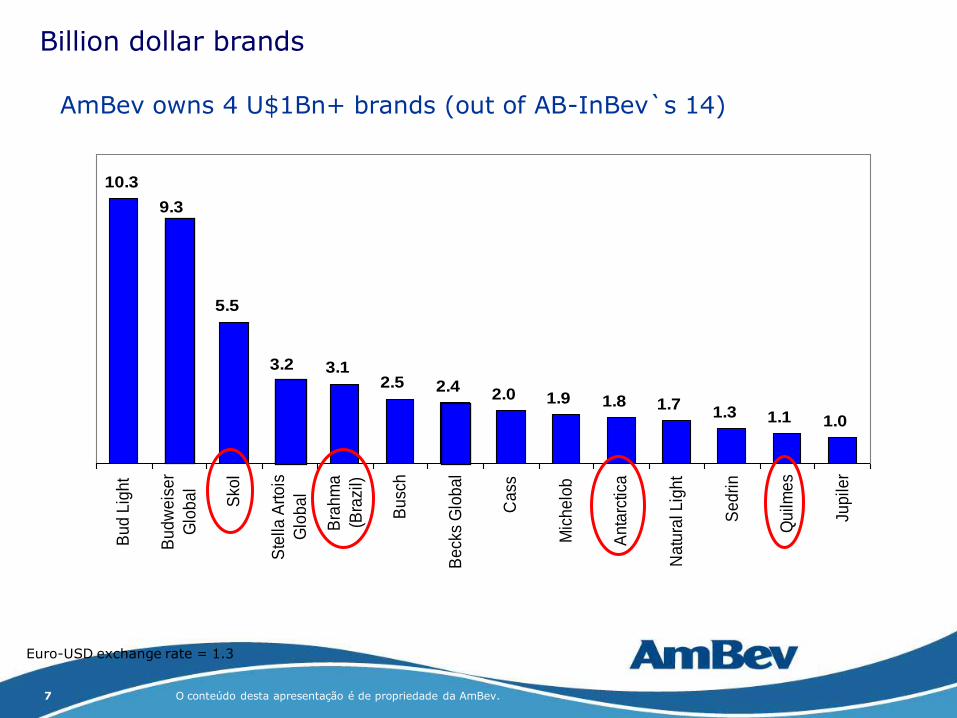

AmBev owns 4 U$1Bn+ brands (out of AB-InBev`s 14)

Billion dollar brands

Euro-USD exchange rate = 1.3

10.3

9.3

5.5

3.2 3.1 2.5 2.4

2.0 1.9 1.8 1.7 1.3 1.1 1.0

Bu

d L

igh

t

Bu

dw

eis

er

Glo

ba

l

Sko

l

Ste

lla A

rto

is

Glo

ba

l

Bra

hm

a

(Bra

zil)

Bu

sch

Be

cks

Glo

ba

l

Ca

ss

Mic

he

lob

An

tarc

tica

Na

tura

l Lig

ht

Se

dri

n

Qu

ilme

s

Jup

iler

O conteúdo desta apresentação é de propriedade da AmBev.8

O conteúdo desta apresentação é de propriedade da AmBev.

•To be the best beer company

in a better world

•Targets and results

•Social Responsibility

•Competitive Advantage

•Compensation

•Leadership development

•Career development

•Training

•Vision

•Mission

•Principles

•Meritocracy

•Ownership

•Consistency

•Long term commitment

•Candor

O conteúdo desta apresentação é de propriedade da AmBev.

