Embed Size (px)

Citation preview

PRIVATE EQUITY & VENTURE CAPITALPRIVATE EQUITY & VENTURE CAPITAL

INVESTMENTS IN BRAZILIAN COMPANIESINVESTMENTS IN BRAZILIAN COMPANIES

SÃO PAULO

ALAMEDA SANTOS, 2.335 | 10º E 11º ANDARES | CEP 01419 002SÃO PAULO | SP | BRASIL | TEL 55 11 3082 9398 | FAX 3082 [email protected] | www.mfra.com.br

RIO DE JANEIRO

AV. ALMIRANTE BARROSO, 52 | 5º ANDAR | CEP 20031 000RIO DE JANEIRO | RJ | BRASIL | TEL 55 21 2533 2200 | FAX 2262 [email protected] | www.mfra.com.br

MARCH, 2012MARCH, 2012

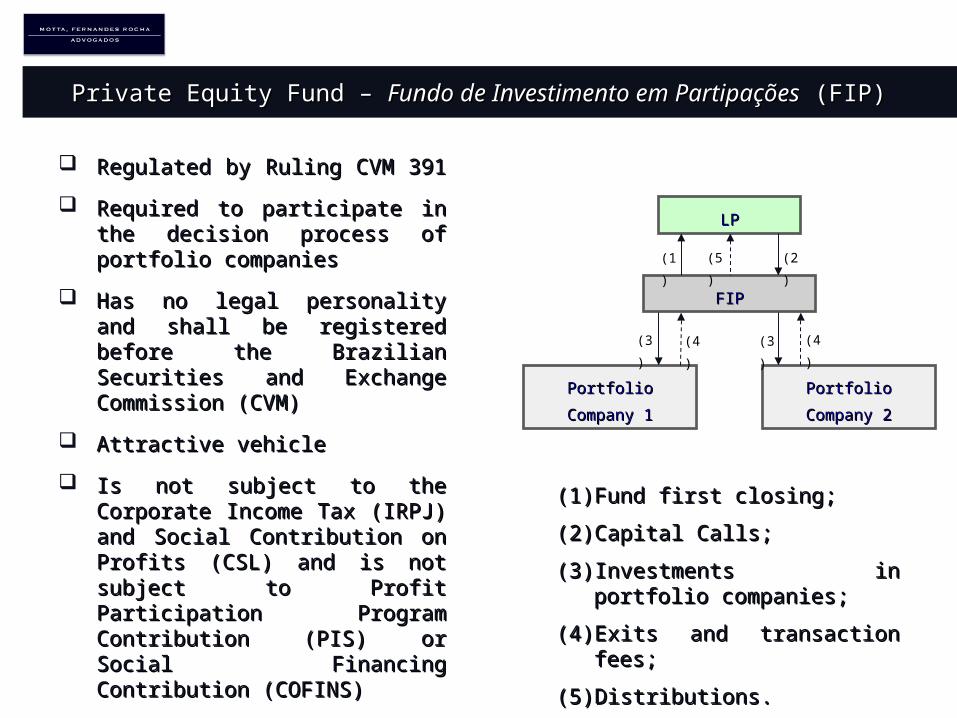

Private Equity Fund – Private Equity Fund – Fundo de Investimento em PartipaçõesFundo de Investimento em Partipações (FIP) (FIP)

Regulated by Ruling CVM 391 Regulated by Ruling CVM 391

Required to participate in the Required to participate in the decision process of portfolio decision process of portfolio companiescompanies

Has no legal personality and Has no legal personality and shall be registered before the shall be registered before the Brazilian Securities and Brazilian Securities and Exchange CommissionExchange Commission (CVM) (CVM)

Attractive vehicle Attractive vehicle

Is not subject to the Corporate Is not subject to the Corporate Income Tax (IRPJ) and Social Income Tax (IRPJ) and Social Contribution on Profits (CSL) and Contribution on Profits (CSL) and is not subject to Profit is not subject to Profit Participation Program Participation Program Contribution (PIS) or Social Contribution (PIS) or Social Financing Contribution (COFINS)Financing Contribution (COFINS)

LPLP

Portfolio Company Portfolio Company

11

FIPFIP

(3)

Portfolio Company Portfolio Company

22

(1) (5) (2)

(4) (3) (4)

(1)(1) Fund first closing; Fund first closing;

(2)(2) Capital Calls;Capital Calls;

(3)(3) Investments in portfolio Investments in portfolio companies;companies;

(4)(4) Exits and transaction fees;Exits and transaction fees;

(5)(5) Distributions.Distributions.

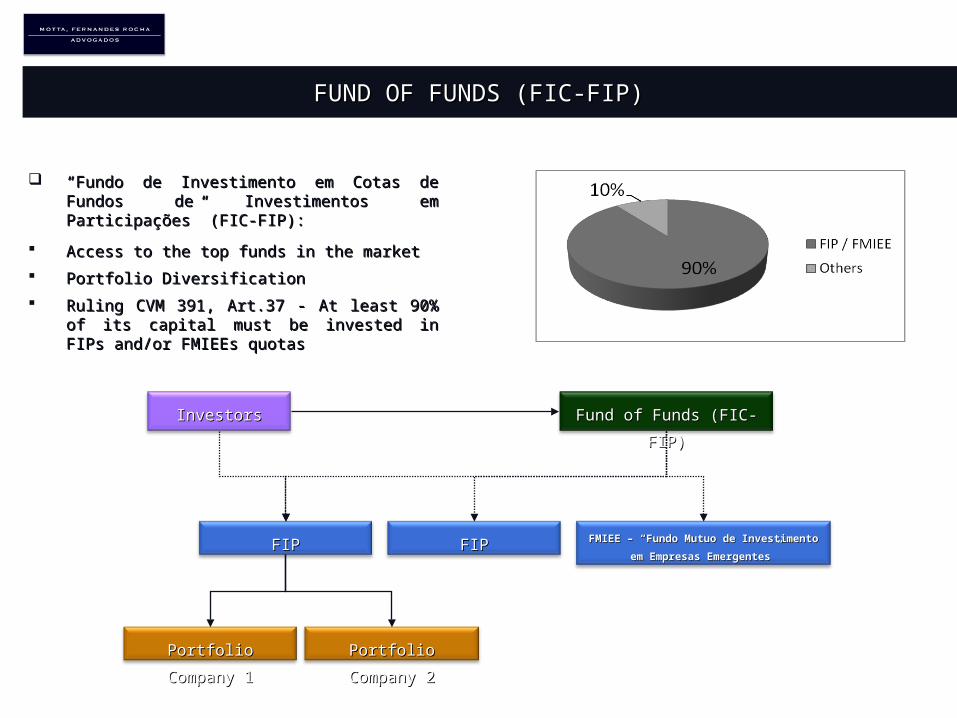

FUND OF FUNDS (FIC-FIP)FUND OF FUNDS (FIC-FIP)

““Fundo de Investimento em Cotas de Fundos Fundo de Investimento em Cotas de Fundos de Investimentos em Participações” (FIC-FIP):de Investimentos em Participações” (FIC-FIP):

Access to the top funds in the market Access to the top funds in the market

Portfolio DiversificationPortfolio Diversification

Ruling CVM 391, Art.37 - At least 90% of its Ruling CVM 391, Art.37 - At least 90% of its capital must be invested in FIPs and/or FMIEEs capital must be invested in FIPs and/or FMIEEs quotasquotas

Portfolio Company Portfolio Company

11

FIPFIP

Portfolio Company Portfolio Company

22

Fund of Funds (FIC-FIP)Fund of Funds (FIC-FIP)InvestorsInvestors

FIPFIP FMIEE – “Fundo Mutuo de FMIEE – “Fundo Mutuo de

Investimento em Empresas Investimento em Empresas

Emergentes”Emergentes”

RESTRICT PLACEMENT EFFORTS RESTRICT PLACEMENT EFFORTS

The Brazilian Securities and Exchange Commission (CVM) issued The Brazilian Securities and Exchange Commission (CVM) issued Instruction 476/09 Instruction 476/09 ruling on public offerings with restricted efforts.ruling on public offerings with restricted efforts.

