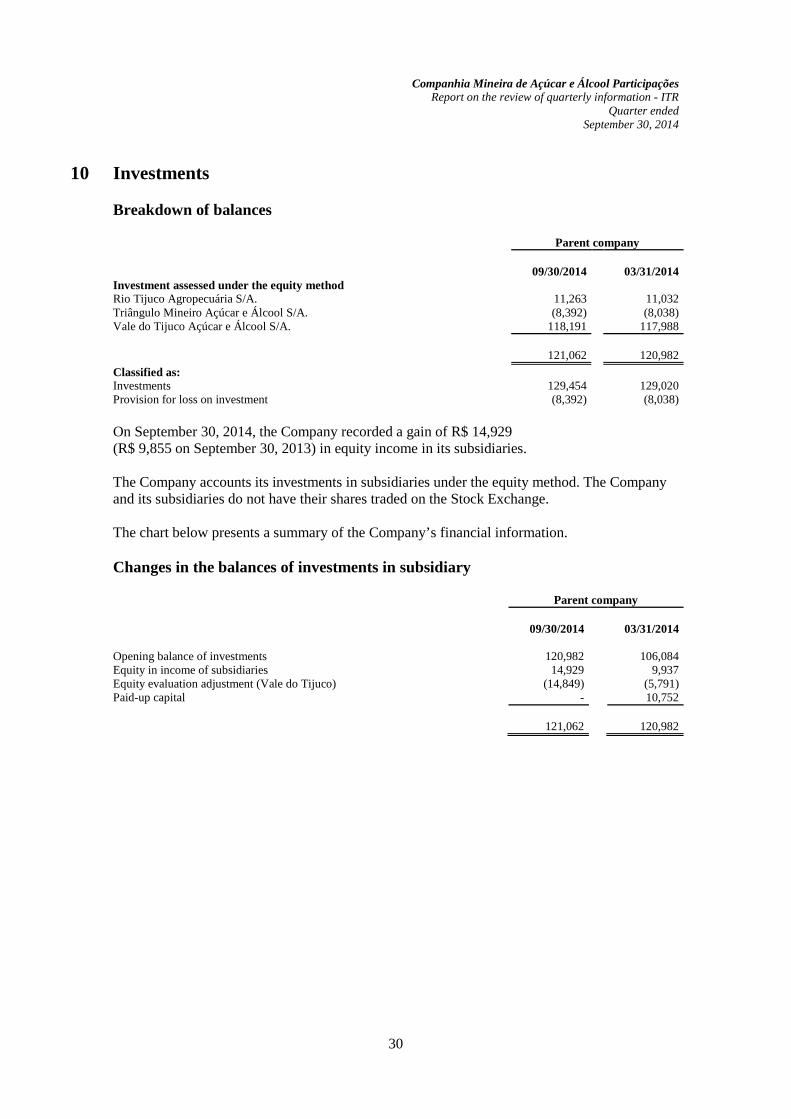

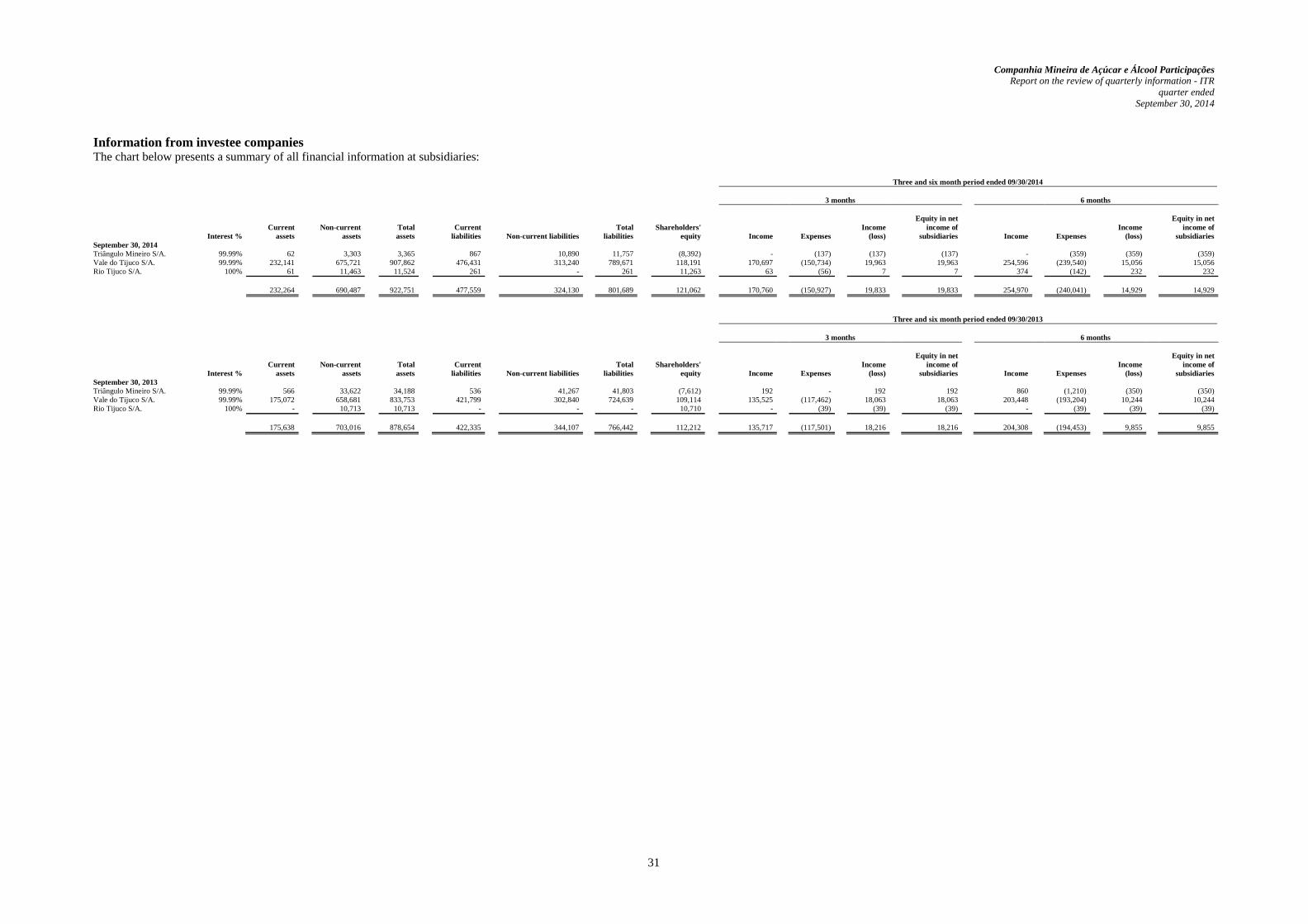

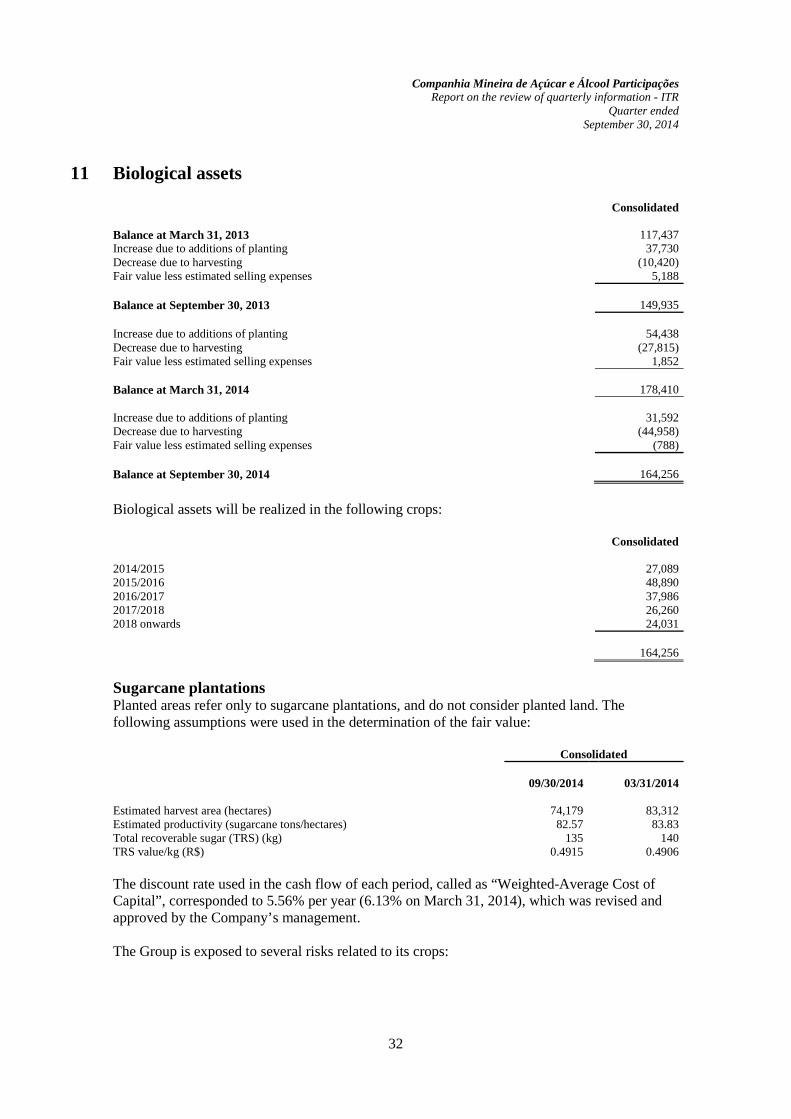

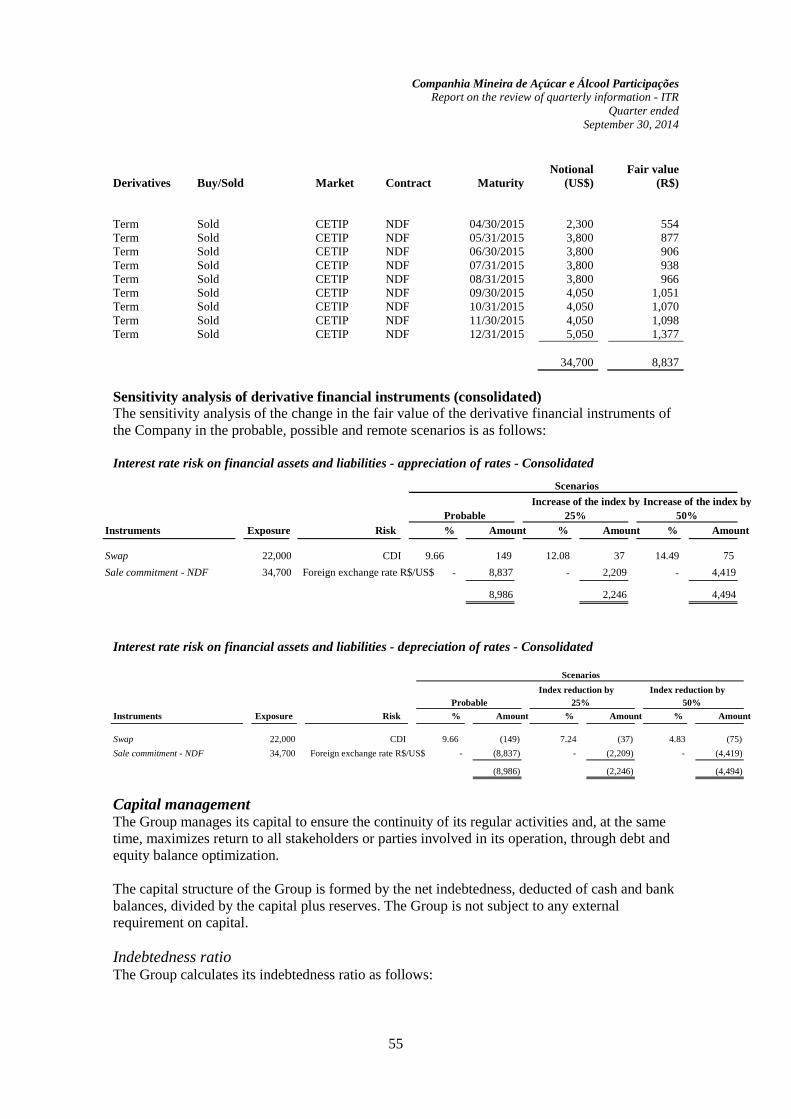

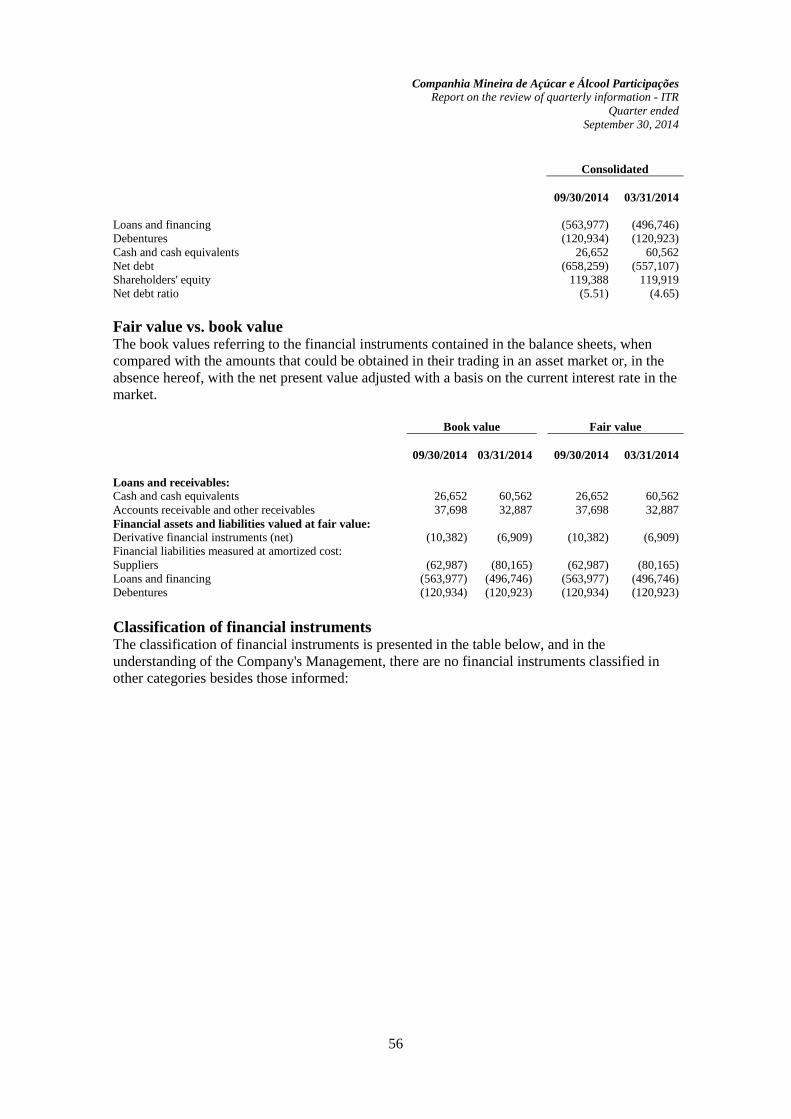

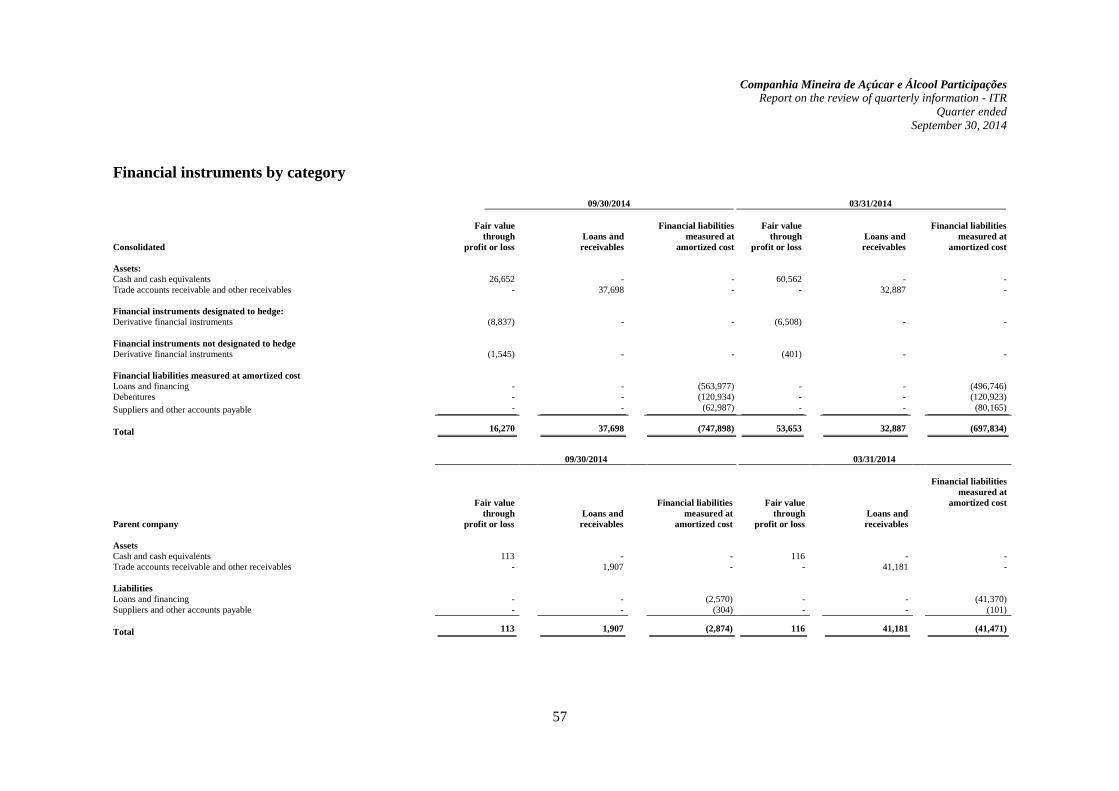

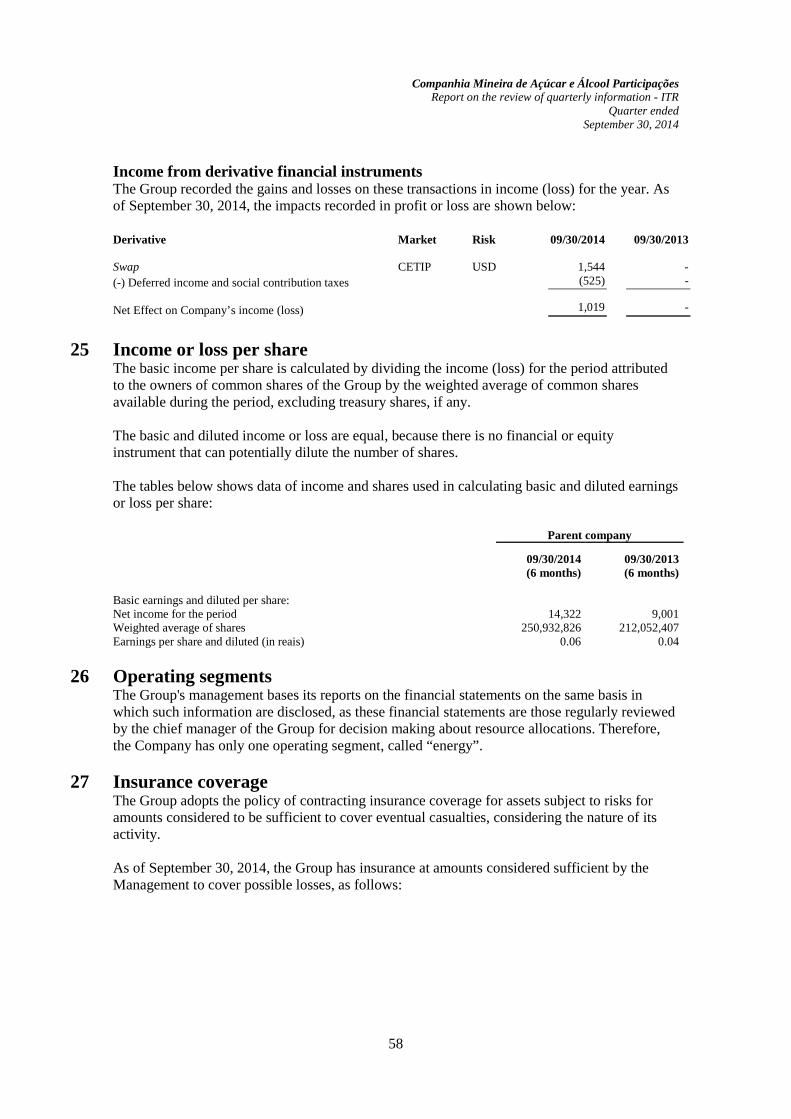

Embed Size (px)