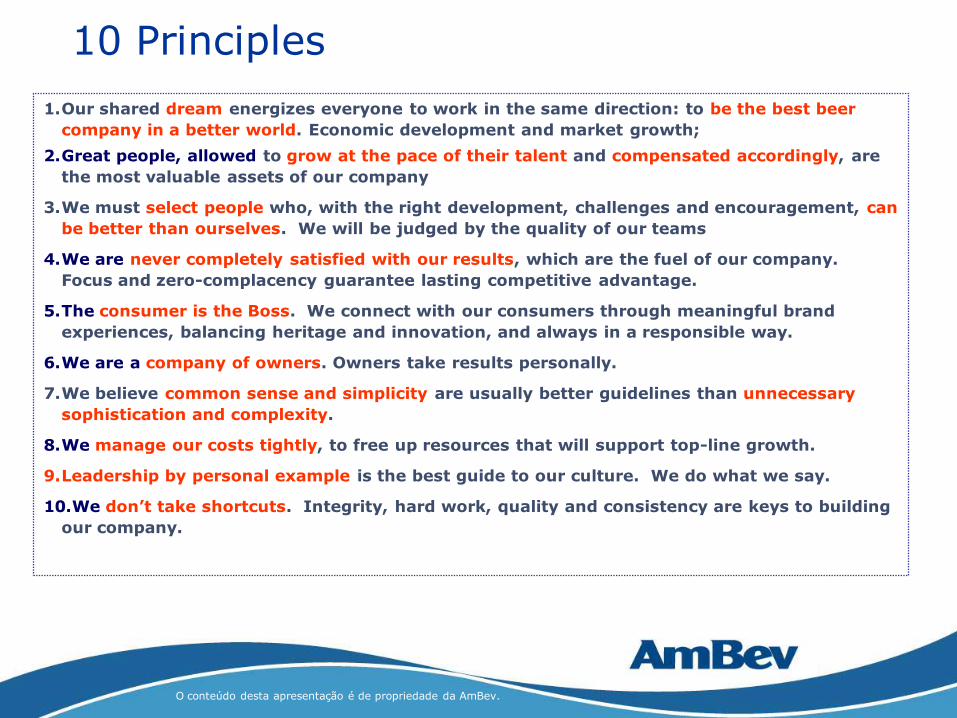

10 Principles

1.Our shared dream energizes everyone to work in the same direction: to be the best beer

company in a better world. Economic development and market growth;

2.Great people, allowed to grow at the pace of their talent and compensated accordingly, are

the most valuable assets of our company

3.We must select people who, with the right development, challenges and encouragement, can

be better than ourselves. We will be judged by the quality of our teams

4.We are never completely satisfied with our results, which are the fuel of our company.

Focus and zero-complacency guarantee lasting competitive advantage.

5.The consumer is the Boss. We connect with our consumers through meaningful brand

experiences, balancing heritage and innovation, and always in a responsible way.

6.We are a company of owners. Owners take results personally.

7.We believe common sense and simplicity are usually better guidelines than unnecessary

sophistication and complexity.

8.We manage our costs tightly, to free up resources that will support top-line growth.

9.Leadership by personal example is the best guide to our culture. We do what we say.

10.We don’t take shortcuts. Integrity, hard work, quality and consistency are keys to building

our company.

O conteúdo desta apresentação é de propriedade da AmBev.

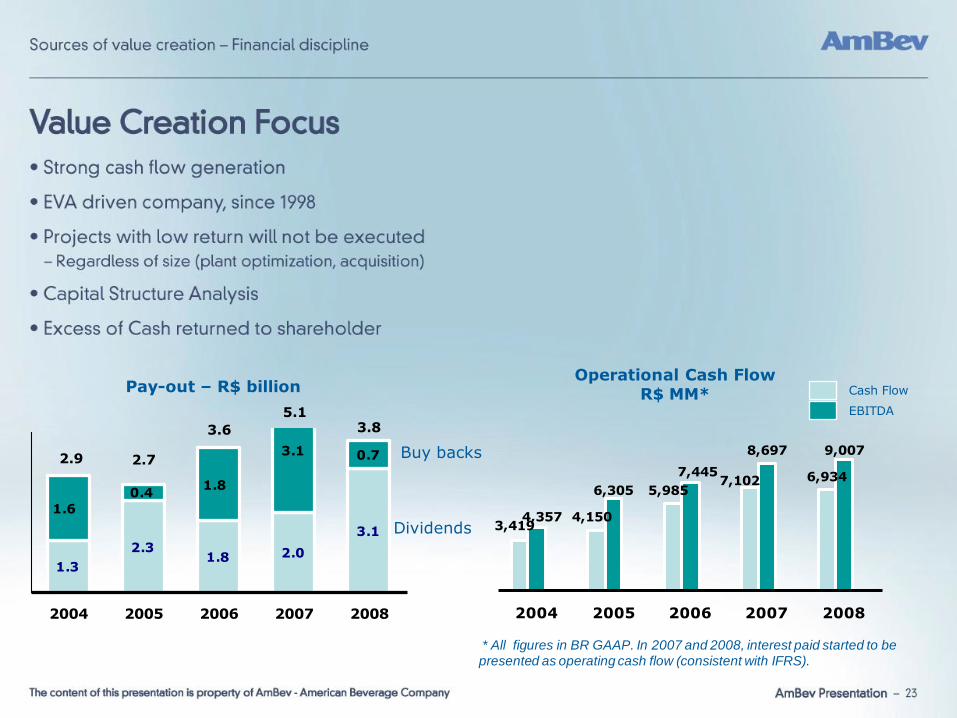

Pay-out – R$ billion

1.6

1.8

3.1 0.7

1.3

2.31.8 2.0

3.1

0.4

2004 2005 2006 2007 2008

Buy backs

Dividends

2.9 2.7

3.6

6,934

8,697 9,007

7,1025,985

4,1503,419

7,445

6,305

4,357

2004 2005 2006 2007 2008

Operational Cash FlowR$ MM* Cash Flow

EBITDA

* All figures in BR GAAP. In 2007 and 2008, interest paid started to be

presented as operating cash flow (consistent with IFRS).