Public offerings with restricted efforts are those in which the issuers Public offerings with restricted efforts are those in which the issuers do not have to do not have to request previous registration of the issuance before CVMrequest previous registration of the issuance before CVM, as it is usually , as it is usually required in relation to public offerings.required in relation to public offerings.

The public offerings with restricted efforts shall be directed The public offerings with restricted efforts shall be directed exclusively to qualified exclusively to qualified investors investors (minimum subscription of R$ 1,000,000.00), and intermediated by (minimum subscription of R$ 1,000,000.00), and intermediated by members of the system of distribution of securities. The issuers are not allowed to members of the system of distribution of securities. The issuers are not allowed to reach investors through offices nor public means of communication, such as media, reach investors through offices nor public means of communication, such as media, radio, television, and internet.radio, television, and internet.

Public offerings with restricted efforts shall be offered to 50 qualified investors, Public offerings with restricted efforts shall be offered to 50 qualified investors, however however only 20 qualified investors can subscribe or acquire the securitiesonly 20 qualified investors can subscribe or acquire the securities..

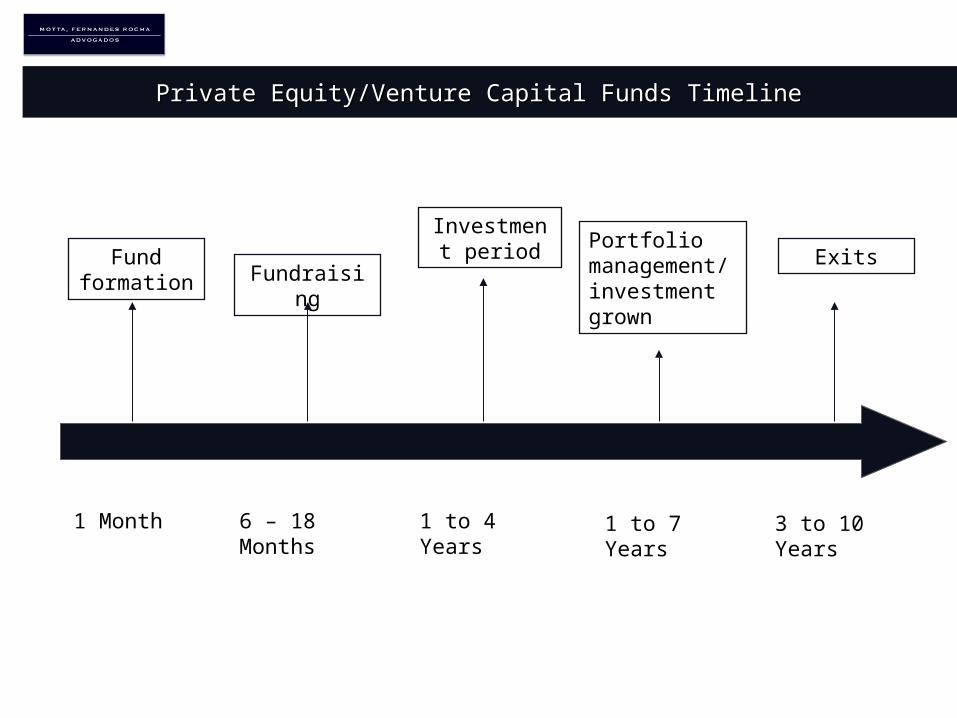

Private Equity/Venture Capital Funds TimelinePrivate Equity/Venture Capital Funds Timeline

Fund formation Fundraising

Investment period Portfolio

management/ investment grown

Exits

1 Month 6 – 18 Months

1 to 4 Years 1 to 7 Years 3 to 10 Years

Tax Chart StructureTax Chart Structure

Foreign InvestorForeign Investor

FIPFIP

Portfolio CompanyPortfolio Company

Abroad

BrazilBrazilian InvestorBrazilian Investor

BuyerBuyer

Foreign InvestorForeign Investor Foreign InvestorForeign Investor

(1)

(3)

(4)(5)

(6)30% 50% 20%

Tax Heaven(7) (8)

(2)

(1)(1) IOF tax rate of 0% to foreign investment fund inflows;IOF tax rate of 0% to foreign investment fund inflows;

(2)(2) Taxation at the level of quotaholders. FIP portfolio is exempt from taxation;Taxation at the level of quotaholders. FIP portfolio is exempt from taxation;

(3)(3) Profits and dividends paid by the portfolio company to FIP are tax exempt;Profits and dividends paid by the portfolio company to FIP are tax exempt;

(4)(4) Capital gain arising from the sale of FIP’s corporate interests on portfolio companies are tax exemptCapital gain arising from the sale of FIP’s corporate interests on portfolio companies are tax exempt..

(5)(5) To Brazilian Investors, income and capital gain in the sale of quotas of the FIP are subject to a income tax rate of 15%.To Brazilian Investors, income and capital gain in the sale of quotas of the FIP are subject to a income tax rate of 15%.

(6)(6) For Foreign Investor, income or capital gain are exempt from tax income if certain conditions are met;For Foreign Investor, income or capital gain are exempt from tax income if certain conditions are met;

(7)(7) In case certain conditions are not observed, the proceeds distributed by the FIP to foreign investor will be subjected to a In case certain conditions are not observed, the proceeds distributed by the FIP to foreign investor will be subjected to a income tax of 15%. (Example: more than 40%)income tax of 15%. (Example: more than 40%)

(8)(8) In case certain conditions are not observed, the proceeds distributed by the FIP to foreign investor will be subjected to a In case certain conditions are not observed, the proceeds distributed by the FIP to foreign investor will be subjected to a income tax of 15%. (Example: Tax Heaven Resident)income tax of 15%. (Example: Tax Heaven Resident)