Citation preview

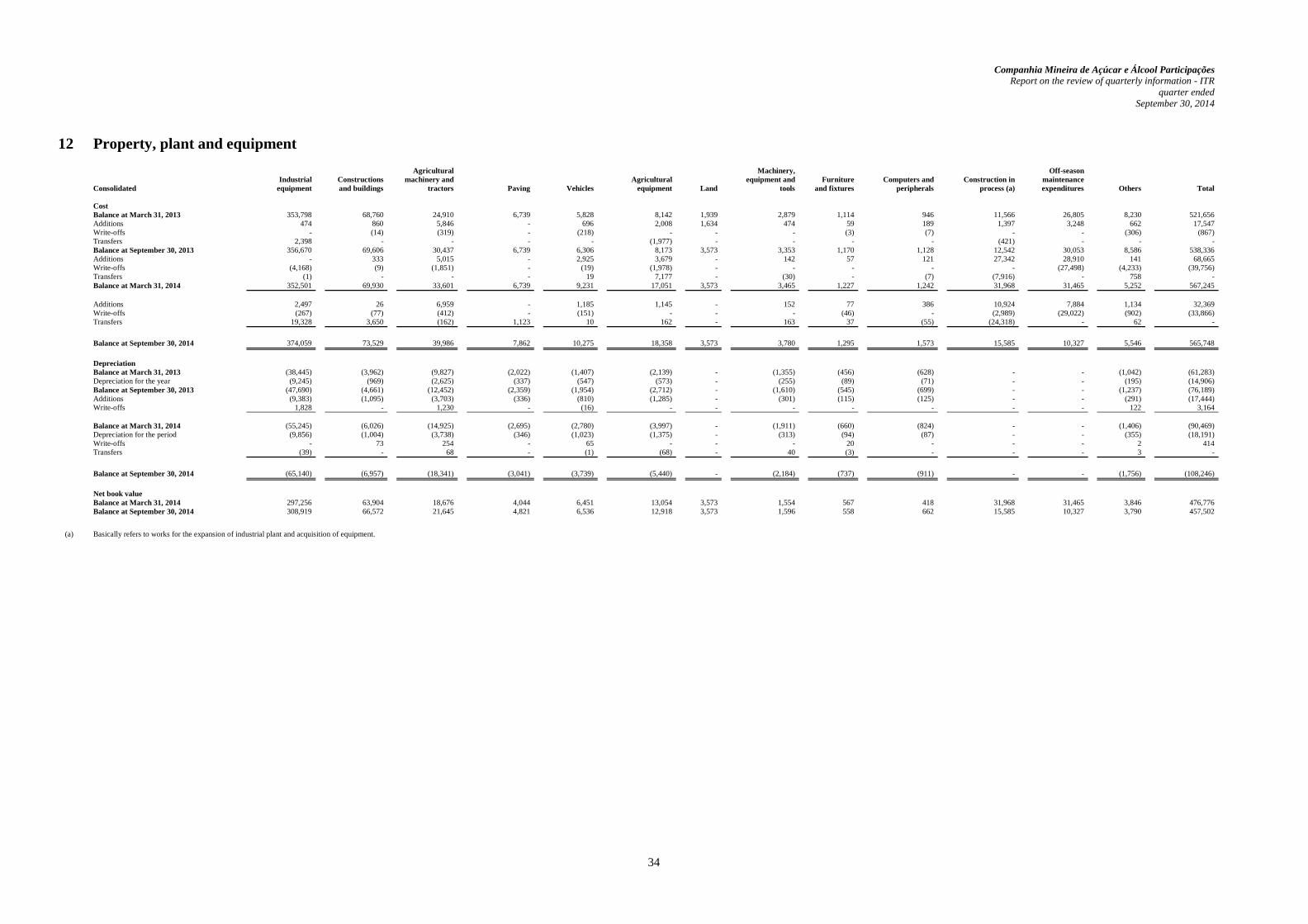

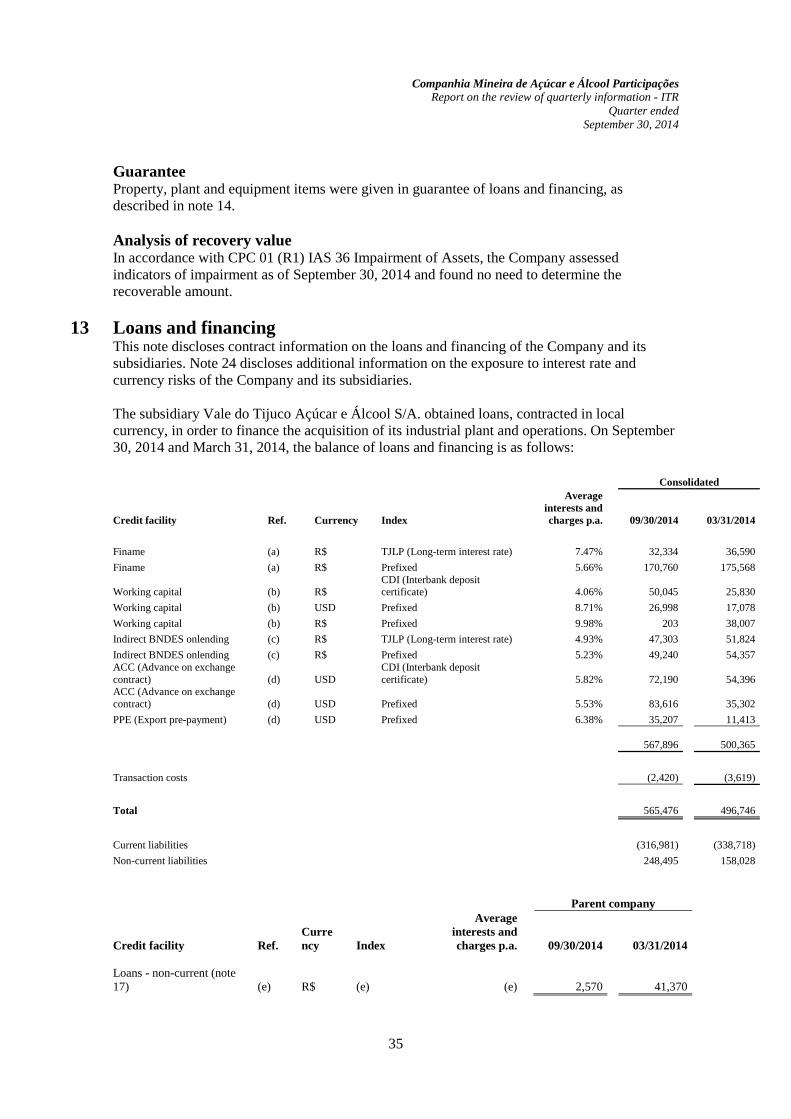

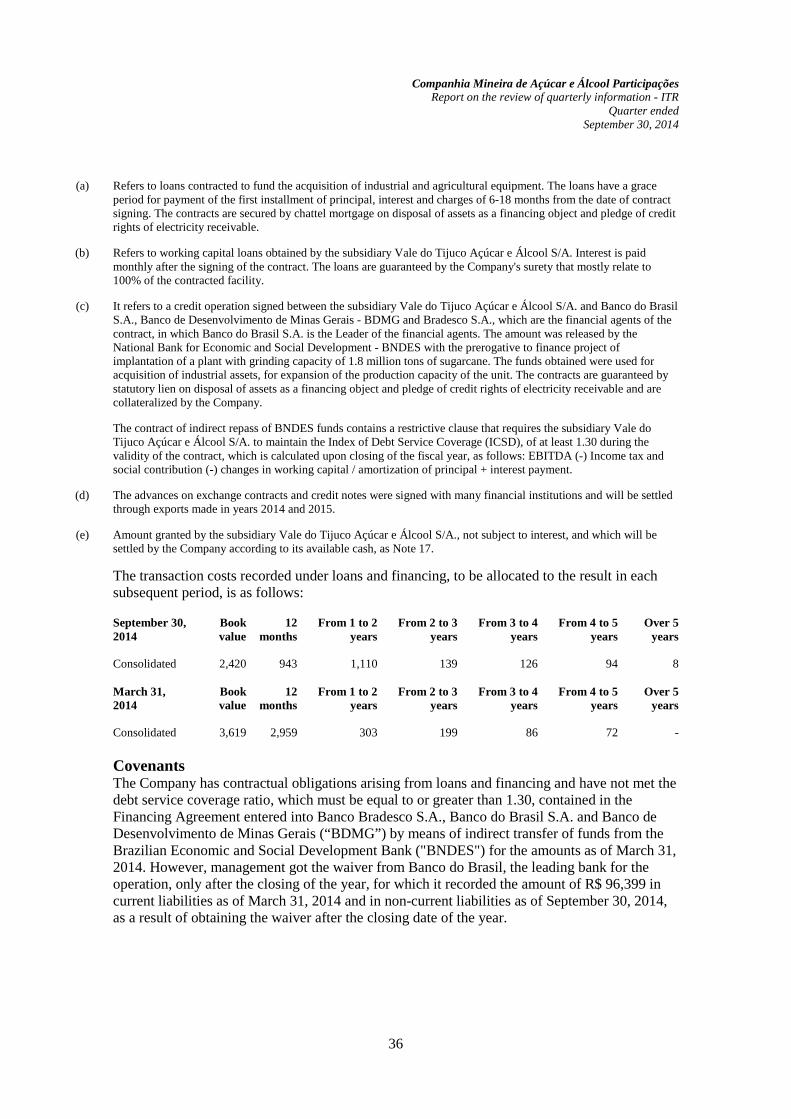

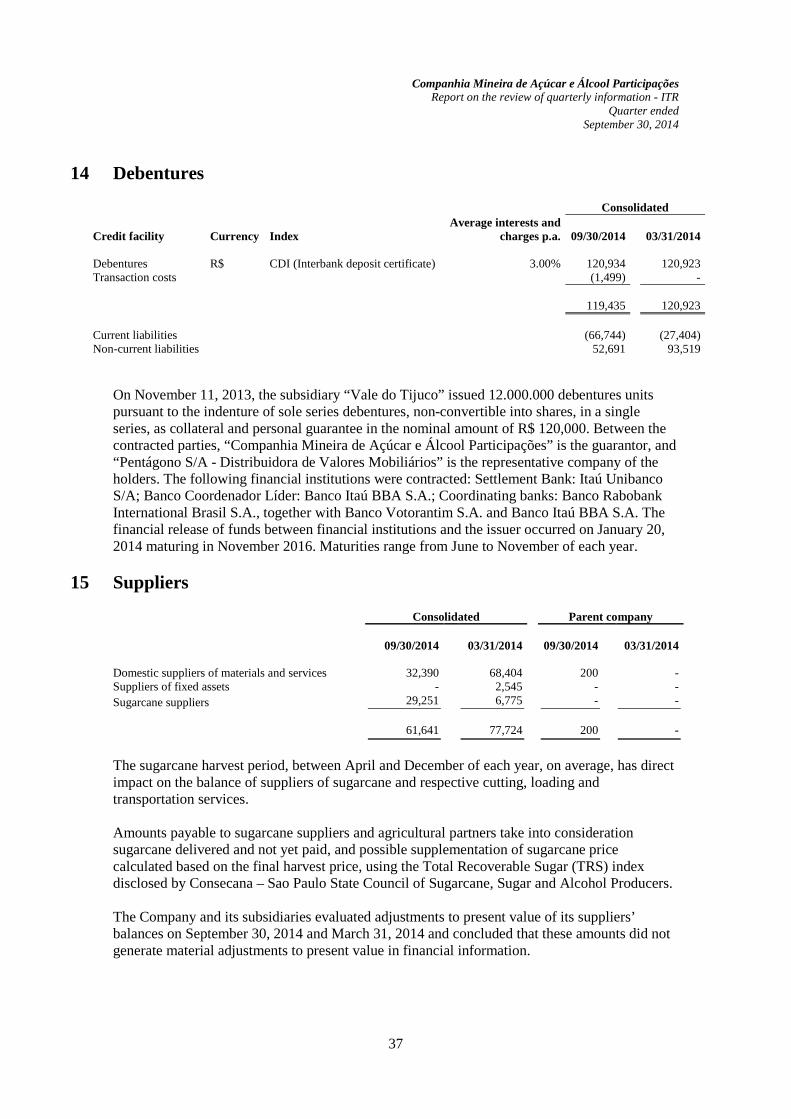

Companhia Mineira de Açúcar e Álcool Participações

Management Report - Harvest 14/15 – 2º Quarterly 2Q15

COMPANHIA MINEIRA DE AÇÚCAR E ÁLCOOL

PARTICIPAÇÕES HARVEST 14/15 – 2Q15

Management Report

Uberaba, November 14th 2014.

Dear Shareholders,

We present the Management Report, the Financial Statements and Independent Auditors' Report for

the first quarterly of harvest 2014/2015, ended on September 30th, 2014 in accordance with CPCs and IFRS..

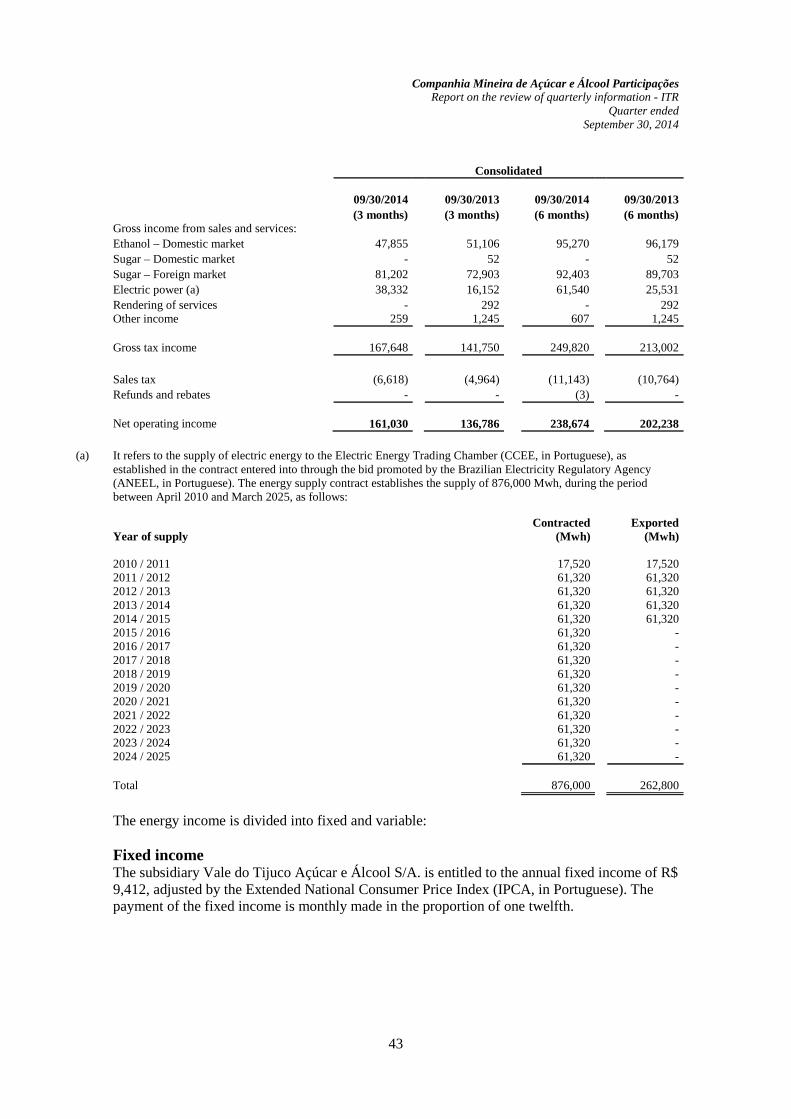

It was crushed 1,498 K Tons of sugarcane in 2Q15, increased 7.9% if compared with previous

crop. YTD of September was 2,781 k Tons, 18.5% higher than last harvest..

On second quarterly of current harvest were produced: 112 k Tons of sugar, 59 K m³ of

ethanol and 105 k MWH of energy. YTD up to September, the production of VHP was 17.2% higher than last

crop (170 ktons), +7.7% of ethanol (112 k m³) and +29% of energy (193k MWH).

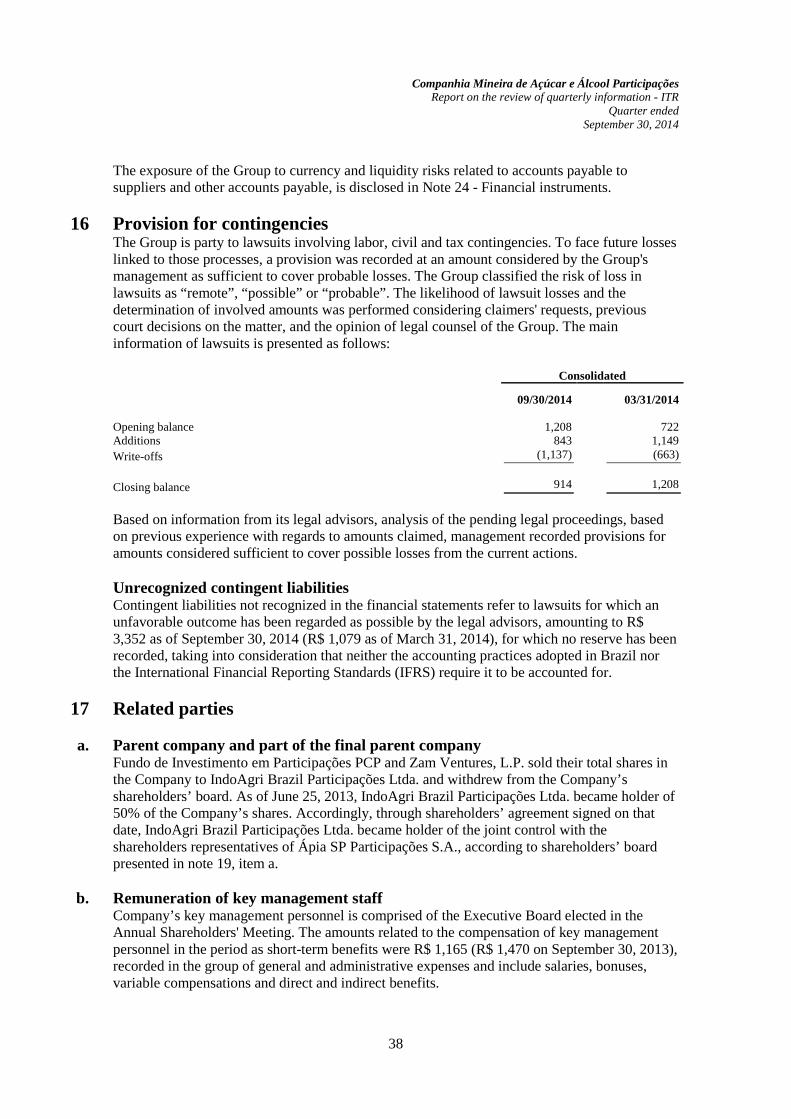

Gross Sales of 2Q15 was 166 MR$, +17% than 2Q14. On this first 6 months of current crop

was billed 249.8 MR$, 17.3% higher than last crop.

EBITDA was 48.7 MR$ in 2Q15, increased of 15.8%. YTD up to September was 82.4 MR$,

55.9% higher than last crop.

Increase of 10.7% at net income in 2Q15 (19.6 MR$). YTD this crop increased 59.1% if

compared same period than previous crop.

Features of Harvest 14/15 – 2Q15

COMPANHIA MINEIRA DE AÇÚCAR E ÁLCOOL

PARTICIPAÇÕES HARVEST 14/15 – 2Q15

Note: EBITDA: Net sales (-) COGS (-) SG&A (+)Depreciation and Plating amortization allocated in product cost. Ratoon cane treatment

is considered in cost, therefore don´t sum to compose EBITDA.

Operational & Financial Features

(THOUSAND REAIS) 2Q14 2Q15 Var.(%) 6M14 6M15 Var.(%)

CMAA - CONSOLIDATED

Gross Sales 141.750 165.914 17,0% 213.002 249.820 17,3%