5.13.8

O conteúdo desta apresentação é de propriedade da AmBev.

• First company in it’s industry to be certified by the United Nations for the

sale of carbon credits

O conteúdo desta apresentação é de propriedade da AmBev.

WHERE DO WE COME FROM?

O conteúdo desta apresentação é de propriedade da AmBev.14

Canada

2004

O conteúdo desta apresentação é de propriedade da AmBev.15

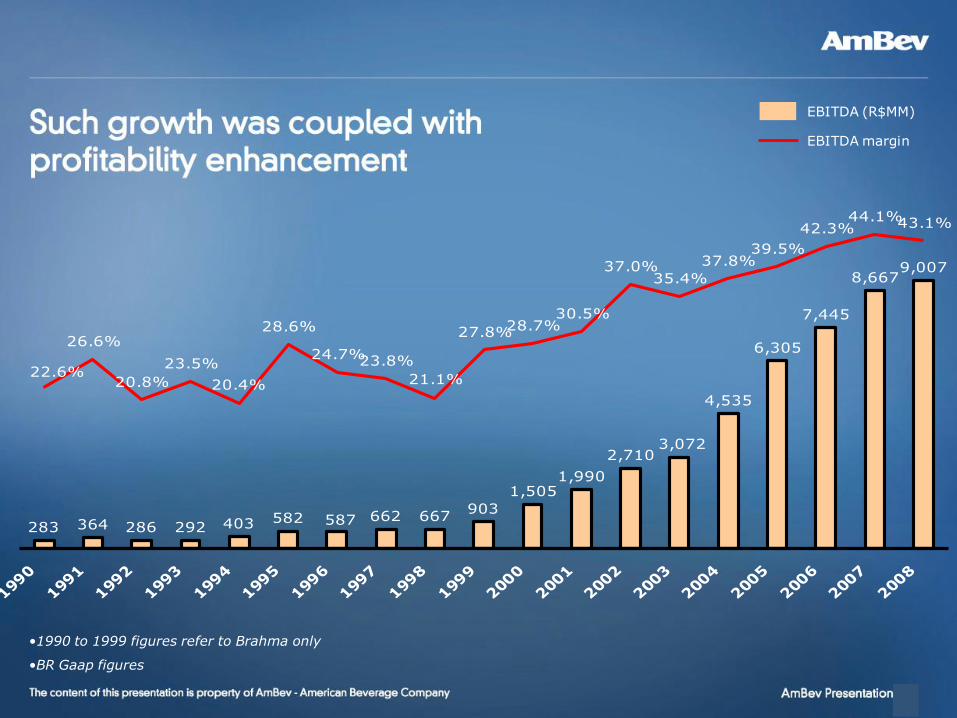

283 364 286 292 403 582 662 667903

1,5051,990

2,710

4,535

6,305

7,445

8,6679,007

3,072

587

23.8%

27.8%28.7%30.5%

37.0%35.4%

37.8%39.5%

42.3%44.1%43.1%

21.1%22.6%

26.6%

20.8%

23.5%

20.4%

28.6%

24.7%

199

0

199

1

199

2

199

3

199

4

199

5

199

6

199

7

199

8

199

9

200

0

200

1

200

2

200

3

200

4

200

5

200

6

200

7

200

8

EBITDA (R$MM)

EBITDA margin

•1990 to 1999 figures refer to Brahma only

•BR Gaap figures

O conteúdo desta apresentação é de propriedade da AmBev.

2009 Results so far ...

O conteúdo desta apresentação é de propriedade da AmBev.