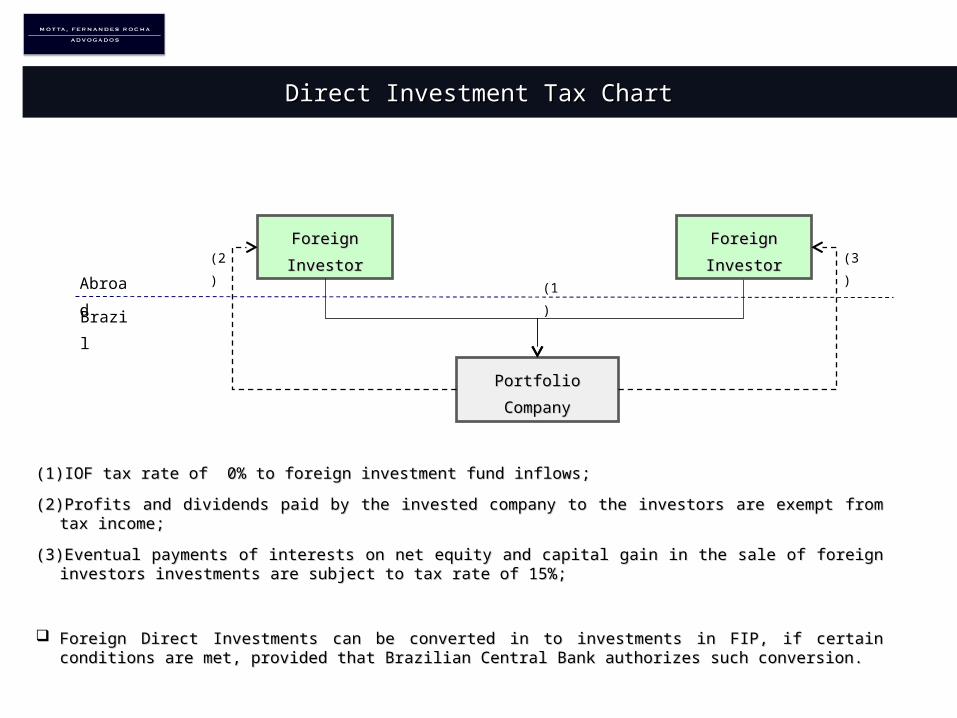

Direct Investment Tax ChartDirect Investment Tax Chart

Foreign InvestorForeign Investor

Portfolio CompanyPortfolio Company

Abroad

Brazil

Foreign InvestorForeign Investor

(1)

(3)(2)

(1)(1) IOF tax rate of 0% to foreign investment fund inflows;IOF tax rate of 0% to foreign investment fund inflows;

(2)(2)Profits and dividends paid by the invested company to the investors are exempt from tax income;Profits and dividends paid by the invested company to the investors are exempt from tax income;

(3)(3)Eventual payments of interests on net equity and capital gain in the sale of foreign investors Eventual payments of interests on net equity and capital gain in the sale of foreign investors investments are subject to tax rate of 15%;investments are subject to tax rate of 15%;

Foreign Direct Investments can be converted in to investments in FIP, if certain conditions are met, Foreign Direct Investments can be converted in to investments in FIP, if certain conditions are met, provided that Brazilian Central Bank authorizes such conversion.provided that Brazilian Central Bank authorizes such conversion.

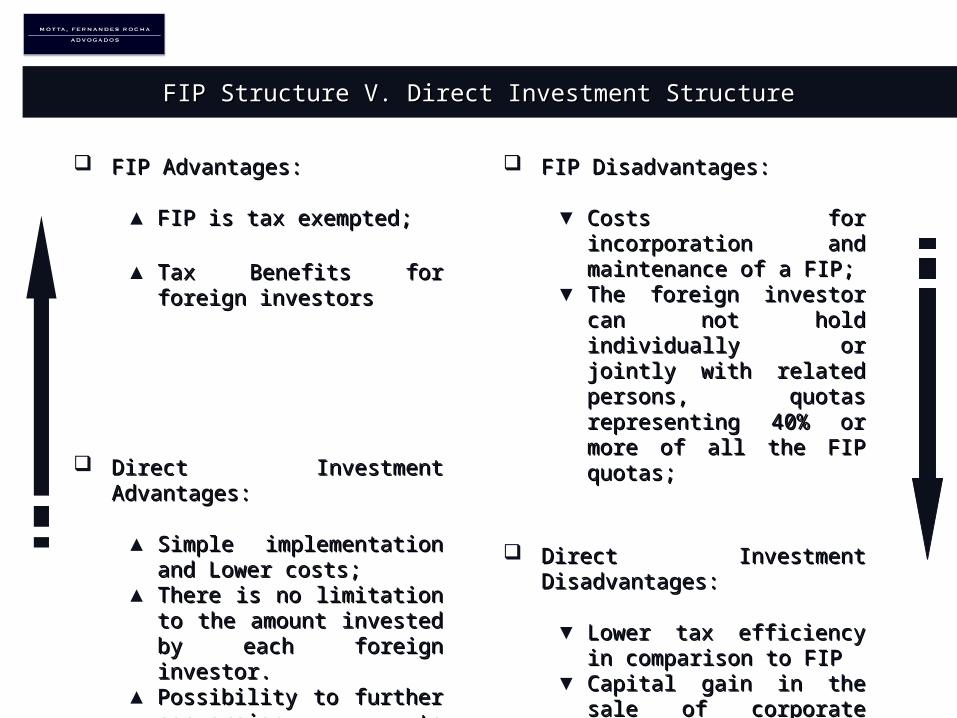

FIP Structure V. Direct Investment StructureFIP Structure V. Direct Investment Structure

FIP FIP Advantages: Advantages:

▲ FIP is tax exempted;FIP is tax exempted;

▲ Tax Benefits for foreign Tax Benefits for foreign investorsinvestors

DirectDirect InvestmentInvestment Advantages: Advantages:

▲ Simple implementation Simple implementation and Lower costs;and Lower costs;

▲ There is no limitation to There is no limitation to the amount invested by the amount invested by each foreign investor.each foreign investor.

▲ Possibility to further Possibility to further conversion to investment conversion to investment in FIP.in FIP.

FIP FIP Disadvantages: Disadvantages:

▼ Costs for incorporation Costs for incorporation and maintenance of a FIP;and maintenance of a FIP;

▼ The foreign investor can The foreign investor can not hold individually or not hold individually or jointly with related jointly with related persons, quotas persons, quotas representing 40% or representing 40% or more of all the FIP more of all the FIP quotas;quotas;

DirectDirect InvestmentInvestment Disadvantages: Disadvantages:

▼ Lower tax efficiency in Lower tax efficiency in

comparison to FIPcomparison to FIP▼ Capital gain in the sale of Capital gain in the sale of

corporate interests is corporate interests is subjected to a 15% subjected to a 15% income tax rate.income tax rate.

INOVAR PROJECT – GENERAL INFORMATIONINOVAR PROJECT – GENERAL INFORMATION

THE PROJECT:THE PROJECT:

• INOVAR PROJECT was launched in May 2000 as a strategic action of FINEP and its INOVAR PROJECT was launched in May 2000 as a strategic action of FINEP and its aim is to promote the development of private equity and venture capital. aim is to promote the development of private equity and venture capital.

• Although Brazil has pre-conditions to develop venture capital and private equity, Although Brazil has pre-conditions to develop venture capital and private equity, this emerging market in the country lacks a comprehensive institutional structure this emerging market in the country lacks a comprehensive institutional structure that can bring the various interested agents together, combining their efforts for that can bring the various interested agents together, combining their efforts for one common purpose. Acting in partnership with agencies and pension funds, the one common purpose. Acting in partnership with agencies and pension funds, the Inovar Project has been seeking to build an institutional framework – a bridge Inovar Project has been seeking to build an institutional framework – a bridge between managers and investors between managers and investors

ELIGIBILITY OF TENDERERSELIGIBILITY OF TENDERERS

• Management companies interested in creating a private equity fund or a private Management companies interested in creating a private equity fund or a private equity fund of fundequity fund of fund

PRESENTATION OF THE PROPOSALPRESENTATION OF THE PROPOSAL

• Detailed Information concerning the fund: Management company; FUND type, Detailed Information concerning the fund: Management company; FUND type, Size designed for the FUND; FUND term;Size designed for the FUND; FUND term; Details of the structure of the Details of the structure of the FUND management fee and carried interest; Details of the team/staff retention FUND management fee and carried interest; Details of the team/staff retention policy; Exit strategies; Other investors fundraising, including investor profile, policy; Exit strategies; Other investors fundraising, including investor profile, stage of negotiations and possible compromises; FUND Investment Strategy; stage of negotiations and possible compromises; FUND Investment Strategy; FUND Internal Rate of Return; FUND governance; pipeline; among others.FUND Internal Rate of Return; FUND governance; pipeline; among others.