Net Sales 136.786 161.030 17,7% 202.238 238.674 18,0%

COGS -88.513 -106.744 20,6% -145.045 -160.501 10,7%

SG&A -13.859 -17.184 24,0% -22.611 -27.176 20,2%

Depreciation and Planting Amortizantion 7.655 11.635 52,0% 18.291 31.445 71,9%

EBITDA 42.069 48.737 15,8% 52.873 82.442 55,9%

EBITDA Margin 30,8% 30,3% -1,6% 26,1% 34,5% 32,2%

Net Income 17.698 19.591 10,7% 9.001 14.322 59,1%

Operational Data 2Q14 2Q15 Var.(%) 6M14 6M15 Var.(%)

CMAA - CONSOLIDATED 2T14 2T15 Var.(%) 6M14 6M15 Var.(%)

Crushing Sugar Cane (Thousand Tons) 1.388 1.498 7,9% 2.347 2.781 18,5%

Owner 295 486 64,7% 781 1.042 33,4%

Third Parties 1.093 1.012 -7,4% 1.566 1.739 11,1%

Mechanized Harvesting 100% 100% 0,0% 100% 100% 0,0%

TRS (Kg/ton of cane) 142,3 139,7 -1,8% 133,4 127,6 -4,3%

Production

Sugar (Thousand Tons) 94 112 19,1% 145 170 17,2%

Anhydrous Ethanol (Thousand m³) 43 44 3,5% 60 77 27,0%

Hydrous Ethanol (Thousand m³) 22 15 -32,8% 44 35 -20,5%

Electric Energy (Thousand Mwh) 92 105 14,1% 150 193 29,0%

Sales

Sugar (Thousand Tons) 77 89 15,5% 97 100 2,9%

Anhydrous Ethanol (Thousand m³) 20 20 -1,7% 37 38 4,0%

Hydrous Ethanol (Thousand m³) 20 15 -26,6% 37 30 -19,7%

Electric Energy (Thousand Mwh) 92 103 12,0% 150 190 26,5%

Inventory

Sugar (Thousand Tons) 48 71 46,1% 48 71 46,1%

Anhydrous Ethanol (Thousand m³) 27 43 59,9% 26,6 42,6 59,9%

Hydrous Ethanol (Thousand m³) 7 4,8 -35,7% 7,4 4,8 -35,7%

COMPANHIA MINEIRA DE AÇÚCAR E ÁLCOOL

PARTICIPAÇÕES HARVEST 14/15 – 2Q15

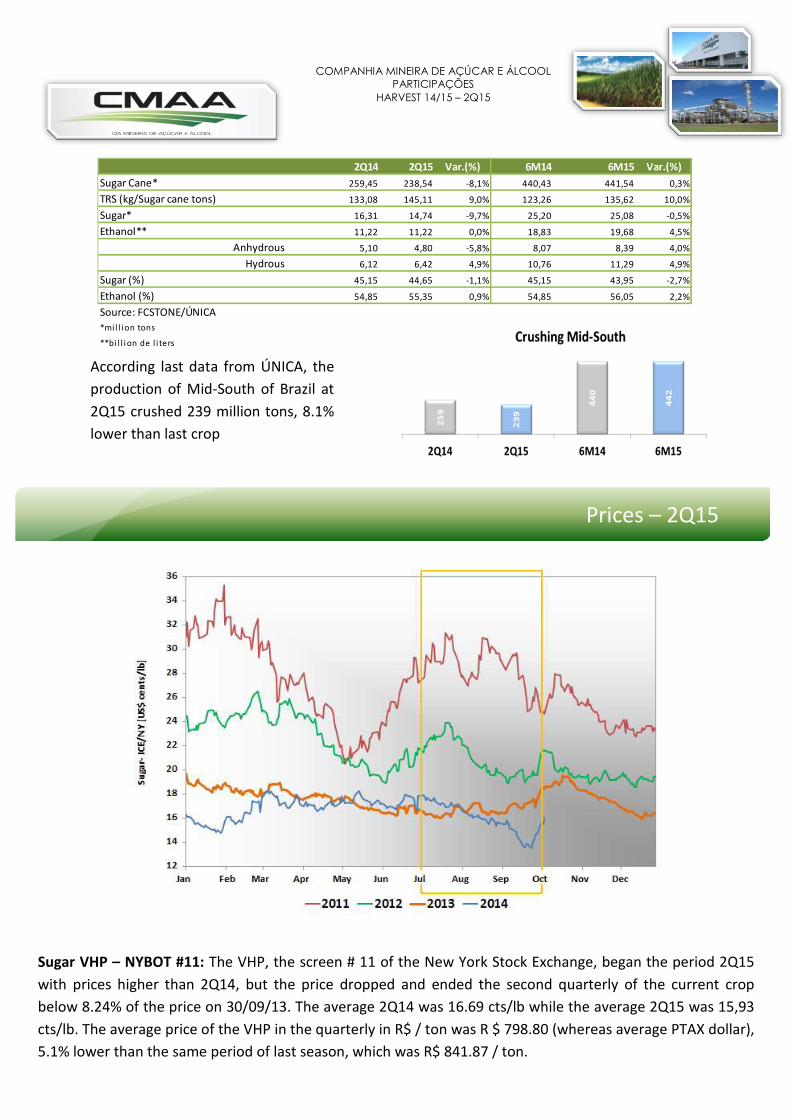

Sugar VHP – NYBOT #11: The VHP, the screen # 11 of the New York Stock Exchange, began the period 2Q15

with prices higher than 2Q14, but the price dropped and ended the second quarterly of the current crop

below 8.24% of the price on 30/09/13. The average 2Q14 was 16.69 cts/lb while the average 2Q15 was 15,93

cts/lb. The average price of the VHP in the quarterly in R$ / ton was R $ 798.80 (whereas average PTAX dollar),

5.1% lower than the same period of last season, which was R$ 841.87 / ton.