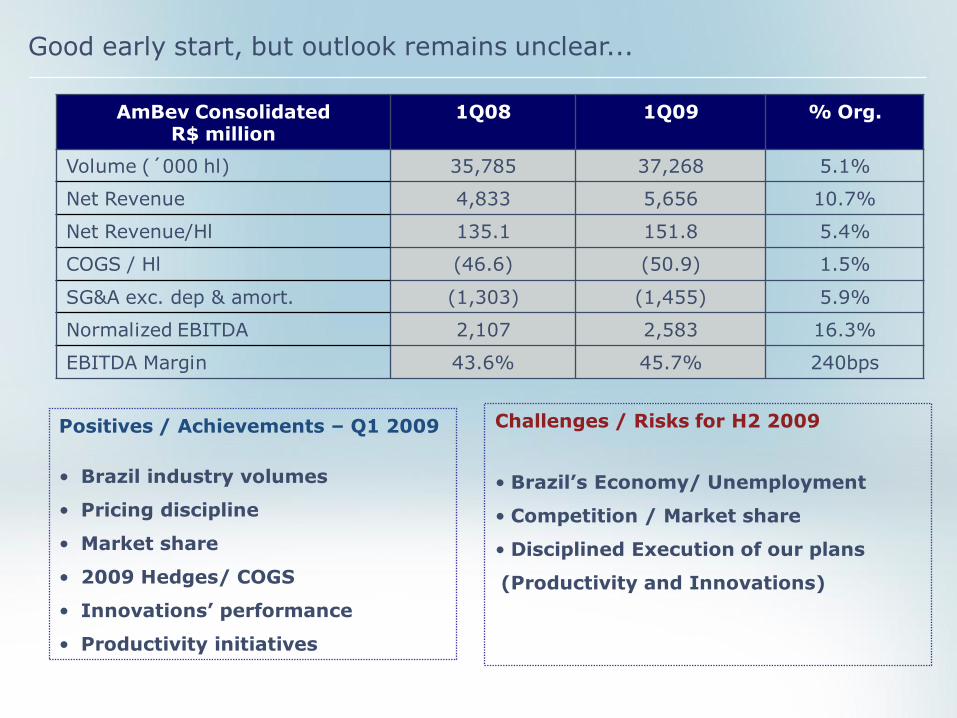

AmBev Consolidated R$ million

1Q08 1Q09 % Org.

Volume (´000 hl) 35,785 37,268 5.1%

Net Revenue 4,833 5,656 10.7%

Net Revenue/Hl 135.1 151.8 5.4%

COGS / Hl (46.6) (50.9) 1.5%

SG&A exc. dep & amort. (1,303) (1,455) 5.9%

Normalized EBITDA 2,107 2,583 16.3%

EBITDA Margin 43.6% 45.7% 240bps

Good early start, but outlook remains unclear...

Positives / Achievements – Q1 2009

• Brazil industry volumes

• Pricing discipline

• Market share

• 2009 Hedges/ COGS

• Innovations’ performance

• Productivity initiatives

Challenges / Risks for H2 2009

• Brazil’s Economy/ Unemployment

• Competition / Market share

• Disciplined Execution of our plans

(Productivity and Innovations)

O conteúdo desta apresentação é de propriedade da AmBev.

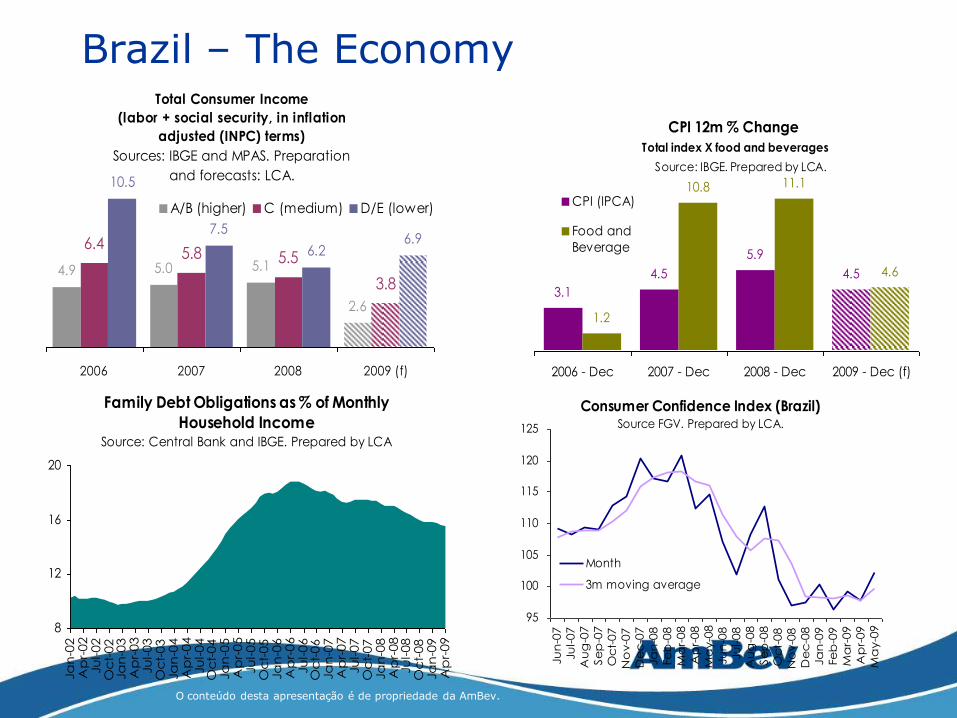

Brazil – The EconomyTotal Consumer Income

(labor + social security, in inflation

adjusted (INPC) terms)

Sources: IBGE and MPAS. Preparation

and forecasts: LCA.

4.9 5.0 5.1

2.6

6.45.8 5.5

3.8

10.5

7.5

6.26.9

2006 2007 2008 2009 (f)

A/B (higher) C (medium) D/E (lower)

CPI 12m % Change

Total index X food and beverages

Source: IBGE. Prepared by LCA.