INOVAR PROJECT – EVALUATION PROCESSINOVAR PROJECT – EVALUATION PROCESS

EVALUATION PROCESS:EVALUATION PROCESS:

• Pre-qualification – Phase 1Pre-qualification – Phase 1

• Appeals to the pre-qualification – Phase 2Appeals to the pre-qualification – Phase 2

• Evaluation Panel – Phase 3Evaluation Panel – Phase 3

• Result of the Evaluation PanelResult of the Evaluation Panel

• The proposals will be allocated in three (3) groups:The proposals will be allocated in three (3) groups:

‒ Group 1 – Group 1 – due diligencedue diligence;;

‒ Group 2 – conditioned Group 2 – conditioned due diligencedue diligence; and; and

‒ Group 3 – non implementation of Group 3 – non implementation of due diligencedue diligence..

• The Group 2 is composed by Proposals which questions and/or requirements The Group 2 is composed by Proposals which questions and/or requirements made by any of the Evaluation Panel members should be solved as precedent made by any of the Evaluation Panel members should be solved as precedent condition to start the condition to start the due diligencedue diligence process. process.

• After the After the due diligence due diligence process, the interested investors will continue individually process, the interested investors will continue individually the analysis process in a more detailed way and further approval by its own the analysis process in a more detailed way and further approval by its own decision-board institutions.decision-board institutions.

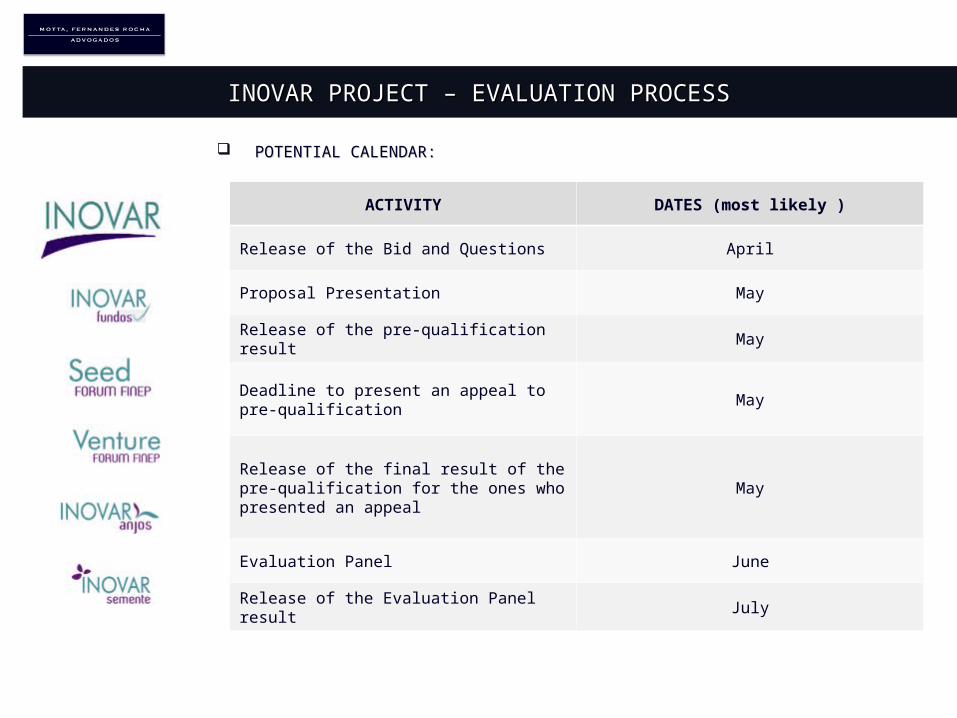

INOVAR PROJECT – EVALUATION PROCESSINOVAR PROJECT – EVALUATION PROCESS

POTENTIAL CALENDAR:POTENTIAL CALENDAR:

ACTIVITY DATES (most likely )

Release of the Bid and Questions April

Proposal Presentation May

Release of the pre-qualification result May

Deadline to present an appeal to pre-qualification

May

Release of the final result of the pre-qualification for the ones who presented an appeal

May

Evaluation Panel June

Release of the Evaluation Panel result July

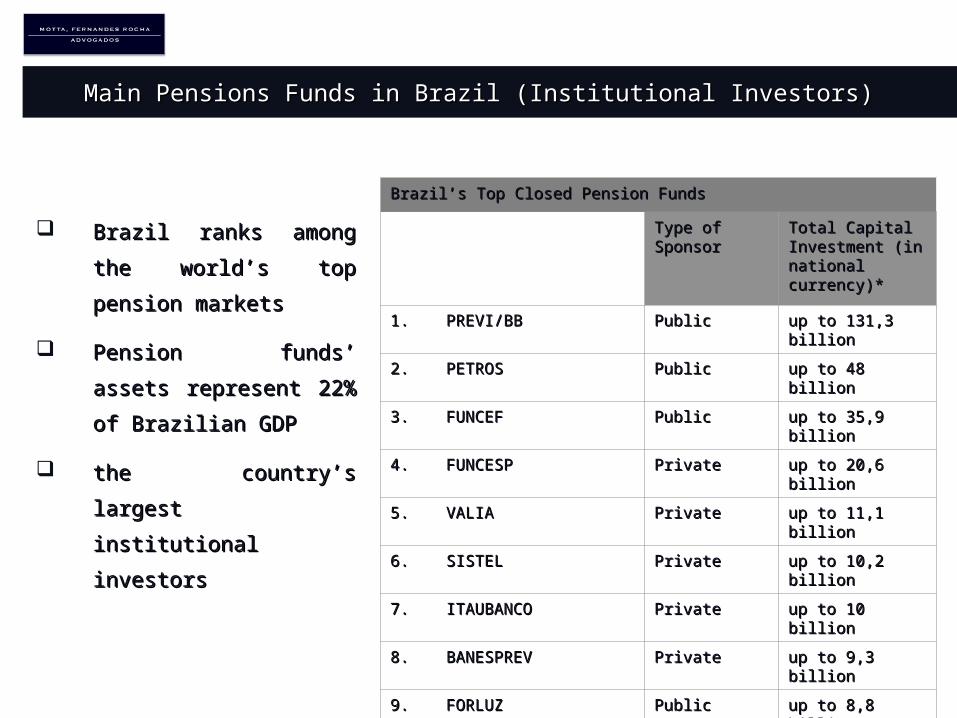

Main Pensions Funds in Brazil (Institutional Investors)Main Pensions Funds in Brazil (Institutional Investors)

Brazil ranks among the Brazil ranks among the

world’s top pension world’s top pension

marketsmarkets

Pension funds’ assets Pension funds’ assets

represent 22% of represent 22% of

Brazilian GDPBrazilian GDP

the country’s largest the country’s largest

institutional investors institutional investors

Brazil’s Top Closed Pension FundsBrazil’s Top Closed Pension Funds

Type of Type of SponsorSponsor

Total Capital Total Capital Investment (in Investment (in national national currency)*currency)*