2Q14 2Q15 Var.(%) 6M14 6M15 Var.(%)

Sugar Cane* 259,45 238,54 -8,1% 440,43 441,54 0,3%

TRS (kg/Sugar cane tons) 133,08 145,11 9,0% 123,26 135,62 10,0%

Sugar* 16,31 14,74 -9,7% 25,20 25,08 -0,5%

Ethanol** 11,22 11,22 0,0% 18,83 19,68 4,5%

Anhydrous 5,10 4,80 -5,8% 8,07 8,39 4,0%

Hydrous 6,12 6,42 4,9% 10,76 11,29 4,9%

Sugar (%) 45,15 44,65 -1,1% 45,15 43,95 -2,7%

Ethanol (%) 54,85 55,35 0,9% 54,85 56,05 2,2%

Source: FCSTONE/ÚNICA

*mil l ion tons

**bi l l i on de l i ters

Prices – 2Q15

According last data from ÚNICA, the

production of Mid-South of Brazil at

2Q15 crushed 239 million tons, 8.1%

lower than last crop

COMPANHIA MINEIRA DE AÇÚCAR E ÁLCOOL

PARTICIPAÇÕES HARVEST 14/15 – 2Q15

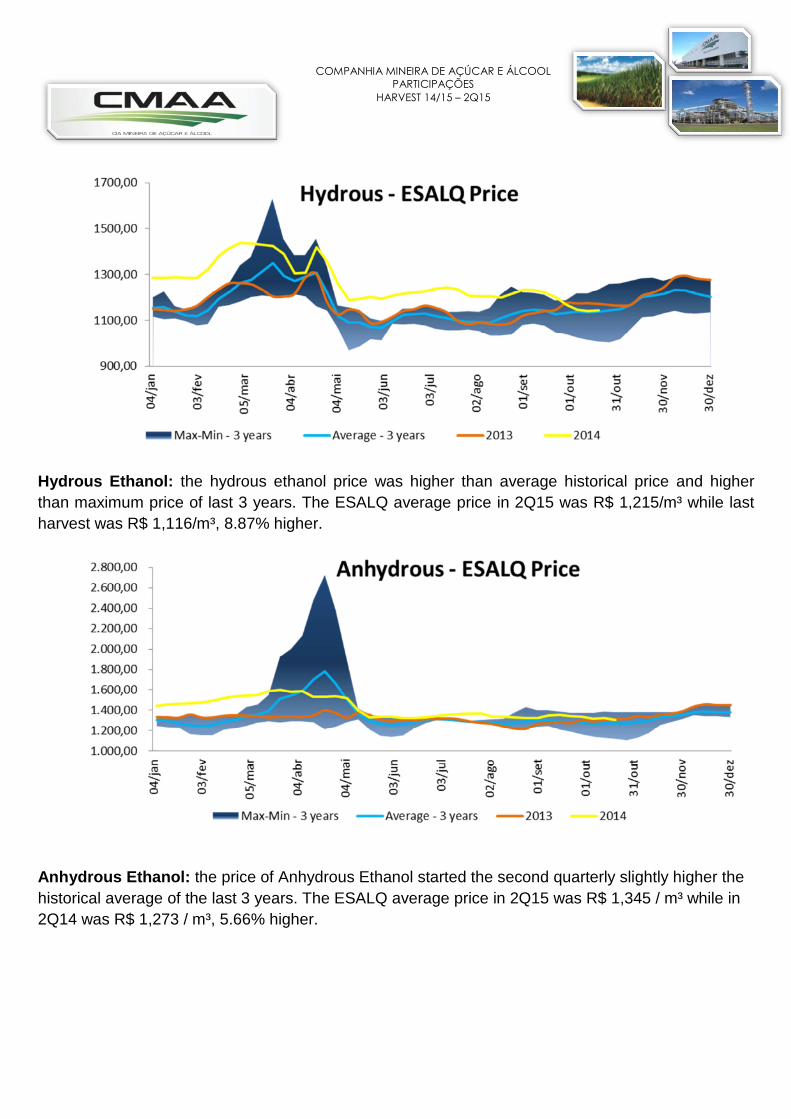

Hydrous Ethanol: the hydrous ethanol price was higher than average historical price and higher than maximum price of last 3 years. The ESALQ average price in 2Q15 was R$ 1,215/m³ while last harvest was R$ 1,116/m³, 8.87% higher.

Anhydrous Ethanol: the price of Anhydrous Ethanol started the second quarterly slightly higher the historical average of the last 3 years. The ESALQ average price in 2Q15 was R$ 1,345 / m³ while in 2Q14 was R$ 1,273 / m³, 5.66% higher.

COMPANHIA MINEIRA DE AÇÚCAR E ÁLCOOL

PARTICIPAÇÕES HARVEST 14/15 – 2Q15

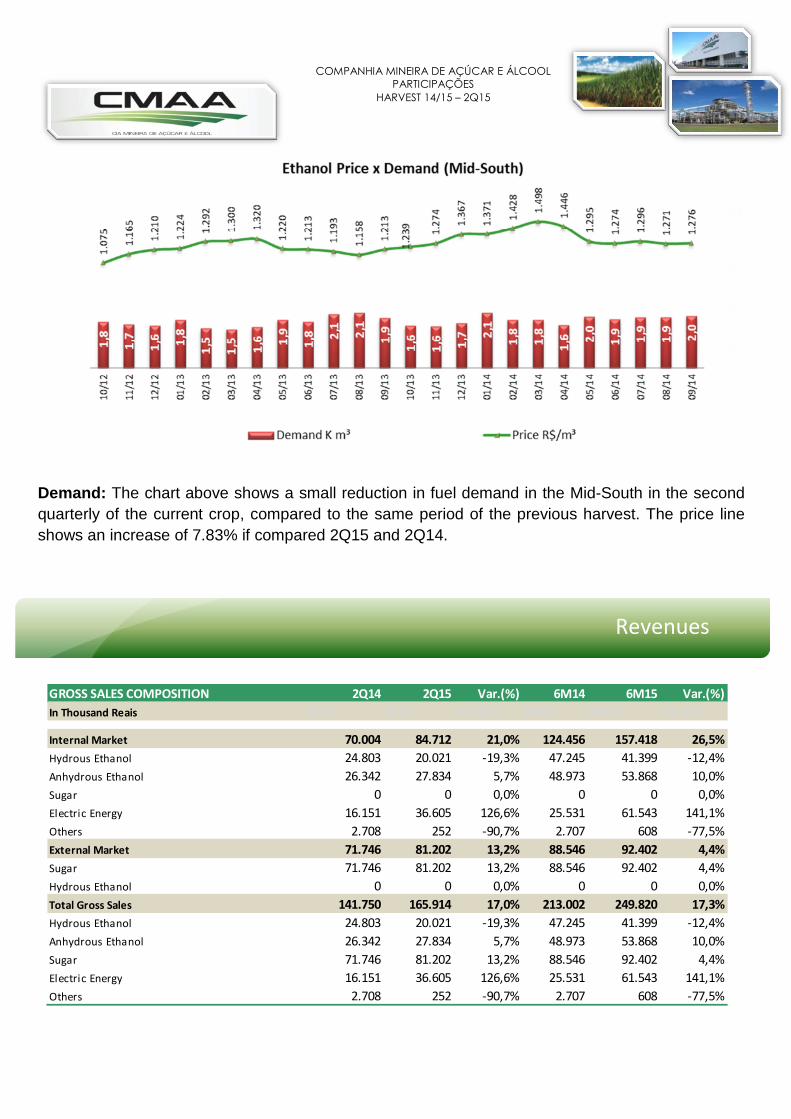

Demand: The chart above shows a small reduction in fuel demand in the Mid-South in the second quarterly of the current crop, compared to the same period of the previous harvest. The price line shows an increase of 7.83% if compared 2Q15 and 2Q14.

Revenues

GROSS SALES COMPOSITION 2Q14 2Q15 Var.(%) 6M14 6M15 Var.(%)

In Thousand Reais 2T14 2T15 Var.(%) 6M14 6M15 Var.(%)

Internal Market 70.004 84.712 21,0% 124.456 157.418 26,5%

Hydrous Ethanol 24.803 20.021 -19,3% 47.245 41.399 -12,4%

Anhydrous Ethanol 26.342 27.834 5,7% 48.973 53.868 10,0%

Sugar 0 0 0,0% 0 0 0,0%

Electric Energy 16.151 36.605 126,6% 25.531 61.543 141,1%

Others 2.708 252 -90,7% 2.707 608 -77,5%

External Market 71.746 81.202 13,2% 88.546 92.402 4,4%

Sugar 71.746 81.202 13,2% 88.546 92.402 4,4%

Hydrous Ethanol 0 0 0,0% 0 0 0,0%

Total Gross Sales 141.750 165.914 17,0% 213.002 249.820 17,3%

Hydrous Ethanol 24.803 20.021 -19,3% 47.245 41.399 -12,4%

Anhydrous Ethanol 26.342 27.834 5,7% 48.973 53.868 10,0%

Sugar 71.746 81.202 13,2% 88.546 92.402 4,4%

Electric Energy 16.151 36.605 126,6% 25.531 61.543 141,1%

Others 2.708 252 -90,7% 2.707 608 -77,5%

COMPANHIA MINEIRA DE AÇÚCAR E ÁLCOOL

PARTICIPAÇÕES HARVEST 14/15 – 2Q15

Sugar VHP

Volume (Thousand tons) e Average Price (R$/ton)

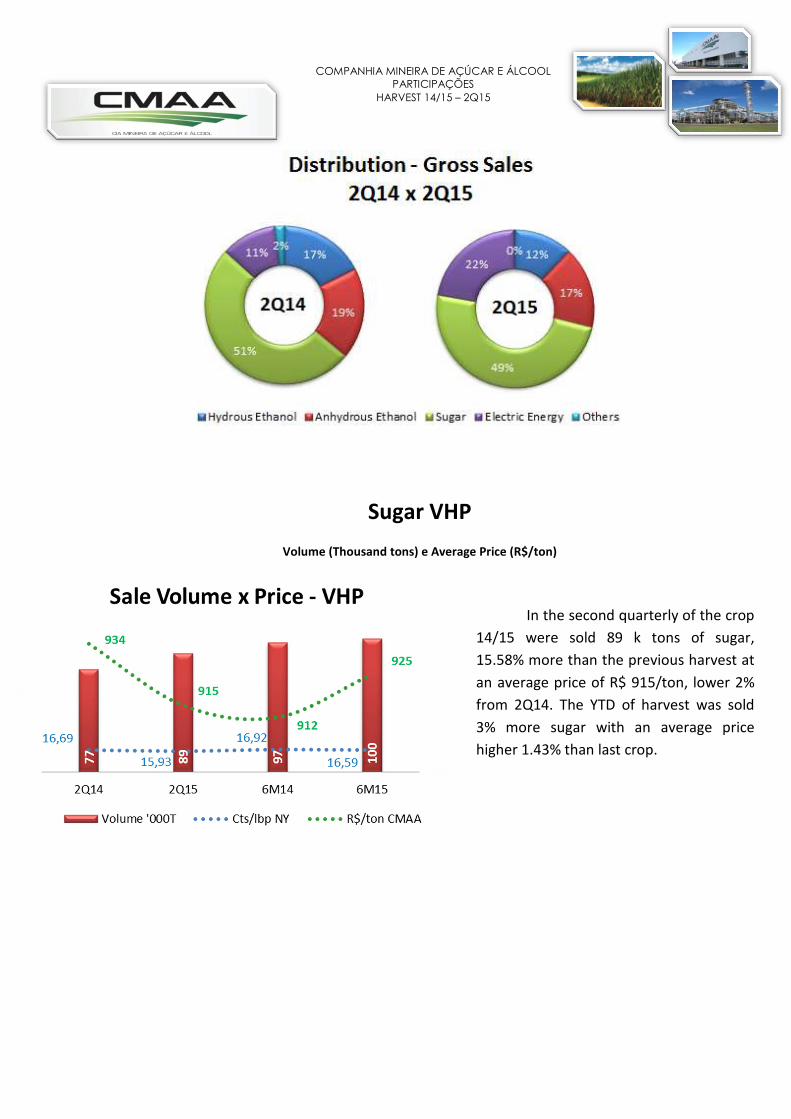

In the second quarterly of the crop

14/15 were sold 89 k tons of sugar,

15.58% more than the previous harvest at

an average price of R$ 915/ton, lower 2%

from 2Q14. The YTD of harvest was sold

3% more sugar with an average price

higher 1.43% than last crop.