3.1

4.5

5.9

4.5

1.2

10.8 11.1

4.6

2006 - Dec 2007 - Dec 2008 - Dec 2009 - Dec (f)

CPI (IPCA)

Food and

Beverage

Family Debt Obligations as % of Monthly

Household IncomeSource: Central Bank and IBGE. Prepared by LCA

8

12

16

20

Ja

n-0

2A

pr-

02

Ju

l-02

Oc

t-02

Ja

n-0

3A

pr-

03

Ju

l-03

Oc

t-03

Ja

n-0

4A

pr-

04

Ju

l-04

Oc

t-04

Ja

n-0

5A

pr-

05

Ju

l-05

Oc

t-05

Ja

n-0

6A

pr-

06

Ju

l-06

Oc

t-06

Ja

n-0

7A

pr-

07

Ju

l-07

Oc

t-07

Ja

n-0

8A

pr-

08

Ju

l-08

Oc

t-08

Ja

n-0

9A

pr-

09

Consumer Confidence Index (Brazil)Source FGV. Prepared by LCA.

95

100

105

110

115

120

125

Ju

n-0

7

Ju

l-07

Au

g-0

7

Se

p-0

7

Oc

t-07

No

v-0

7

De

c-0

7

Ja

n-0

8

Fe

b-0

8

Ma

r-08

Ap

r-08

Ma

y-0

8

Ju

n-0

8

Ju

l-08

Au

g-0

8

Se

p-0

8

Oc

t-08

No

v-0

8

De

c-0

8

Ja

n-0

9

Fe

b-0

9

Ma

r-09

Ap

r-09

Ma

y-0

9

Month

3m moving average

O conteúdo desta apresentação é de propriedade da AmBev.

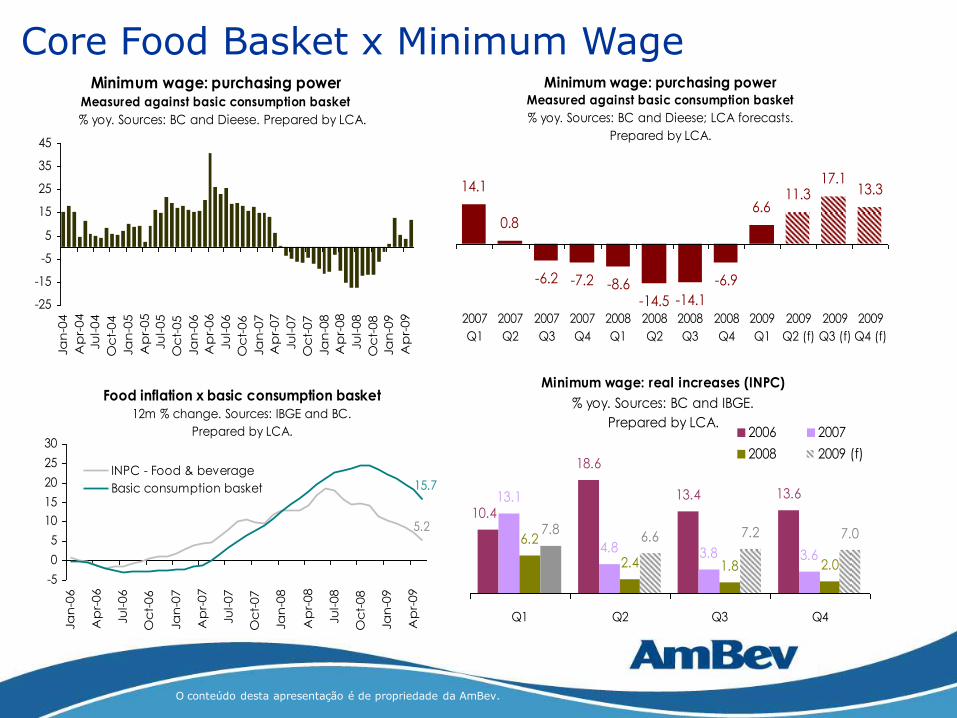

Core Food Basket x Minimum WageMinimum wage: purchasing power

Measured against basic consumption basket

% yoy. Sources: BC and Dieese. Prepared by LCA.

-25

-15

-5

5

15

25

35

45

Ja

n-0

4

Ap

r-04

Ju

l-04

Oc

t-04

Ja

n-0

5

Ap

r-05

Ju

l-05

Oc

t-05

Ja

n-0

6

Ap

r-06

Ju

l-06

Oc

t-06

Ja

n-0

7

Ap

r-07

Ju

l-07

Oc

t-07

Ja

n-0

8

Ap

r-08

Ju

l-08

Oc

t-08

Ja

n-0

9

Ap

r-09

Minimum wage: purchasing powerMeasured against basic consumption basket

% yoy. Sources: BC and Dieese; LCA forecasts.