1.1. PREVI/BBPREVI/BB PublicPublic up to 131,3 up to 131,3 billionbillion

2.2. PETROSPETROS PublicPublic up to 48 billionup to 48 billion

3.3. FUNCEFFUNCEF PublicPublic up to 35,9 billionup to 35,9 billion

4.4. FUNCESPFUNCESP PrivatePrivate up to 20,6 billionup to 20,6 billion

5.5. VALIAVALIA PrivatePrivate up to 11,1 billionup to 11,1 billion

6.6. SISTELSISTEL PrivatePrivate up to 10,2 billionup to 10,2 billion

7.7. ITAUBANCOITAUBANCO PrivatePrivate up to 10 billionup to 10 billion

8.8. BANESPREVBANESPREV PrivatePrivate up to 9,3 billionup to 9,3 billion

9.9. FORLUZFORLUZ PublicPublic up to 8,8 billionup to 8,8 billion

10.10. CENTRUSCENTRUS PublicPublic up to 8,2 billionup to 8,2 billion

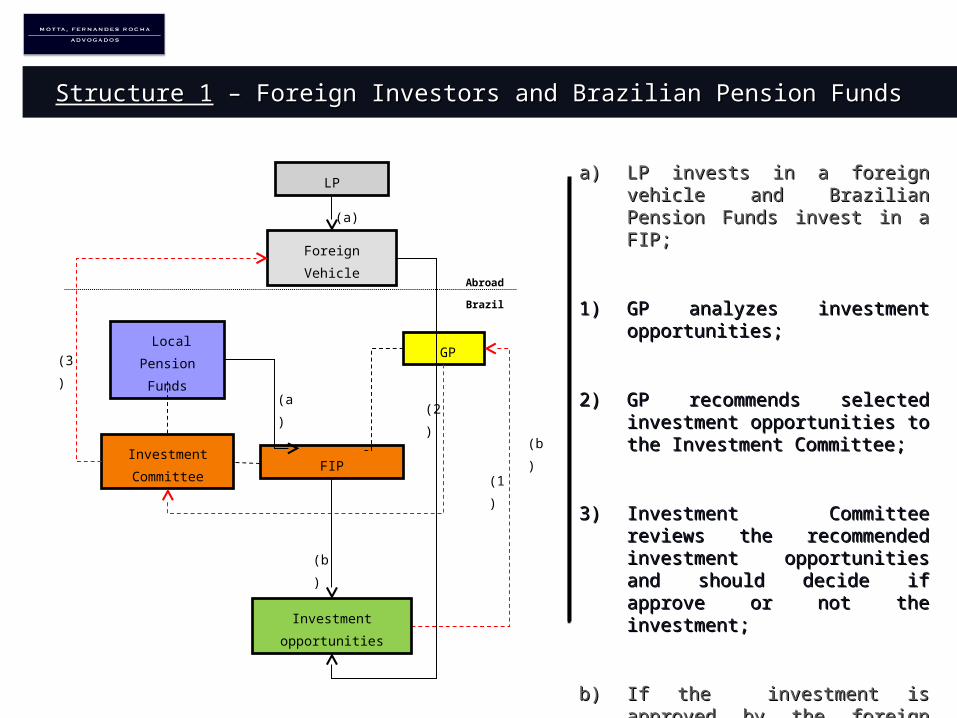

Structure 1Structure 1 – Foreign Investors and Brazilian Pension Funds – Foreign Investors and Brazilian Pension Funds

FIP

Foreign Vehicle

GP

(a)

(1)

a)a) LP invests in a foreign vehicle LP invests in a foreign vehicle and Brazilian Pension Funds and Brazilian Pension Funds invest in a FIP;invest in a FIP;

1)1) GP analyzes investment GP analyzes investment opportunities;opportunities;

2)2) GP recommends selected GP recommends selected investment opportunities to the investment opportunities to the Investment Committee;Investment Committee;

3)3) Investment Committee reviews Investment Committee reviews the recommended investment the recommended investment opportunities and should decide opportunities and should decide if approve or not the if approve or not the investment; investment;

b)b) If the investment is approved If the investment is approved by the foreign vehicle, FIP and by the foreign vehicle, FIP and the foreign vehicle invest in the the foreign vehicle invest in the target company.target company.

(a)

Investment opportunities

LP

Local Pension

Funds

Investment

Committee

(2)

Abroad

Brazil

(b)

(3)

(b)

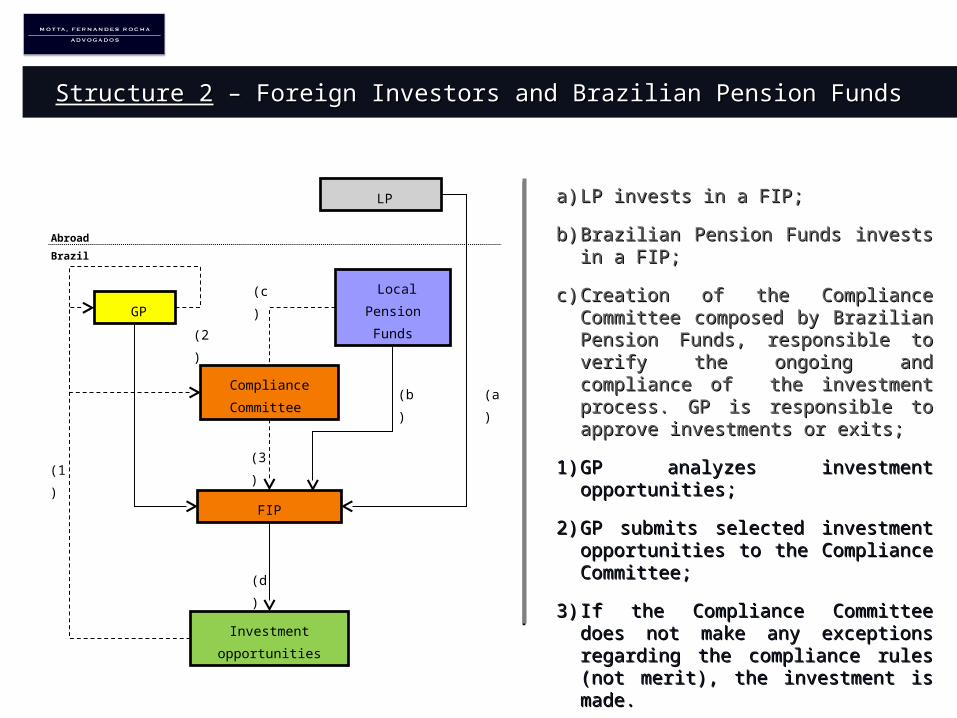

Structure 2Structure 2 – Foreign Investors and Brazilian Pension Funds – Foreign Investors and Brazilian Pension Funds

FIP

GP

(a)

(1)

a)a) LP invests in a FIP;LP invests in a FIP;

b)b) Brazilian Pension Funds invests in a Brazilian Pension Funds invests in a FIP;FIP;

c)c) Creation of the Compliance Creation of the Compliance Committee composed by Brazilian Committee composed by Brazilian Pension Funds, responsible to verify Pension Funds, responsible to verify the ongoing and compliance of the the ongoing and compliance of the investment process. GP is investment process. GP is responsible to approve investments responsible to approve investments or exits;or exits;

1)1) GP analyzes investment GP analyzes investment opportunities;opportunities;

2)2) GP submits selected investment GP submits selected investment opportunities to the Compliance opportunities to the Compliance Committee;Committee;

3)3) If the Compliance Committee does If the Compliance Committee does not make any exceptions regarding not make any exceptions regarding the compliance rules (not merit), the the compliance rules (not merit), the investment is made. investment is made.

d)d) FIP invests in the target company.FIP invests in the target company.