COMPANHIA MINEIRA DE AÇÚCAR E ÁLCOOL

PARTICIPAÇÕES HARVEST 14/15 – 2Q15

Ethanol

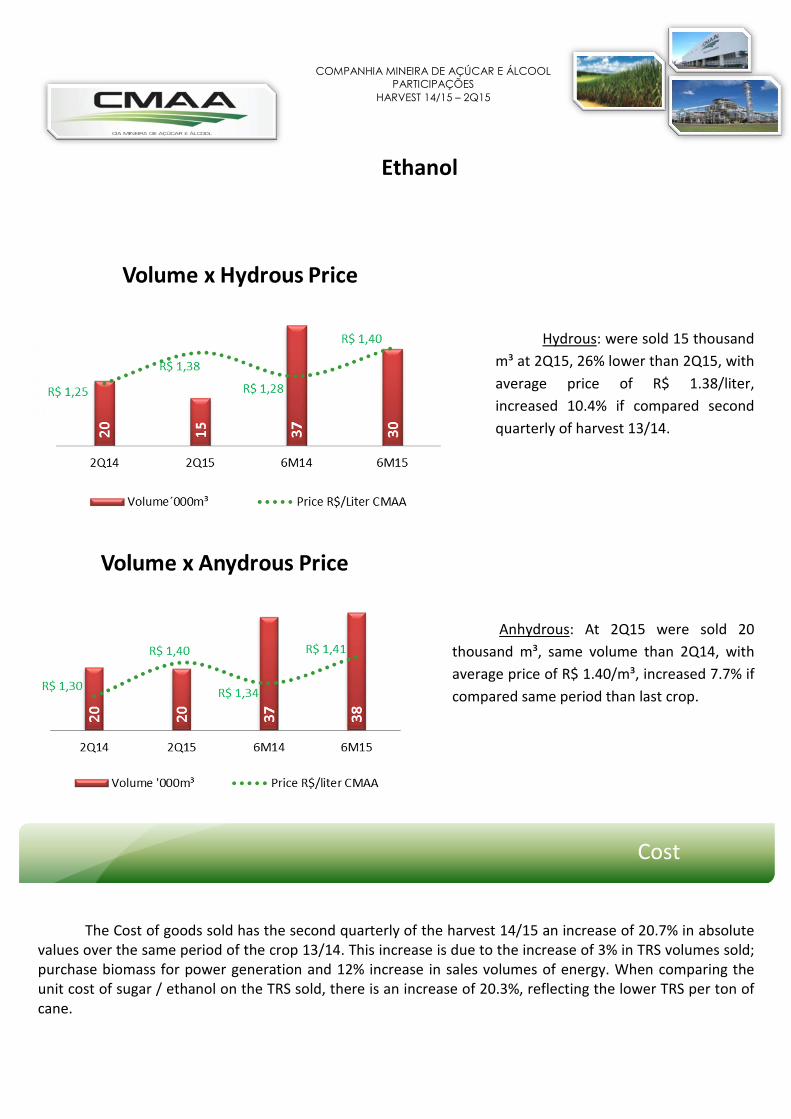

Hydrous: were sold 15 thousand

m³ at 2Q15, 26% lower than 2Q15, with

average price of R$ 1.38/liter,

increased 10.4% if compared second

quarterly of harvest 13/14.

Anhydrous: At 2Q15 were sold 20

thousand m³, same volume than 2Q14, with

average price of R$ 1.40/m³, increased 7.7% if

compared same period than last crop.

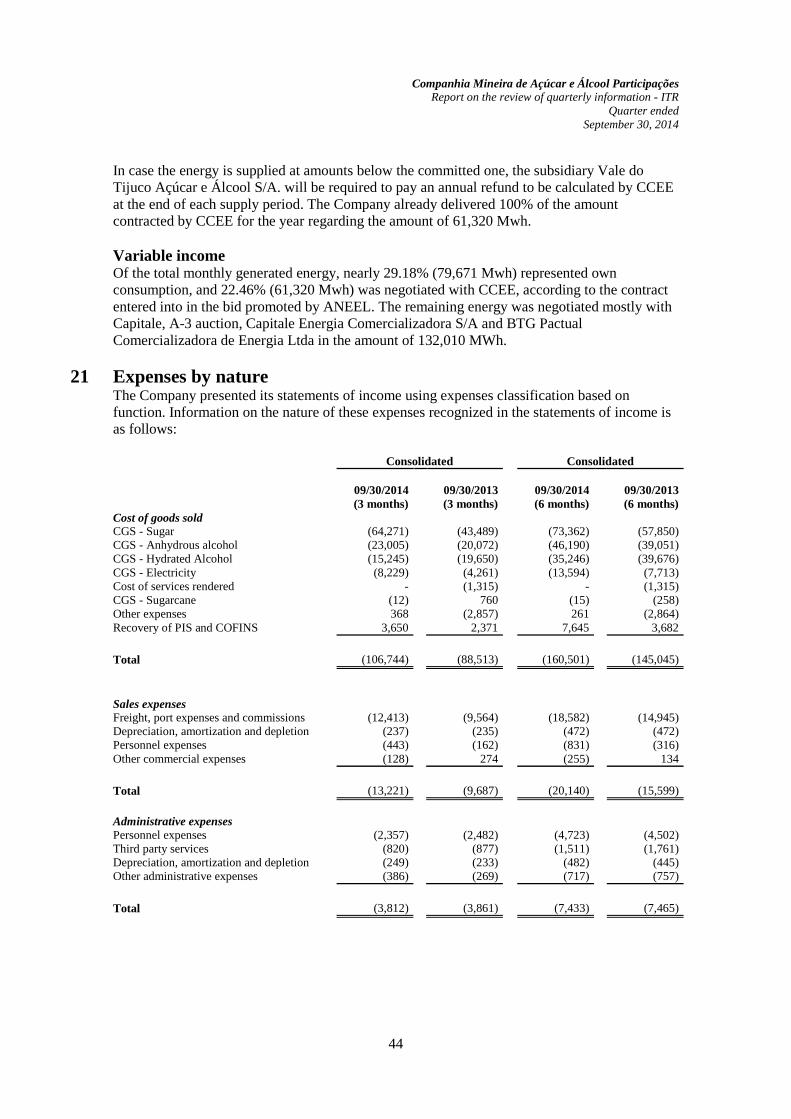

The Cost of goods sold has the second quarterly of the harvest 14/15 an increase of 20.7% in absolute

values over the same period of the crop 13/14. This increase is due to the increase of 3% in TRS volumes sold; purchase biomass for power generation and 12% increase in sales volumes of energy. When comparing the unit cost of sugar / ethanol on the TRS sold, there is an increase of 20.3%, reflecting the lower TRS per ton of cane.

Cost

COMPANHIA MINEIRA DE AÇÚCAR E ÁLCOOL

PARTICIPAÇÕES HARVEST 14/15 – 2Q15

Sales: At 2Q15 increased 36.5% than 2Q14. The variation is due increase of 15.5% in VHP volumes

transported to port and increase of 18% in freight prices.

Administrative: Decrease of 1.3% on administrative expenses if compared second quarterly of harvest

15/16 to second quarterly of last crop.

Expenses

COGS 2Q14 2Q15 Var.(%) 6M14 6M15 Var.(%)

In Thousand Reais 2T14 2T15 Var.(%) 6M14 6M15 Var.(%)

Sugar 41.761 62.071 48,6% 56.154 70.633 25,8%

Ethanol 38.062 36.801 -3,3% 76.614 76.953 0,4%

Electric Energy 4.055 7.927 95,5% 7.468 12.897 72,7%

Others 4.635 -55 -101,2% 4.809 18 -99,6%

Total COGS 88.513 106.744 20,6% 145.045 160.501 10,7%

TRS Sold (Thousand Tons) 141 145 3,0% 213 207 -2,6%

Unit Cost (Sugar&Ethanol COGS/TRS) 566 681 20,3% 625 713 14,1%

Sales Expenses 2Q14 2Q15 Var.(%) 6M14 6M15 Var.(%)

In Thousand Reais

Freight of transfers and sales 7.050 9.589 36,0% 11.567 15.119 30,7%

Port Charges 2.149 2.520 17,3% 2.683 2.844 6,0%

Comissions and Sales fees 18 328 1771,0% 358 677 89,1%

Personnel expenses 161 261 62,2% 314 459 46,0%

Depreciation 235 237 0,9% 472 472 0,1%

Rent 6 0 -95,5% 27 0 -98,8%

Others Expenses 68 286 318,9% 178 569 219,0%

Total 9.687 13.221 36,5% 15.599 20.140 29,1%

Administrative Expenses 2Q14 2Q15 Var.(%) 6M14 6M15 Var.(%)

In Thousand Reais

Personnel expenses 2.217 2.253 1,7% 4.145 4.509 8,8%

General expenses and Outsourced Services 1.342 1.243 -7,3% 2.633 2.308 -12,3%

Depreciation 233 249 6,8% 445 482 8,3%

Tax, fees and contribuitions 42 38 -8,9% 149 81 -45,7%

Rent 27 29 7,5% 93 53 -43,3%

Total 3.861 3.812 -1,3% 7.465 7.433 -0,4%

COMPANHIA MINEIRA DE AÇÚCAR E ÁLCOOL

PARTICIPAÇÕES HARVEST 14/15 – 2Q15

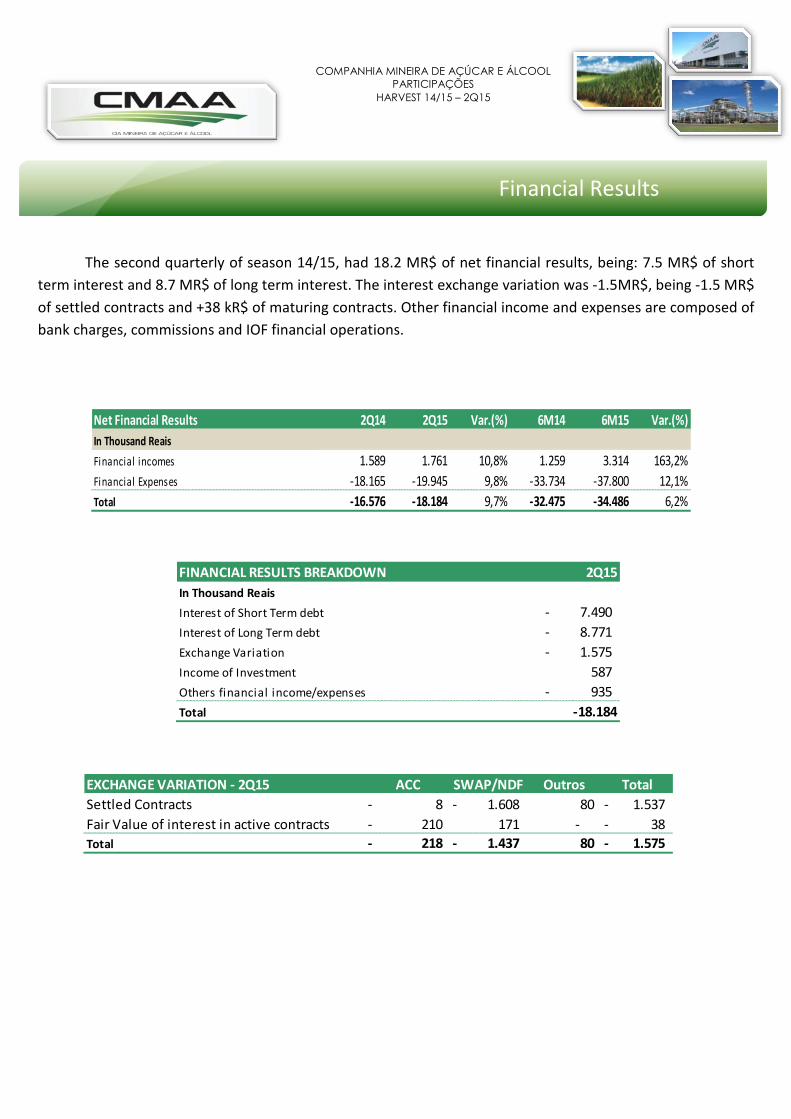

The second quarterly of season 14/15, had 18.2 MR$ of net financial results, being: 7.5 MR$ of short

term interest and 8.7 MR$ of long term interest. The interest exchange variation was -1.5MR$, being -1.5 MR$

of settled contracts and +38 kR$ of maturing contracts. Other financial income and expenses are composed of

bank charges, commissions and IOF financial operations.

Financial Results

FINANCIAL RESULTS BREAKDOWN 2Q15

In Thousand Reais

Interest of Short Term debt 7.490-

Interest of Long Term debt 8.771-

Exchange Variation 1.575-

Income of Investment 587

Others financial income/expenses 935-

Total -18.184

EXCHANGE VARIATION - 2Q15 ACC SWAP/NDF Outros Total

Settled Contracts 8- 1.608- 80 1.537-

Fair Value of interest in active contracts 210- 171 - 38-

Total 218- 1.437- 80 1.575-

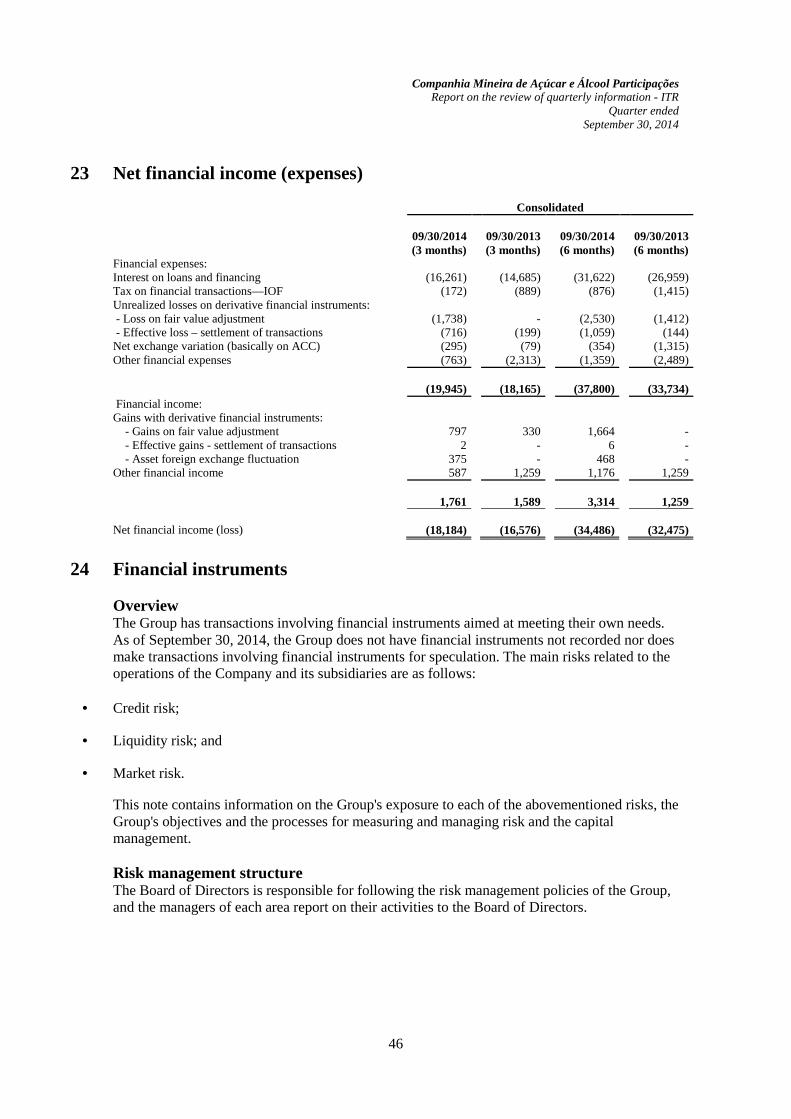

Net Financial Results 2Q14 2Q15 Var.(%) 6M14 6M15 Var.(%)