Prepared by LCA.

14.1

0.8

11.317.1

13.36.6

-6.9

-14.1-14.5-8.6-7.2-6.2

2007

Q1

2007

Q2

2007

Q3

2007

Q4

2008

Q1

2008

Q2

2008

Q3

2008

Q4

2009

Q1

2009

Q2 (f)

2009

Q3 (f)

2009

Q4 (f)

Food inflation x basic consumption basket

12m % change. Sources: IBGE and BC.

Prepared by LCA.

5.2

15.7

-5

0

5

10

15

20

25

30

Ja

n-0

6

Ap

r-06

Ju

l-06

Oc

t-06

Ja

n-0

7

Ap

r-07

Ju

l-07

Oc

t-07

Ja

n-0

8

Ap

r-08

Ju

l-08

Oc

t-08

Ja

n-0

9

Ap

r-09

INPC - Food & beverage

Basic consumption basket

Minimum wage: real increases (INPC)

% yoy. Sources: BC and IBGE.

Prepared by LCA.

18.6

13.4 13.613.1

4.8 3.8 3.66.2

2.4 1.8 2.0

7.86.6 7.2 7.0

10.4

Q1 Q2 Q3 Q4

2006 2007

2008 2009 (f)

O conteúdo desta apresentação é de propriedade da AmBev.

THE FUTURE...

O conteúdo desta apresentação é de propriedade da AmBev.

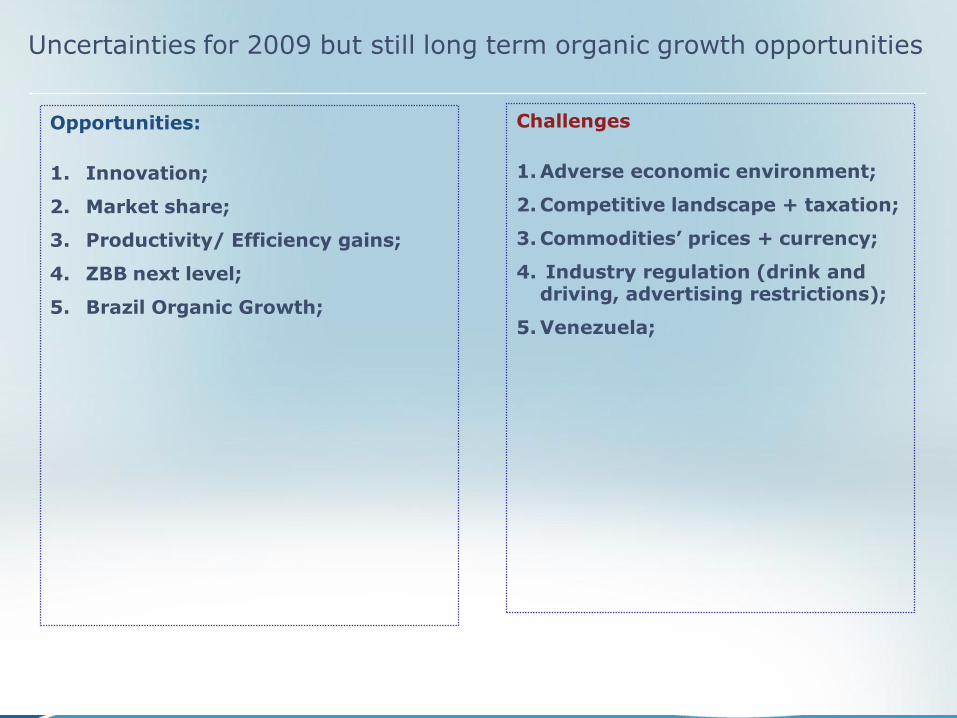

Uncertainties for 2009 but still long term organic growth opportunities

Opportunities:

1. Innovation;

2. Market share;

3. Productivity/ Efficiency gains;

4. ZBB next level;

5. Brazil Organic Growth;

Challenges

1. Adverse economic environment;

2. Competitive landscape + taxation;

3. Commodities’ prices + currency;

4. Industry regulation (drink and driving, advertising restrictions);

5. Venezuela;

O conteúdo desta apresentação é de propriedade da AmBev.

BRAZIL OVERVIEW

O conteúdo desta apresentação é de propriedade da AmBev.