Investment opportunities

LP

(3)

Abroad

Brazil

Compliance

Committee

Local Pension

Funds

(b)

(2)

(c)

(d)

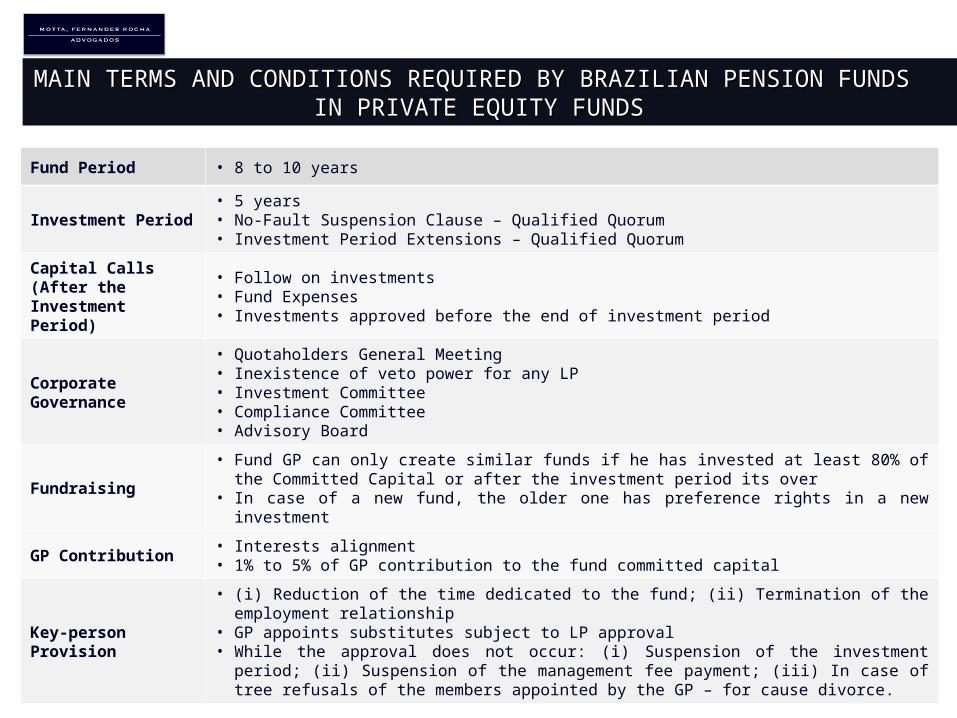

MAIN TERMS AND CONDITIONS REQUIRED BY BRAZILIAN PENSION FUNDS MAIN TERMS AND CONDITIONS REQUIRED BY BRAZILIAN PENSION FUNDS IN PRIVATE EQUITY FUNDSIN PRIVATE EQUITY FUNDS

Fund Period • 8 to 10 years

Investment Period• 5 years• No-Fault Suspension Clause – Qualified Quorum• Investment Period Extensions – Qualified Quorum

Capital Calls (After the Investment Period)

• Follow on investments• Fund Expenses• Investments approved before the end of investment period

Corporate Governance

• Quotaholders General Meeting• Inexistence of veto power for any LP• Investment Committee• Compliance Committee• Advisory Board

Fundraising• Fund GP can only create similar funds if he has invested at least 80% of the

Committed Capital or after the investment period its over• In case of a new fund, the older one has preference rights in a new investment

GP Contribution• Interests alignment • 1% to 5% of GP contribution to the fund committed capital

Key-person Provision

• (i) Reduction of the time dedicated to the fund; (ii) Termination of the employment relationship

• GP appoints substitutes subject to LP approval• While the approval does not occur: (i) Suspension of the investment period; (ii)

Suspension of the management fee payment; (iii) In case of tree refusals of the members appointed by the GP – for cause divorce.

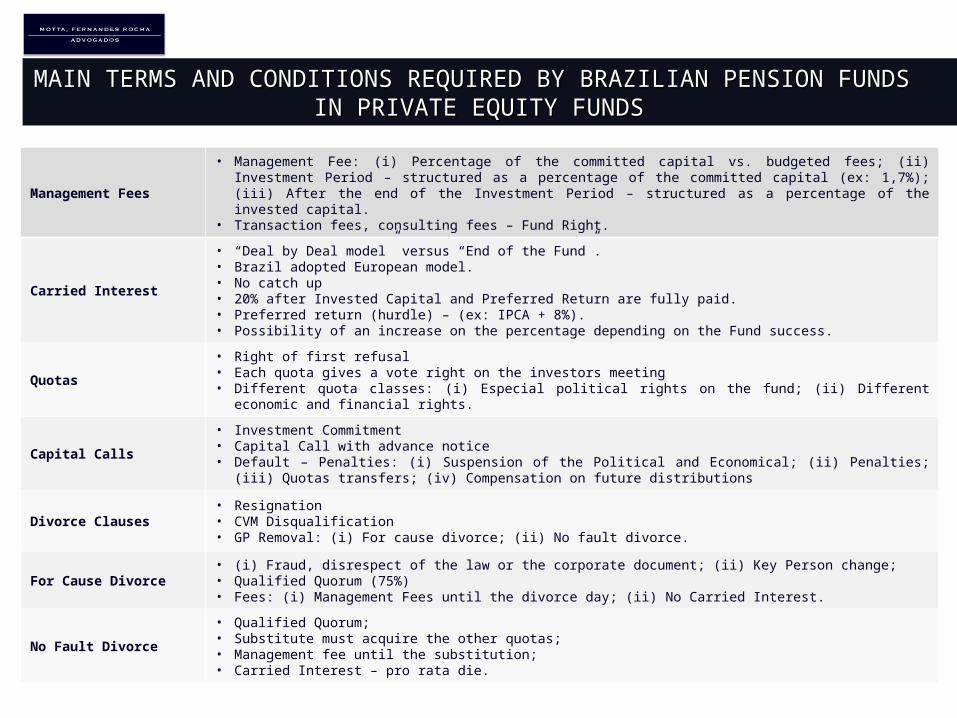

Management Fees

• Management Fee: (i) Percentage of the committed capital vs. budgeted fees; (ii) Investment Period – structured as a percentage of the committed capital (ex: 1,7%); (iii) After the end of the Investment Period – structured as a percentage of the invested capital.

• Transaction fees, consulting fees – Fund Right.

Carried Interest

• “Deal by Deal model” versus “End of the Fund”.• Brazil adopted European model.• No catch up• 20% after Invested Capital and Preferred Return are fully paid.• Preferred return (hurdle) – (ex: IPCA + 8%).• Possibility of an increase on the percentage depending on the Fund success.

Quotas

• Right of first refusal• Each quota gives a vote right on the investors meeting• Different quota classes: (i) Especial political rights on the fund; (ii) Different economic and financial

rights.

Capital Calls

• Investment Commitment• Capital Call with advance notice• Default – Penalties: (i) Suspension of the Political and Economical; (ii) Penalties; (iii) Quotas transfers;

(iv) Compensation on future distributions

Divorce Clauses• Resignation• CVM Disqualification• GP Removal: (i) For cause divorce; (ii) No fault divorce.