In Thousand Reais

Financial incomes 1.589 1.761 10,8% 1.259 3.314 163,2%

Financial Expenses -18.165 -19.945 9,8% -33.734 -37.800 12,1%

Total -16.576 -18.184 9,7% -32.475 -34.486 6,2%

COMPANHIA MINEIRA DE AÇÚCAR E ÁLCOOL

PARTICIPAÇÕES HARVEST 14/15 – 2Q15

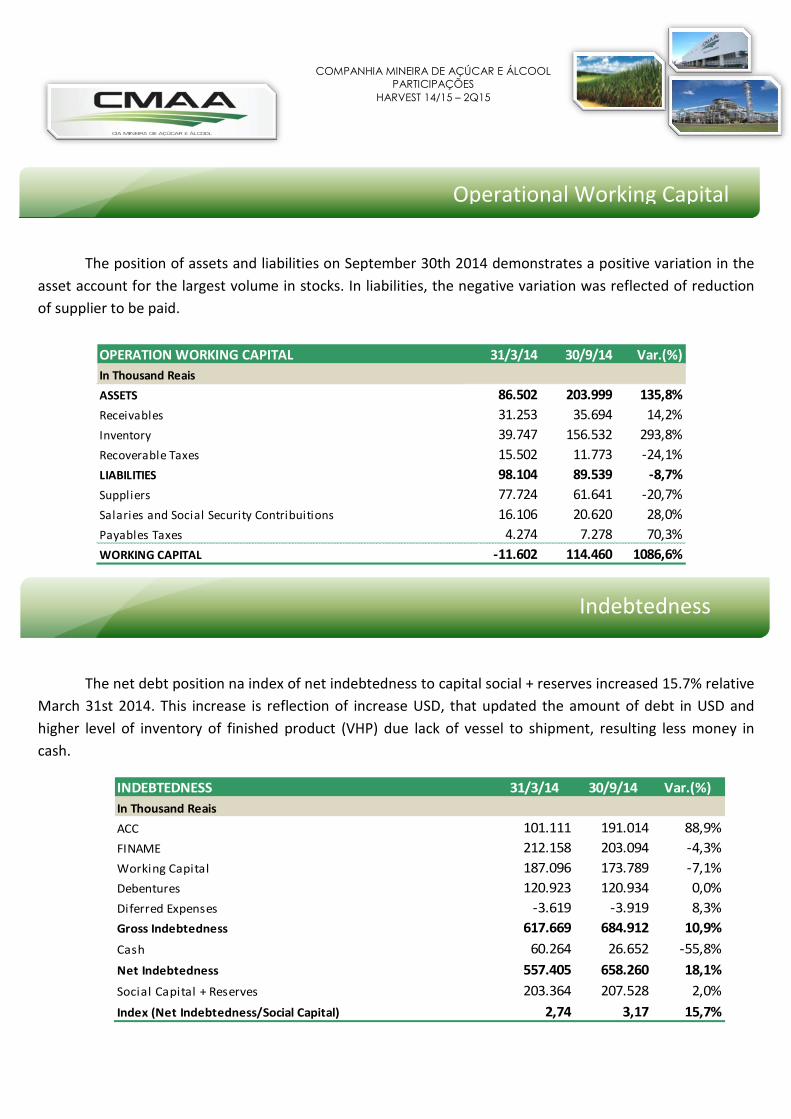

The position of assets and liabilities on September 30th 2014 demonstrates a positive variation in the

asset account for the largest volume in stocks. In liabilities, the negative variation was reflected of reduction

of supplier to be paid.

The net debt position na index of net indebtedness to capital social + reserves increased 15.7% relative

March 31st 2014. This increase is reflection of increase USD, that updated the amount of debt in USD and

higher level of inventory of finished product (VHP) due lack of vessel to shipment, resulting less money in

cash.

INDEBTEDNESS 31/3/14 30/9/14 Var.(%)

In Thousand Reais

ACC 101.111 191.014 88,9%

FINAME 212.158 203.094 -4,3%

Working Capital 187.096 173.789 -7,1%

Debentures 120.923 120.934 0,0%

Diferred Expenses -3.619 -3.919 8,3%

Gross Indebtedness 617.669 684.912 10,9%

Cash 60.264 26.652 -55,8%

Net Indebtedness 557.405 658.260 18,1%

Social Capital + Reserves 203.364 207.528 2,0%

Index (Net Indebtedness/Social Capital) 2,74 3,17 15,7%

Indebtedness

Operational Working Capital

OPERATION WORKING CAPITAL 31/3/14 30/9/14 Var.(%)

In Thousand Reais

ASSETS 86.502 203.999 135,8%

Receivables 31.253 35.694 14,2%

Inventory 39.747 156.532 293,8%

Recoverable Taxes 15.502 11.773 -24,1%

LIABILITIES 98.104 89.539 -8,7%

Suppliers 77.724 61.641 -20,7%

Salaries and Social Security Contribuitions 16.106 20.620 28,0%

Payables Taxes 4.274 7.278 70,3%

WORKING CAPITAL -11.602 114.460 1086,6%

COMPANHIA MINEIRA DE AÇÚCAR E ÁLCOOL

PARTICIPAÇÕES HARVEST 14/15 – 2Q15

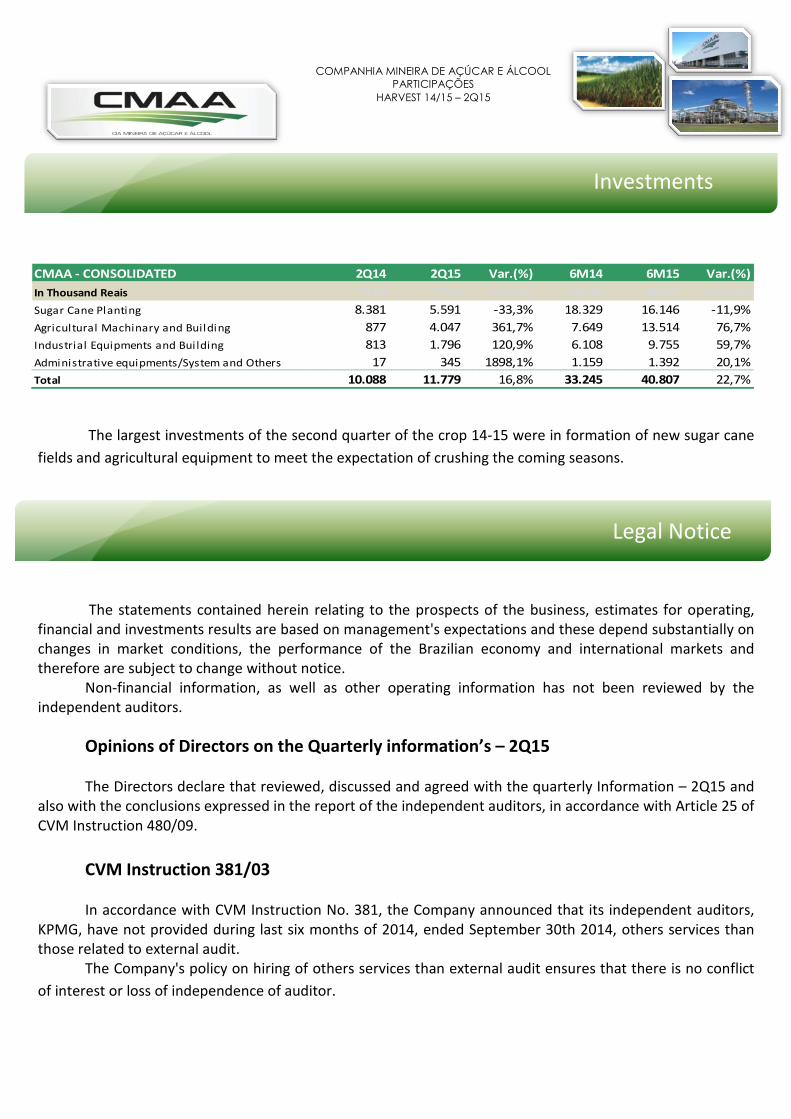

The largest investments of the second quarter of the crop 14-15 were in formation of new sugar cane

fields and agricultural equipment to meet the expectation of crushing the coming seasons.

The statements contained herein relating to the prospects of the business, estimates for operating,

financial and investments results are based on management's expectations and these depend substantially on changes in market conditions, the performance of the Brazilian economy and international markets and therefore are subject to change without notice.

Non-financial information, as well as other operating information has not been reviewed by the independent auditors.

Opinions of Directors on the Quarterly information’s – 2Q15

The Directors declare that reviewed, discussed and agreed with the quarterly Information – 2Q15 and also with the conclusions expressed in the report of the independent auditors, in accordance with Article 25 of CVM Instruction 480/09.

CVM Instruction 381/03 In accordance with CVM Instruction No. 381, the Company announced that its independent auditors,

KPMG, have not provided during last six months of 2014, ended September 30th 2014, others services than those related to external audit.

The Company's policy on hiring of others services than external audit ensures that there is no conflict

of interest or loss of independence of auditor.

Legal Notice

Investments

CMAA - CONSOLIDATED 2Q14 2Q15 Var.(%) 6M14 6M15 Var.(%)

In Thousand Reais 2T14 2T15 Var.(%) 6M14 6M15 Var.(%)

Sugar Cane Planting 8.381 5.591 -33,3% 18.329 16.146 -11,9%

Agricultural Machinary and Building 877 4.047 361,7% 7.649 13.514 76,7%

Industrial Equipments and Building 813 1.796 120,9% 6.108 9.755 59,7%

Administrative equipments/System and Others 17 345 1898,1% 1.159 1.392 20,1%

Total 10.088 11.779 16,8% 33.245 40.807 22,7%

COMPANHIA MINEIRA DE AÇÚCAR E ÁLCOOL

PARTICIPAÇÕES HARVEST 14/15 – 2Q15

The CMAA is a public company registered with the CVM and was created to be a hub for three mills of

ethanol, sugar and energy, crushing a total of 12.9 million tons per year. It is located in a region close to major consumption centers (in Triângulo Mineiro). Currently operation is unit Usina Vale do Tijuco, in Uberaba(MG), which was designed with total processing capacity of 4 Million Tons of sugarcane and export up to 210 MW. This plant started its first season in April 2010 with a crushing of 1.2 million tons, with the second season in 2011, with a grinding of 1.66 million tons of sugarcane, already producing VHP, anhydrous & hydrous ethanol and electric energy. For the season 2012/2013 was crushed 2.2 million tons and for harvest 2013/14 crushed

3 million tons of sugarcane. The prevision of harvest 14/15 is crushing 3.5 million tons of sugarcane.

About CMAA Group

COMPANHIA MINEIRA DE AÇÚCAR E ÁLCOOL

PARTICIPAÇÕES HARVEST 14/15 – 2Q15

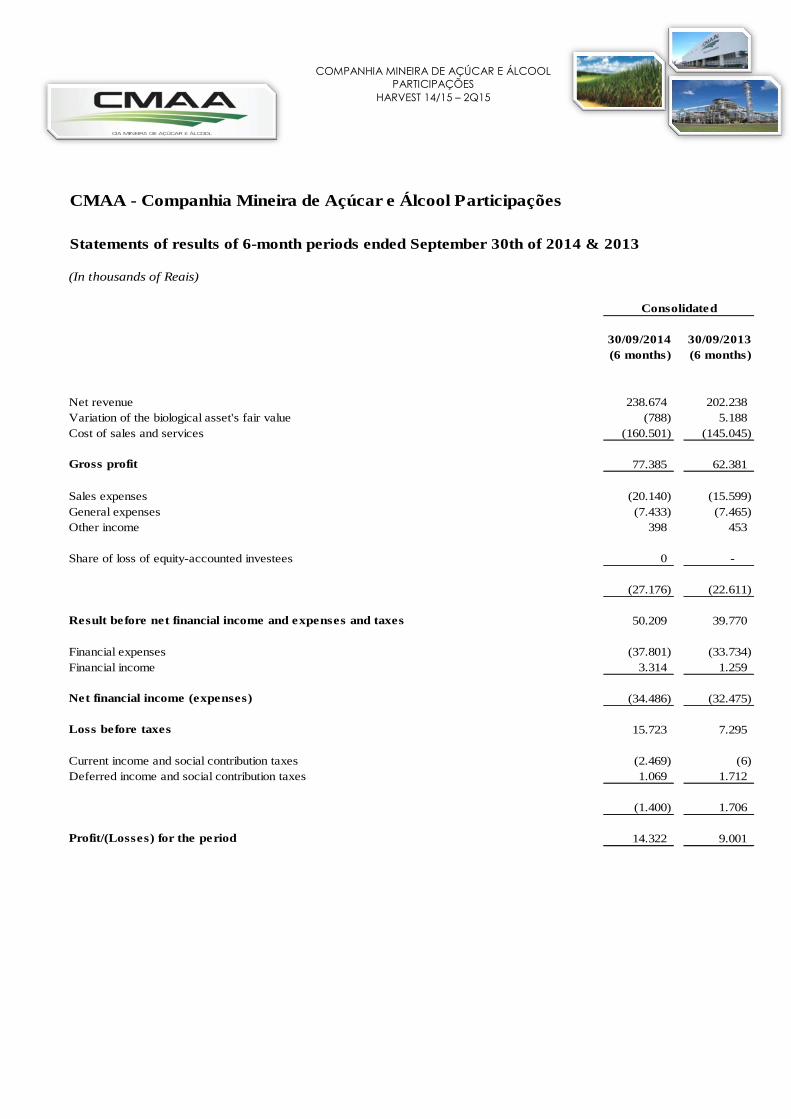

CMAA - Companhia Mineira de Açúcar e Álcool Participações

Statements of results of 6-month periods ended September 30th of 2014 & 2013

(In thousands of Reais)