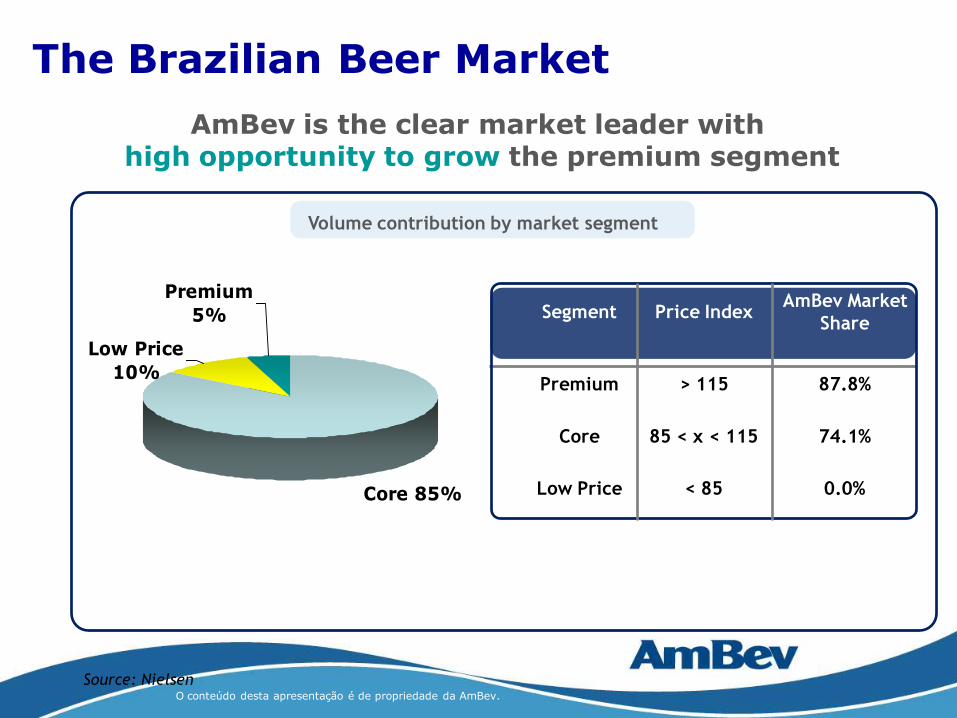

The Brazilian Beer Market

84.087.1

91.6 95.4101.0 102.9

2003 2004 2005 2006 2007 2008

Beer volume – Brazil (million HL)

The 4th largest beer market in the world and growing

(2nd largest profit pool behind only the US)

115 113

159

110

9587 84 82 79

58

Czech

Republic

Ireland Germany Austria Venezuela UK USA Spain Russia Brazil

Per Capita Beer Consumption 2008 (in liters)

O conteúdo desta apresentação é de propriedade da AmBev.

32%

47%

21%

40%

60%

The Brazilian Beer Market

Beer market is concentrated in AmBev’s strongholds

Grocery Stores

On premise (Bar)

Supermarkets

Volume contribution by chanel - 2008

Beer Blast Others

Volume contribution by Occasion - 2008

Returnable

Disposable

Volume contribution by Packaging - 2008

Source: Nielsen. Ipsos

65%

35%

O conteúdo desta apresentação é de propriedade da AmBev.