For Cause Divorce• (i) Fraud, disrespect of the law or the corporate document; (ii) Key Person change; • Qualified Quorum (75%)• Fees: (i) Management Fees until the divorce day; (ii) No Carried Interest.

No Fault Divorce

• Qualified Quorum; • Substitute must acquire the other quotas;• Management fee until the substitution; • Carried Interest – pro rata die.

MAIN TERMS AND CONDITIONS REQUIRED BY BRAZILIAN PENSION FUNDS MAIN TERMS AND CONDITIONS REQUIRED BY BRAZILIAN PENSION FUNDS IN PRIVATE EQUITY FUNDSIN PRIVATE EQUITY FUNDS

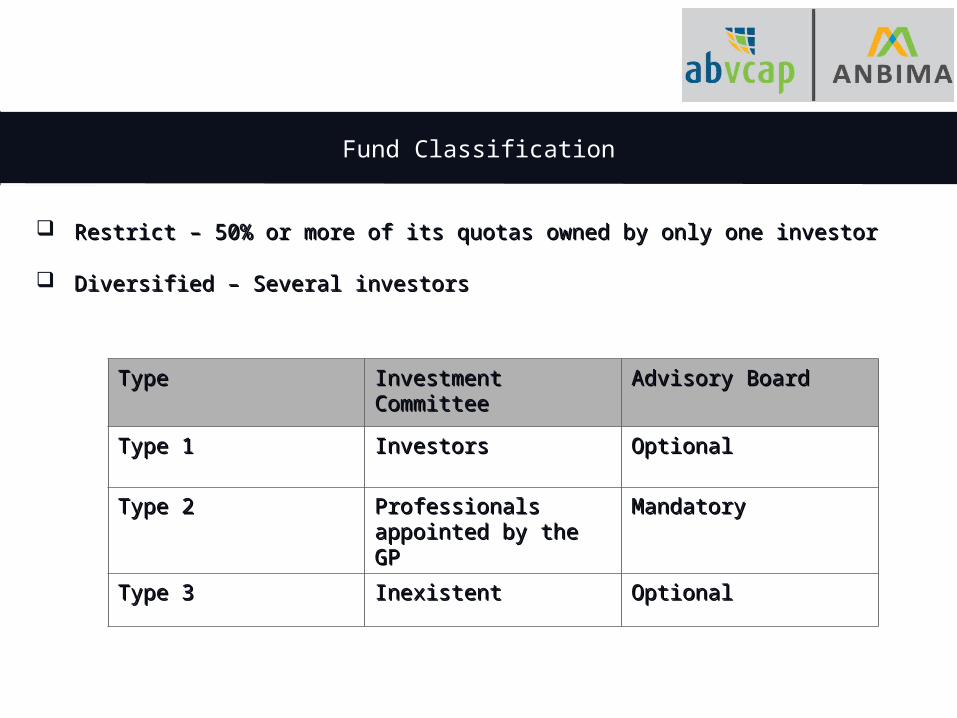

Fund Classification

Restrict – 50% or more of its quotas owned by only one investorRestrict – 50% or more of its quotas owned by only one investor

Diversified – Several investorsDiversified – Several investors

Type Type Investment Investment CommitteeCommittee

Advisory BoardAdvisory Board

Type 1Type 1 InvestorsInvestors Optional Optional

Type 2Type 2 Professionals Professionals appointed by the GPappointed by the GP

Mandatory Mandatory

Type 3Type 3 Inexistent Inexistent Optional Optional

WHY MOTTA, FERNANDES ROCHA ADVOGADOS?WHY MOTTA, FERNANDES ROCHA ADVOGADOS?

Founded in 1956, Motta, Fernandes Rocha Advogados - MFRA was one of Founded in 1956, Motta, Fernandes Rocha Advogados - MFRA was one of the the first law firms to create a private equity groupfirst law firms to create a private equity group, providing a , providing a combination of deep local knowledge and international experience in combination of deep local knowledge and international experience in the Brazilian and Latin American markets. the Brazilian and Latin American markets.

Luiz Leonardo CantidianoLuiz Leonardo Cantidiano, MFRA’s founding partner and former , MFRA’s founding partner and former president of the CVM (Brazilian Securities and Exchange Commission), president of the CVM (Brazilian Securities and Exchange Commission), signed the CVM’s Rule that signed the CVM’s Rule that created the Private Equity Fund (“FIP”) created the Private Equity Fund (“FIP”) and FIC-FIP in Braziland FIC-FIP in Brazil..

Knowledge of the Terms and Conditions Knowledge of the Terms and Conditions required by Brazilians required by Brazilians pension funds to invest in a private equity fund.pension funds to invest in a private equity fund.

Responsible for a leading project to structure a private equity Responsible for a leading project to structure a private equity fund of funds as a Fundo de fund of funds as a Fundo de Investimento em Cotas de Fundos Investimento em Cotas de Fundos de Investimento em Participações (FIC-FIP) de Investimento em Participações (FIC-FIP) to an international to an international player and participation at Inovar Project. Active participation in player and participation at Inovar Project. Active participation in the discussion with Brazilian pension funds to invest in a FIC-the discussion with Brazilian pension funds to invest in a FIC-FIP.FIP.

Close relationship with Pension funds Close relationship with Pension funds and institutional investors.and institutional investors.

Relevant experience in bid projects Relevant experience in bid projects as Projeto Inovar.as Projeto Inovar.

Active Active member of ABVCAP member of ABVCAP (Brazilian Association of Private Equity & (Brazilian Association of Private Equity & Venture Capital).Venture Capital).

Overview of MFRA’s Recent Private Equity Experience

The The group manages and group manages and has advised on a combined has advised on a combined total of over USD 21 billion total of over USD 21 billion in private equity and real in private equity and real estate funds over the estate funds over the world.world.

BR Educacional BR Educacional –– Private Private Equity Fund focused on the Equity Fund focused on the education sector (R$ 400 education sector (R$ 400 million).million).

FIP Terra Viva FIP Terra Viva –– Private Private Equity Fund focused on the Equity Fund focused on the sugar cane and ethanol sugar cane and ethanol sector (R$ 350 million).sector (R$ 350 million).

Advice LogAdvice Logíística Brasil stica Brasil –– Private Equity Fund Private Equity Fund focused on the focused on the transportation and logistics transportation and logistics sector (R$ 400 million).sector (R$ 400 million).

GG Investimentos – GG Investimentos – Brazilian Private Equity Brazilian Private Equity Fund.Fund.

US$ 130 million US$ 130 million investment by Fundos investment by Fundos GGáávea in Cosan Limited.vea in Cosan Limited.

FIP NSG Brazil Metal FIP NSG Brazil Metal –– Private Equity Fund (R$ Private Equity Fund (R$ 600 million). Acquisition of 600 million). Acquisition of Zamprogna.Zamprogna.

Brazilian Fund focused on Brazilian Fund focused on IT market.IT market.