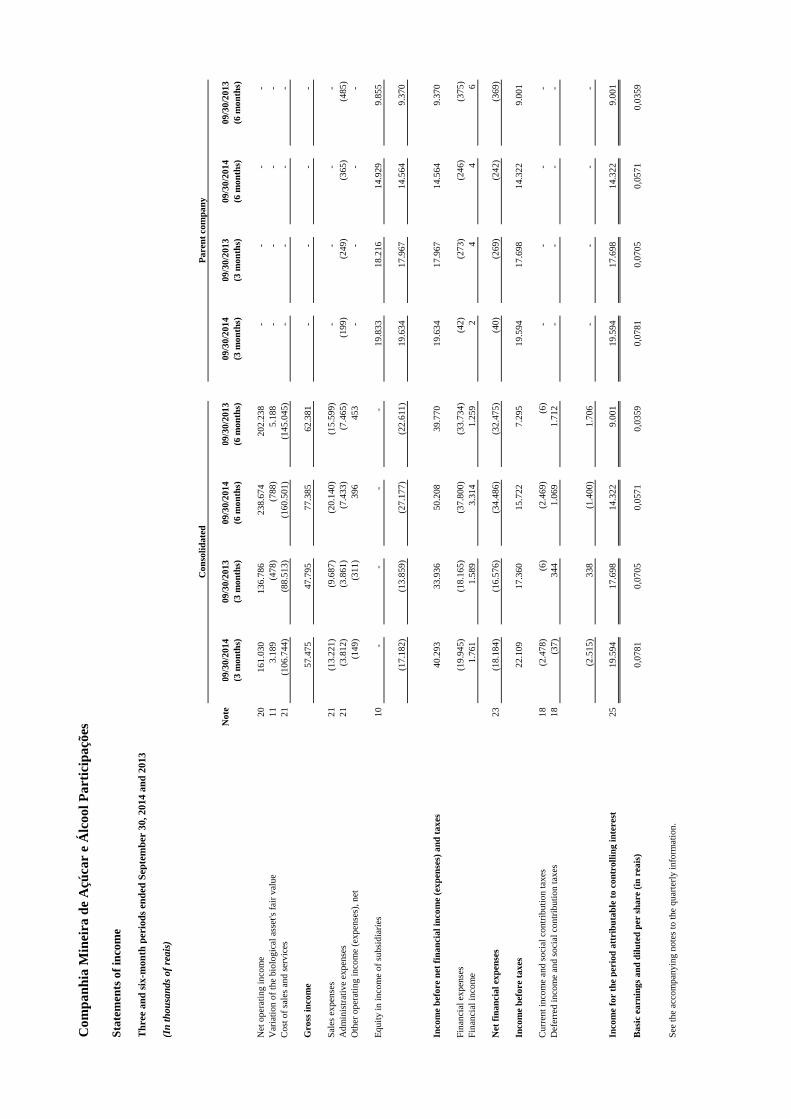

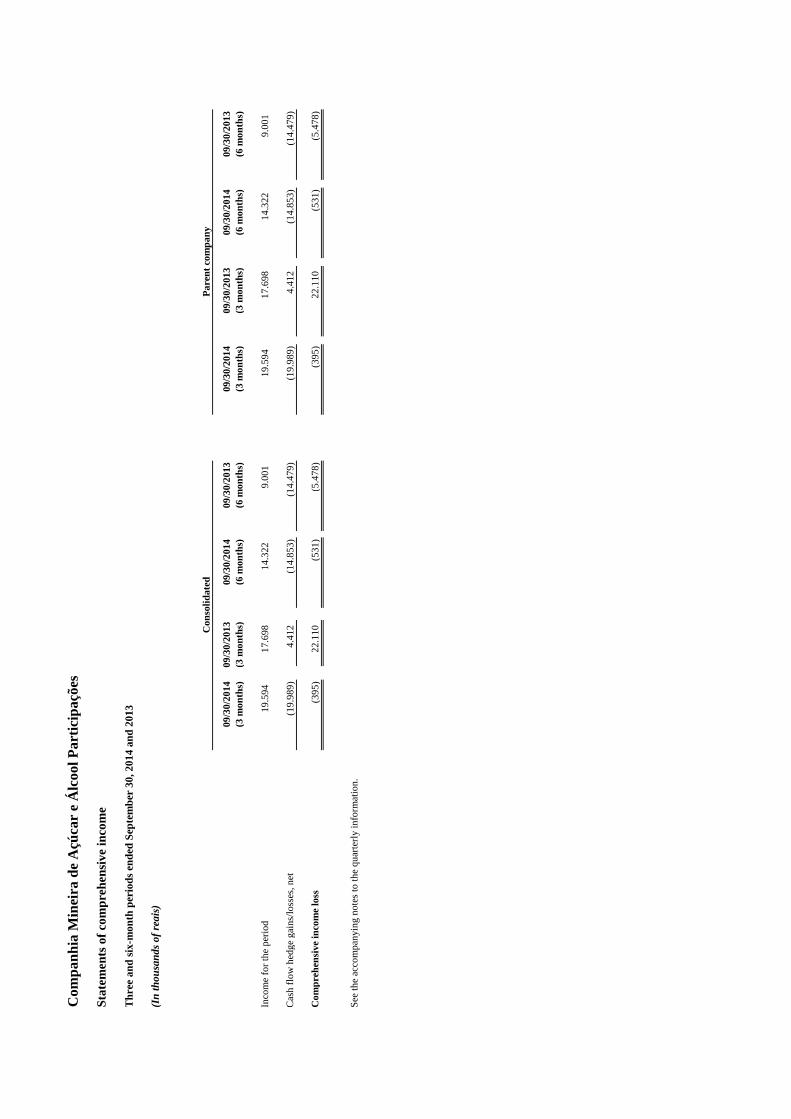

30/09/2014 30/09/2013(6 months) (6 months)

Net revenue 238.674 202.238 Variation of the biological asset's fair value (788) 5.188 Cost of sales and services (160.501) (145.045)

Gross profit 77.385 62.381

Sales expenses (20.140) (15.599) General expenses (7.433) (7.465) Other income 398 453

Share of loss of equity-accounted investees 0 -

(27.176) (22.611)

Result before net financial income and expenses and taxes 50.209 39.770

Financial expenses (37.801) (33.734) Financial income 3.314 1.259

Net financial income (expenses) (34.486) (32.475)

Loss before taxes 15.723 7.295

Current income and social contribution taxes (2.469) (6) Deferred income and social contribution taxes 1.069 1.712

(1.400) 1.706

Profit/(Losses) for the period 14.322 9.001

Consolidated

COMPANHIA MINEIRA DE AÇÚCAR E ÁLCOOL

PARTICIPAÇÕES HARVEST 14/15 – 2Q15

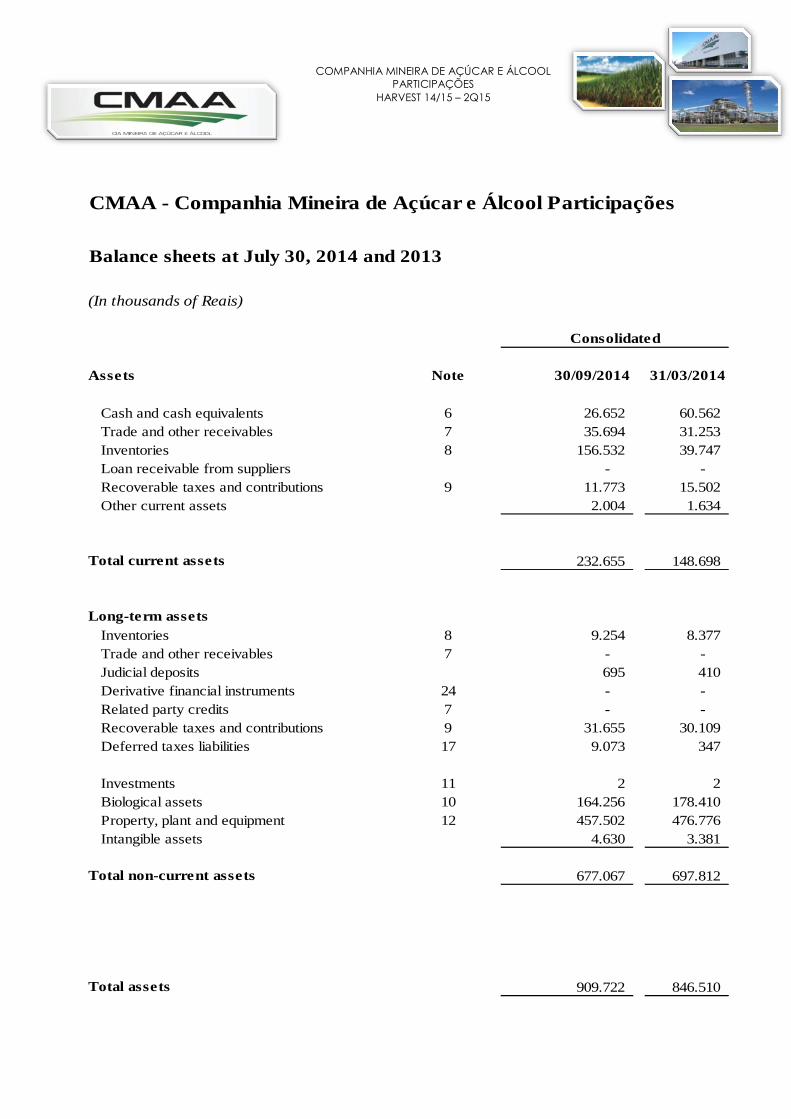

CMAA - Companhia Mineira de Açúcar e Álcool Participações

Balance sheets at July 30, 2014 and 2013

(In thousands of Reais)

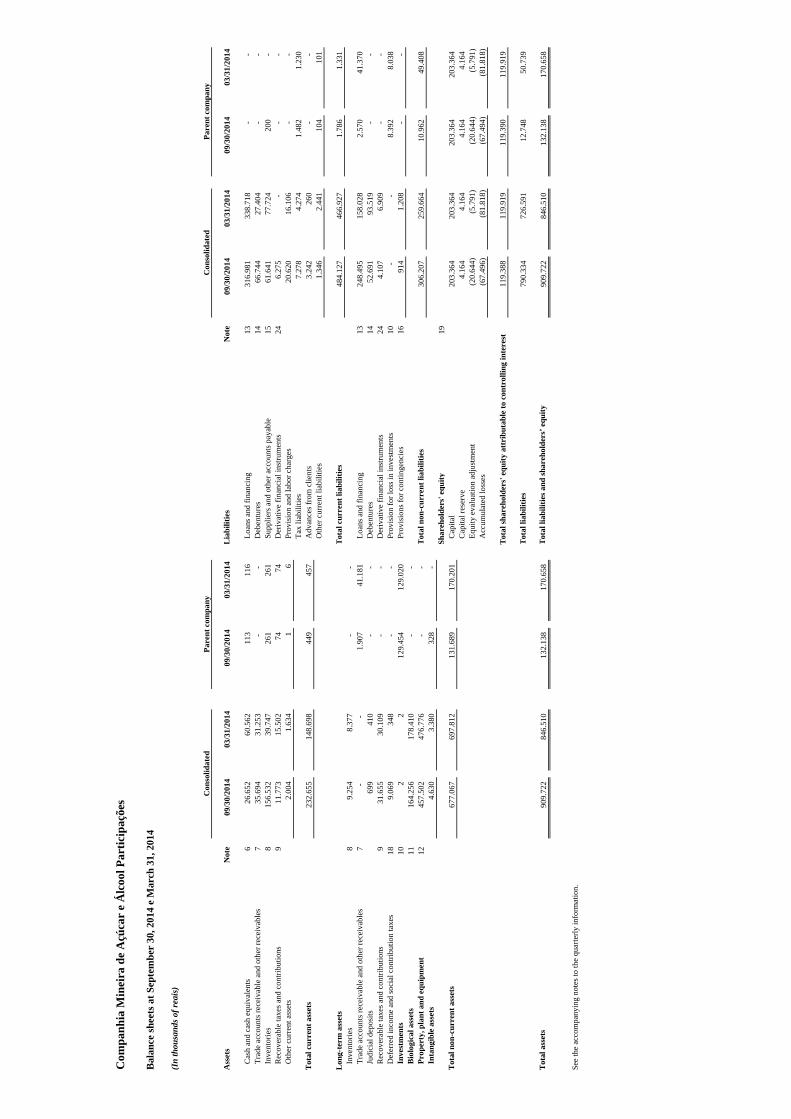

Assets Note 30/09/2014 31/03/2014

Cash and cash equivalents 6 26.652 60.562 Trade and other receivables 7 35.694 31.253 Inventories 8 156.532 39.747 Loan receivable from suppliers - - Recoverable taxes and contributions 9 11.773 15.502 Other current assets 2.004 1.634

Total current assets 232.655 148.698

Long-term assetsInventories 8 9.254 8.377 Trade and other receivables 7 - - Judicial deposits 695 410 Derivative financial instruments 24 - - Related party credits 7 - - Recoverable taxes and contributions 9 31.655 30.109 Deferred taxes liabilities 17 9.073 347

Investments 11 2 2 Biological assets 10 164.256 178.410 Property, plant and equipment 12 457.502 476.776 Intangible assets 4.630 3.381

Total non-current assets 677.067 697.812

Total assets 909.722 846.510

Consolidated

COMPANHIA MINEIRA DE AÇÚCAR E ÁLCOOL

PARTICIPAÇÕES HARVEST 14/15 – 2Q15

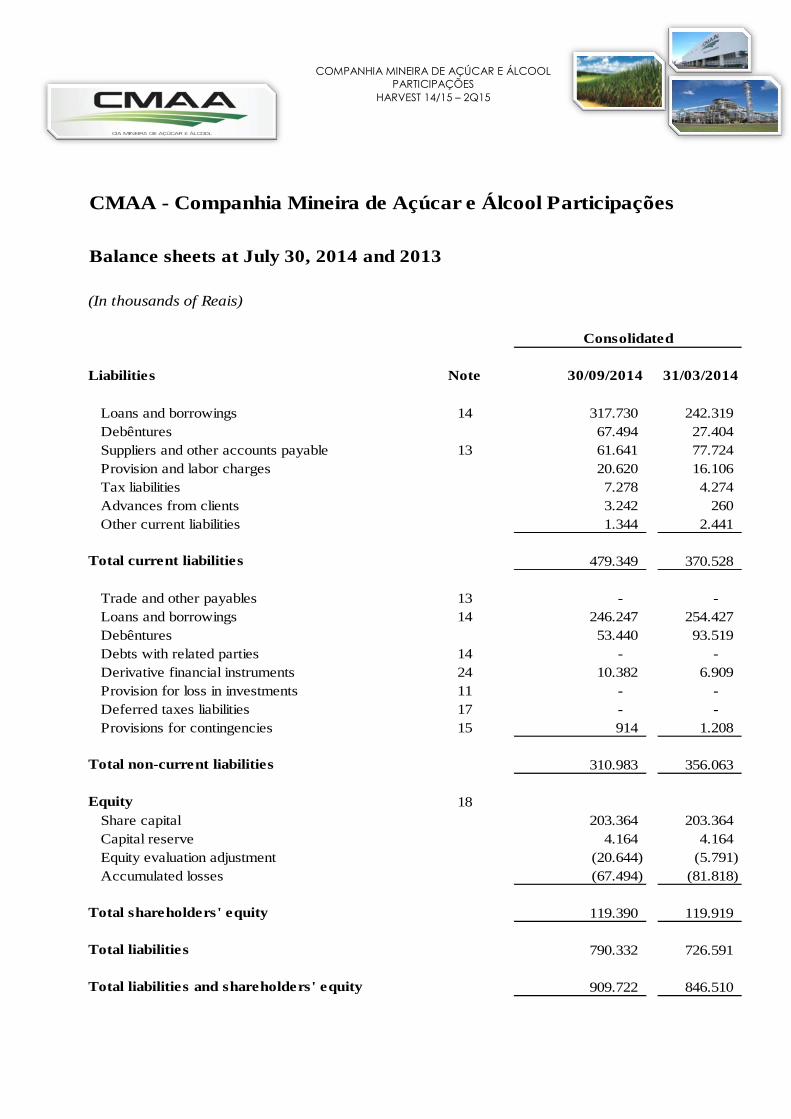

CMAA - Companhia Mineira de Açúcar e Álcool Participações

Balance sheets at July 30, 2014 and 2013

(In thousands of Reais)

Liabilities Note 30/09/2014 31/03/2014

Loans and borrowings 14 317.730 242.319 Debêntures 67.494 27.404 Suppliers and other accounts payable 13 61.641 77.724 Provision and labor charges 20.620 16.106 Tax liabilities 7.278 4.274 Advances from clients 3.242 260 Other current liabilities 1.344 2.441

Total current liabilities 479.349 370.528

Trade and other payables 13 - - Loans and borrowings 14 246.247 254.427 Debêntures 53.440 93.519 Debts with related parties 14 - - Derivative financial instruments 24 10.382 6.909 Provision for loss in investments 11 - - Deferred taxes liabilities 17 - - Provisions for contingencies 15 914 1.208

Total non-current liabilities 310.983 356.063 Equity 18

Share capital 203.364 203.364 Capital reserve 4.164 4.164 Equity evaluation adjustment (20.644) (5.791) Accumulated losses (67.494) (81.818)