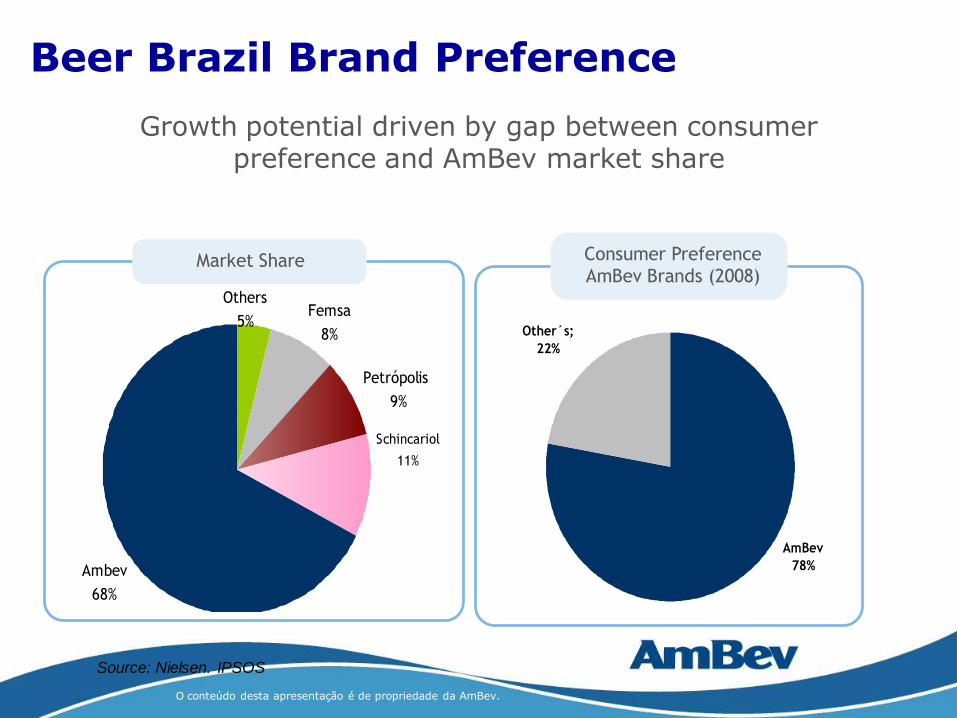

Beer Brazil Brand Preference

Growth potential driven by gap between consumerpreference and AmBev market share

Market Share

Ambev

68%

Schincariol

11%

Petrópolis

9%

Femsa

8%

Others

5%

Source: Nielsen. IPSOS

Consumer Preference AmBev Brands (2008)

AmBev

78%

Other´s;

22%

O conteúdo desta apresentação é de propriedade da AmBev.

Premium

5%

Low Price

10%

Core 85%

Segment Price IndexAmBev Market

Share

Premium > 115 87.8%

Core 85 < x < 115 74.1%

Low Price < 85 0.0%

Source: Nielsen

The Brazilian Beer Market

AmBev is the clear market leader with high opportunity to grow the premium segment

Volume contribution by market segment

O conteúdo desta apresentação é de propriedade da AmBev.

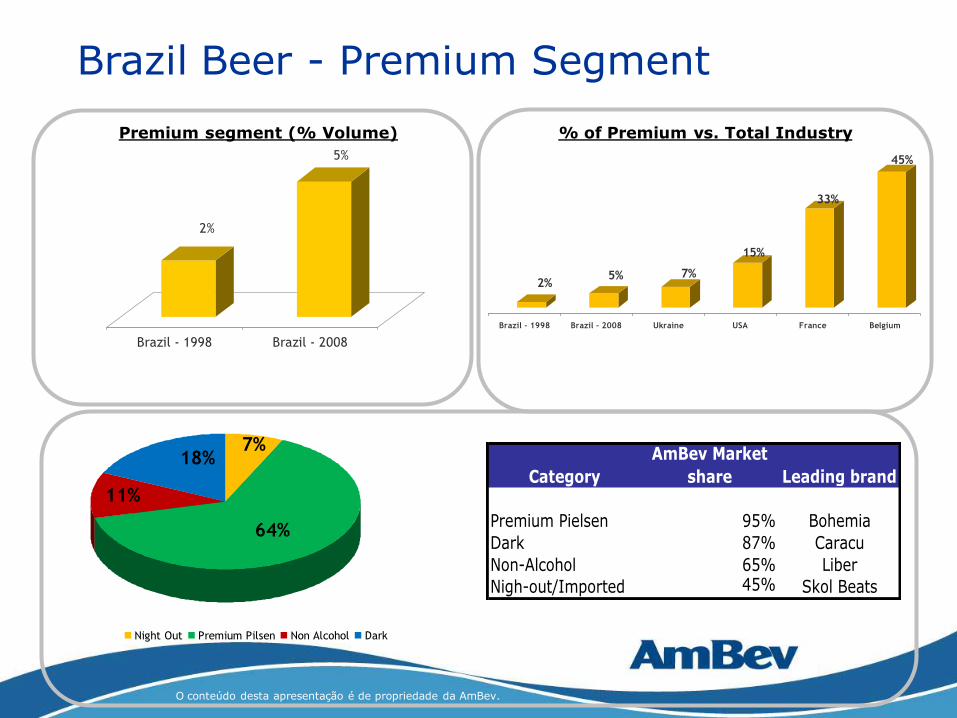

% of Premium vs. Total IndustryPremium segment (% Volume)

Brazil Beer - Premium Segment

2%

5%

Brazil - 1998 Brazil - 2008

2%5% 7%

15%

33%

45%

Brazil - 1998 Brazil - 2008 Ukraine USA France Belgium

7%

64%

11%

18%

Night Out Premium Pilsen Non Alcohol Dark

Category

AmBev Market

share Leading brand

Premium Pielsen 95% Bohemia

Dark 87% Caracu

Non-Alcohol 65% Liber

Nigh-out/Imported 45% Skol Beats

O conteúdo desta apresentação é de propriedade da AmBev.

0

20

40

60

80

100

120

okt/05

jan/

06

apr/06

jul/0

6

okt/06

jan/

07

apr/07

jul/0

7

okt/07

jan/

08

apr/08

jul/0

8

okt/08

jan/

09

apr/09

% r

ela

tive s

hare

Heineken Stella Artois

Stella Artois in Argentina:

# 1 international beer < 3 years after launch

28

UK: Market share gain in 2008 after 5 years of consistent declineOur premium experience in Argentina

O conteúdo desta apresentação é de propriedade da AmBev.

Innovations 2007/08

Brahma Historical

cans