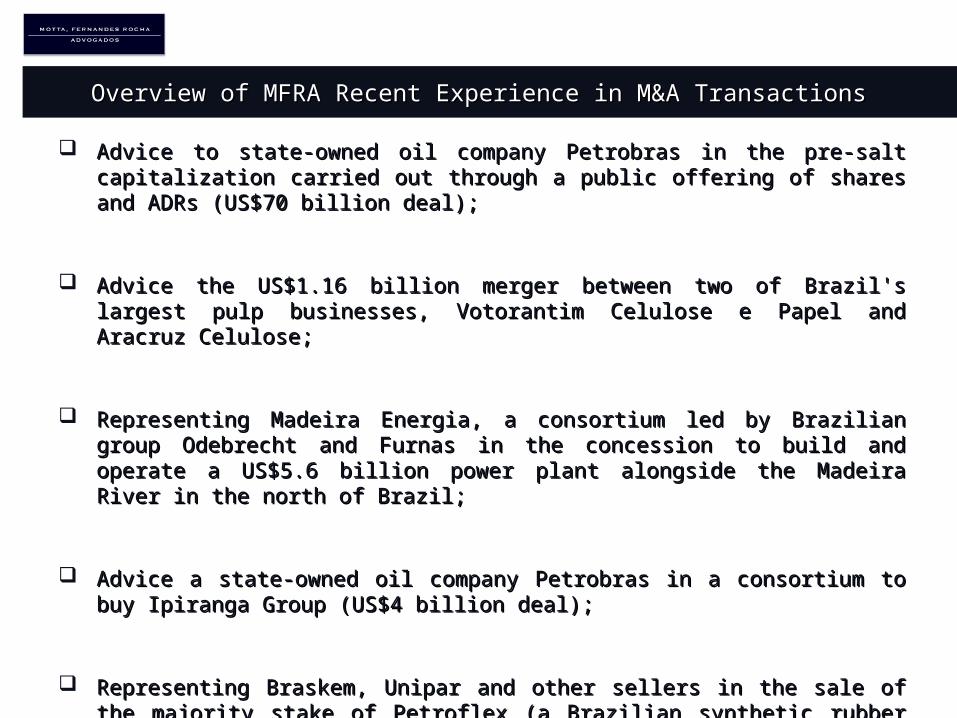

Overview of MFRA Recent Experience in M&A TransactionsOverview of MFRA Recent Experience in M&A Transactions

Advice to state-owned oil company Petrobras in the pre-salt capitalization Advice to state-owned oil company Petrobras in the pre-salt capitalization carried out through a public offering of shares and ADRs (US$70 billion carried out through a public offering of shares and ADRs (US$70 billion deal);deal);

Advice the US$1.16 billion merger between two of Brazil's largest pulp Advice the US$1.16 billion merger between two of Brazil's largest pulp businesses, Votorantim Celulose e Papel and Aracruz Celulose;businesses, Votorantim Celulose e Papel and Aracruz Celulose;

Representing Madeira Energia, a consortium led by Brazilian group Representing Madeira Energia, a consortium led by Brazilian group Odebrecht and Furnas in the concession to build and operate a US$5.6 Odebrecht and Furnas in the concession to build and operate a US$5.6 billion power plant alongside the Madeira River in the north of Brazil;billion power plant alongside the Madeira River in the north of Brazil;

Advice a state-owned oil company Petrobras in a consortium to buy Advice a state-owned oil company Petrobras in a consortium to buy Ipiranga Group (US$4 billion deal);Ipiranga Group (US$4 billion deal);

Representing Braskem, Unipar and other sellers in the sale of the majority Representing Braskem, Unipar and other sellers in the sale of the majority stake of Petroflex (a Brazilian synthetic rubber producer) to a German stake of Petroflex (a Brazilian synthetic rubber producer) to a German Chemical company Lanxess in the amount of R$526,680.000.00;Chemical company Lanxess in the amount of R$526,680.000.00;

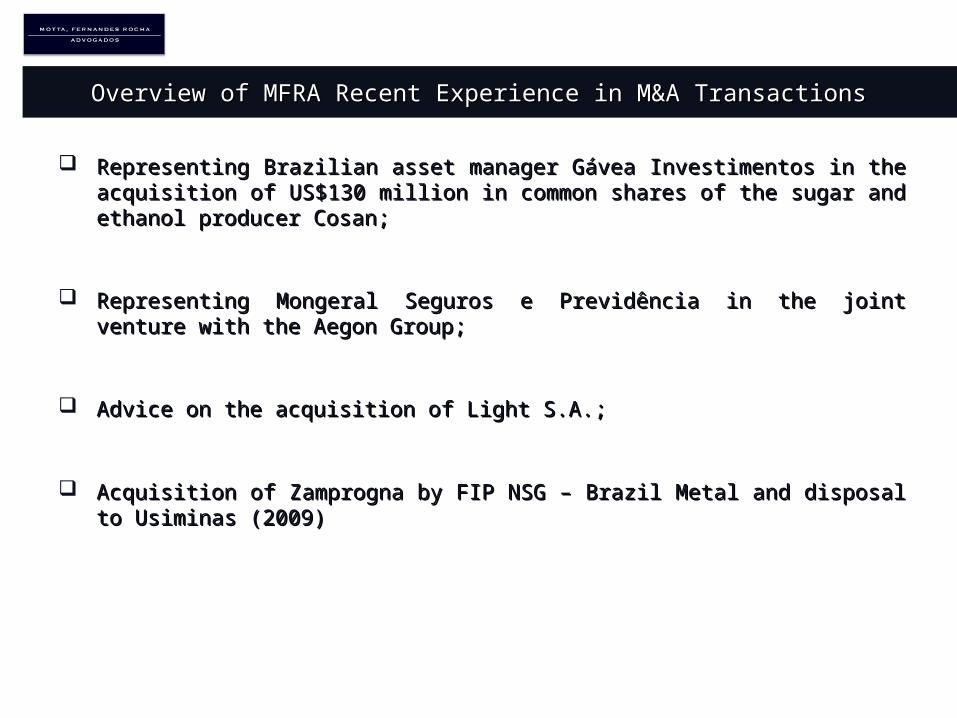

Overview of MFRA Recent Experience in M&A TransactionsOverview of MFRA Recent Experience in M&A Transactions

Representing Brazilian asset manager Gávea Investimentos in the Representing Brazilian asset manager Gávea Investimentos in the acquisition of US$130 million in common shares of the sugar and ethanol acquisition of US$130 million in common shares of the sugar and ethanol producer Cosan;producer Cosan;

Representing Mongeral Seguros e Previdência in the joint venture with the Representing Mongeral Seguros e Previdência in the joint venture with the Aegon Group;Aegon Group;

Advice on the acquisition of Light S.A.;Advice on the acquisition of Light S.A.;

Acquisition of Zamprogna by FIP NSG – Brazil Metal and disposal to Acquisition of Zamprogna by FIP NSG – Brazil Metal and disposal to Usiminas (2009)Usiminas (2009)

Copyright 2012 Motta, Fernandes Rocha Advogados. All rights reserved.

SÃO PAULOSÃO PAULO

Alameda Santos, 2335 – 10º , 11º e 12º Floor – Jardim Paulista

CEP 01419-002 São Paulo SP BrazilTel: +55 (11) 3082-9398 | +55 (11) 2192-9300Fax: +55 (11) 3082-3272 | [email protected]

Av. Brasil, 1.030 – Jardim AméricaCEP 01430-000 São Paulo SP BrazilTel: +55 (11) 3069-4300 | Fax: +55 (11) 3069-4301

RIO DE JANEIRORIO DE JANEIRO

Almirante Barroso, 52 – 5º Floor – Centro CEP 20031-000 Rio de Janeiro RJ BrazilTel: +55 (21) 2533-2200 | +55 (21) 3257-2200Fax: +55 (21) 2262-2459 | [email protected]

CONTACTCONTACT

DANIEL [email protected]