Total shareholders' equity 119.390 119.919

Total liabilities 790.332 726.591

Total liabilities and shareholders' equity 909.722 846.510

Consolidated

COMPANHIA MINEIRA DE AÇÚCAR E ÁLCOOL

PARTICIPAÇÕES HARVEST 14/15 – 2Q15

Kind Regards,

Chairman Industrial Director

Carlos Eduardo T. Santos Celso Oliveira

CFO Agricultural Director

Sylvio Ortega Filho Eduardo Scandiuzzi

Accountant

Anderson Cesar Augusto Alves

KPDS 100700

Companhia Mineira de Açúcar e Álcool Participações

Report on the review of quarterly information - ITR

quarter ended September 30, 2014

Companhia Mineira de Açúcar e Álcool Participações

Report on the review of quarterly information - ITR quarter ended

September 30, 2014

2

Contents Report on the review of quarterly information - ITR 3 Balance sheets 5 Statements of income 6 Statements of comprehensive income 7 Statements of changes in shareholders' equity 8 Statements of cash flows – Indirect method 9 Statements of added value 10 Notes to the quarterly financial information 11

3

Report on the review of quarterly information - ITR To the Board Members and Shareholders of Companhia Mineira de Açúcar e Álcool Participações Uberaba - Minas Gerais Introduction We have reviewed the interim, individual and consolidated financial information of Company, contained in the Quarterly Information – ITR Form for the quarter ended September 30, 2014, which comprise the balance sheet as of September 30, 2014 and related statements of income, of comprehensive income for the three and six-month periods then ended, of changes in shareholders' equity and of cash flows for the six-month period then ended, including the explanatory notes. The Company's Management is responsible for the preparation of the individual interim accounting information in accordance with Technical Pronouncement CPC 21 (RI) - Interim Statement and of the consolidated interim accounting information in accordance with CPC 21 (R1) and with international standard IAS 34 - Interim Financial Reporting, issued by the International Accounting Standards Board - IASB, as well as for the presentation of this information in a manner consistent with the standards issued by the Brazilian Securities and Exchange Commission, applicable to the preparation of the Quarterly Information - ITR. Our responsibility is to express a conclusion on this interim financial information based on our review. Scope of the review We conducted our review in accordance with the Brazilian and international review standards for interim information (NBC TR 2410 - Review of Interim Financial Information Performed by the Independent Auditor of the Entity and ISRE 2410 - Review of Interim Financial Information Performed by the Independent Auditor of the Entity, respectively). A review of interim information consists in asking questions, chiefly to the persons in charge of financial and accounting affairs, and in applying analytical procedures and other review procedures. A review is substantially less in scope than an audit conducted in accordance with Brazilian and International Standards on Auditing and consequently does not enable us to obtain assurance that we would become aware of all significant matters that might be identified in an audit. Accordingly, we do not express an audit opinion.

4

Conclusion on the individual interim information Based on our review, we are not aware of any facts that would lead us to believe that the individual interim accounting information included in the quarterly information referred to above was not prepared, in all material respects, in accordance with CPC 21 (R1) applicable to the preparation of Quarterly Information - ITR, and presented in a manner consistent with the standards issued by the Brazilian Securities and Exchange Commission. Conclusion on the consolidated interim information Based on our review, we are not aware of any facts that would lead us to believe that the consolidated interim accounting information included in the quarterly information referred to above was not prepared, in all material respects, in accordance with CPC 21 (R1) and IAS 34 applicable to the preparation of Quarterly Information - ITR, and presented in a manner consistent with the standards issued by the Brazilian Securities and Exchange Commission. Emphasis Going concern Without qualifying our opinion, we call your attention to note 1 to the financial quarterly information, which indicates that on that date, the Company’s consolidated current liabilities exceeded the total current assets by R$ 251,472 thousand. These conditions, together with other matters, as described in Note 1, indicate that a significant uncertainty exists and may raise significant doubts on the Company's capacity of continuing as a going concern. Other issues Statements of added value We also reviewed the individual and consolidated statements of added value (SAV) for the six-month period ended on September 30, 2014, prepared by the Company's management, whose presentation in the interim information is required according to the standards issued by the CVM – Brazilian Securities and Exchange Commission, applicable to the preparation of Quarterly Information - ITR and considered supplementary information by the IFRS, which do not require the presentation of the SAV. These statements were subjected to the review procedures previously described and, based on our review, we are not aware of any other event that make us believe that those were not prepared, in all material respects, in accordance with the individual and consolidated interim accounting information taken as a whole. São Carlos, November 05, 2014. KPMG Auditores Independentes CRC SP-014428/O-6 F-MG André Luiz Monaretti Accountant CRC 1SP160909/O-3

Com

panh

ia M

inei

ra d

e A

çúca

r e

Álc

ool P

artic

ipaç

ões

Bal

ance

she

ets

at S

epte

mbe

r 30

, 201

4 e

Mar

ch 3

1, 2

014

(In

thou

sand

s of

rea

is)

Ass

ets

Not

e09

/30/

2014

03/3

1/20

1409

/30/

2014

03/3

1/20

14Li

abili

ties

Not

e09

/30/

2014

03/3

1/20

1409

/30/

2014

03/3

1/20

14

Cas

h a

nd

cas

h e

qu

ival

ents

62

6.6

52

60

.56

2

#

##

11

3

11

6

#L

oan

s an

d fi

nan

cin

g1

33

16

.98

1

33

8.7

18

#

-

-

Tra

de

acco

un

ts r

ecei

vab

le a

nd

oth

er r

ecei

vab

les

73

5.6

94

31

.25

3

#

##

-

-

#D

eben

ture

s1

46

6.7

44

27

.40

4

#

-

-

Inve

nto

ries

81

56

.53

2

39

.74

7

#

##

26

1

26

1

#S

up

plie

rs a

nd

oth

er a

cco

un

ts p

ayab

le1

56

1.6

41

77

.72

4

#

20

0

-

Rec

ove

rab

le ta

xes

and

co

ntr

ibu

tion

s9

11

.77

3

1

5.5

02

##

#7

4

7

4

#

Der

ivat

ive

finan

cial

inst

rum

ents

24

6.2

75

-

-

-

Oth

er c

urr

ent a

sset

s2

.00

4

1

.63

4

3

70

1

6

#

Pro

visi

on

an

d la

bo

r ch

arg

es2

0.6

20

16

.10

6

#

-

-

- #

Tax

liab

ilitie

s7

.27

8

4

.27

4

#

1.4

82

1.2

30

Tot

al c

urre

nt a

sset

s2

32

.65

5

14

8.6

98

#

##

44

9

45

7

#A

dva

nce

s fr

om

clie

nts

3.2

42

26

0

# -

-

O

ther

cu

rren

t lia

bili

ties

1.3

46

2.4

41

#1

04

1

01

-

##

Long

-ter

m a

sset

s-

#T

otal

cur

rent

liab

ilitie

s4

84

.12

7

46

6.9

27

#

1.7

86

1.3

31

Inve

nto

ries

89

.25

4

8

.37

7

8

77

-

-

#

#T

rad

e ac

cou

nts

rec

eiva

ble

an

d o

ther

rec

eiva

ble

s7

-

-

- 1

.90

7

4

1.1

81

#L

oan

s an

d fi

nan

cin

g1

32

48

.49

5

15

8.0

28

#

2.5

70

41

.37

0

Ju

dic

ial d

epo

sits

69

9

41

0

28

9

-

-

#D

eben

ture

s1

45

2.6

91

93

.51

9

#

-

-

Rec

ove

rab

le ta

xes

and

co

ntr

ibu

tion

s9

31

.65

5

3

0.1

09

##

# -

-

#

Der

ivat

ive

finan

cial

inst

rum

ents

24

4.1

07

6.9

09

# -

-

D

efer

red

inco

me

and

so

cial

co

ntr

ibu

tion

taxe

s1

89

.06

9

3

48

#

##

-

-

#P

rovi

sio

n fo

r lo

ss in

inve

stm

ents

10

-

-

#8

.39

2

8

.03

8

In

vest

men

ts1

02

2

-

12

9.4

54

1

29

.02

0

#P

rovi

sio

ns

for

con

ting

enci

es1

69

14

1

.20

8

#

-

-

Bio

logi

cal a

sset

s1

11

64

.25

6

17

8.4

10

#

##

-

-

##

Pro

pert

y, p

lant

and

equ

ipm

ent

12

45

7.5

02

4

76

.77

6

##

# -

-

#

Tot

al n

on-c

urre

nt li

abili

ties

30

6.2

07

2

59

.66

4

#1

0.9

62

49

.40

8

In

tang

ible

ass

ets

4.6

30

3.3

80

##

#3

28

-

#

#-

#S

hare

hold

ers'

equ

ity1

9#

Tot

al n

on-c

urre

nt a

sset

s6

77

.06

7

69

7.8

12

#

##

13

1.6

89

1

70

.20

1

#C

apita

l2

03

.36

4

20

3.3

64

#

20

3.3

64

2

03

.36

4

- #

Cap

ital r

eser

ve4

.16

4

4

.16

4

#

4.1

64

4.1

64

- #

Eq

uity

eva

luat

ion

ad

just

men

t(2

0.6

44

)

(5.7

91

)

#

(20

.64

4)

(5

.79

1)

- #

Acc

um

ula

ted

loss

es(6

7.4

96

)

(81

.81

8)

#

(67

.49

4)

(8

1.8

18

)

- #

#-

#T

otal

sha

reho

lder

s' e

quity

attr

ibut

able

to c

ontr

ollin

g in

tere

st1

19

.38

8

11

9.9

19

#

11

9.3

90

1

19

.91

9

- #

##

- #

Tot

al li

abili

ties

79

0.3

34

7

26

.59

1

#1

2.7

48

50

.73

9

-

##

Tot

al a

sset

s9

09

.72

2

84

6.5

10

#

##

13

2.1

38

1

70

.65

8

#T

otal

liab

ilitie

s an

d sh

areh

olde

rs’ e

quity

90

9.7

22

8

46

.51

0

#1

32

.13

8

17

0.6

58

- #

See

the

acco

mp

anyi

ng

no

tes

to th

e q

uar

terly

info

rma

tion

.

Con

solid

ated

Par

ent c

ompa

nyC

onso

lidat

edP

aren

t com

pany

Com

panh

ia M

inei

ra d

e A

çúca

r e

Álc

ool P

artic

ipaç

ões

Sta

tem

ents

of i

ncom

e

Thr

ee a

nd s

ix-m

onth

per

iods

end

ed S

epte

mbe

r 30

, 201

4 an

d 20

13

(In

thou

sand

s of

rea

is)

Not

e09

/30/

2014

09/3

0/20

1309

/30/

2014

09/3

0/20

1309

/30/

2014

09/3

0/20

1309

/30/

2014

09/3

0/20

13(3

mon

ths)

(3 m

onth

s)(6

mon

ths)

(6 m

onth

s)(3

mon

ths)

(3 m

onth

s)(6

mon

ths)

(6 m

onth

s)

Net

op

erat

ing

inco

me

20

16

1.0

30

13

6.7

86

23

8.6

74

20

2.2

38

-

-

-

-

Var

iatio

n o

f th

e b

iolo

gic

al a

sset

's fa

ir v

alu

e1

13

.18

9

(4

78

)

(7

88

)

5

.18

8

-

-

-

-

C

ost

of s

ales

an

d s

ervi

ces

21

(10

6.7

44

)

(8

8.5

13

)

(1

60

.50

1)

(14

5.0

45

)

-

-

-

-

Gro

ss in

com

e5

7.4

75

4

7.7

95

7

7.3

85

6

2.3

81

-

-

-

-

Sal

es e

xpen

ses

21

(13

.22

1)

(9.6

87

)

(20

.14

0)

(15

.59

9)

-

-

-

-

Ad

min

istr

ativ

e ex

pen

ses

21

(3.8

12

)

(3.8

61

)

(7.4

33

)

(7.4

65

)

(19

9)

(24

9)

(36

5)

(48

5)

Oth

er o

per

atin

g in

com

e (e

xpen

ses)

, net

(14

9)

(31

1)

39

6

45

3

-

-

-

-

Eq

uity

in in

com

e o

f su

bsi

dia

ries

10

-

-

-

-

19

.83

3

18

.21

6

14

.92

9

9.8

55

(17

.18

2)

(13

.85

9)

(27

.17

7)

(22

.61

1)

19

.63

4

17

.96

7

14

.56

4

9.3

70

40

.29

3

33

.93

6

50

.20

8

39

.77

0

19

.63

4

17

.96

7

14

.56

4

9.3

70

Fin

anci

al e

xpen

ses

(19

.94

5)

(18

.16

5)

(37

.80

0)

(33

.73

4)

(42

)

(27

3)

(24

6)

(37

5)

Fin

anci

al in

com

e1

.76

1

1

.58

9

3

.31

4

1

.25

9

2

4

4

6

Net

fina

ncia

l exp

ense

s2

3(1

8.1

84

)

(1

6.5

76

)

(3

4.4

86

)

(3

2.4

75

)

(4

0)

(2

69

)

(2

42

)

(3

69

)

Inco

me

befo

re ta

xes

22

.10

9

17

.36

0

15

.72

2

7.2

95

19

.59

4

17

.69

8

14

.32

2

9.0

01

Cu

rren

t in

com

e an

d s

oci

al c

on

trib

utio

n ta

xes

18

(2.4

78

)

(6)

(2.4

69

)

(6)

-

-

-

-

Def

erre

d in

com

e an

d s

oci

al c

on

trib

utio

n ta

xes

18

(37

)

34

4

1.0

69

1.7

12

-

-

-

-

(2.5

15

)

33

8

(1.4

00

)

1.7

06

-

-

-

-

Inco

me

for

the

perio

d at

trib

utab

le to

con

trol

ling

inte

rest

25

19

.59

4

17

.69

8

14

.32

2

9.0

01

19

.59

4

17

.69

8

14

.32

2

9.0

01

Bas

ic e

arni

ngs

and

dilu

ted

per

shar

e (in

rea

is)

0,0

78

1

0,0

70

5

0,0

57

1

0,0

35

9

0,0

78

1

0,0

70

5

0,0

57

1

0,0

35

9

See

the

acco

mp

anyi

ng

no

tes

to th

e q

uar

terl

y in

form

atio

n.

Con

solid

ated

Par

ent c

ompa

ny

Inco

me

befo

re n

et fi

nanc

ial i

ncom

e (e

xpen

ses)

and

tax

es

Com

panh

ia M

inei

ra d

e A

çúca

r e

Álc

ool P

artic

ipaç

ões

Sta

tem

ents

of c

ompr

ehen

sive

inco

me

Thr

ee a

nd s

ix-m

onth

per

iods

end

ed S

epte

mbe

r 30

, 2014

and

2013

(In

thou

sand

s of

rea

is)

09/3

0/20

1409

/30/

2013

09/3

0/20

1409

/30/

2013

09/3

0/20

140

9/30

/201

309

/30/

2014

09/3

0/20

13(3

mon

ths)

(3 m

onth

s)(6

mon

ths)

(6 m

onth

s)(3

mon

ths)

(3 m

onth

s)(6

mon

ths)

(6 m

onth

s)

Inco

me

for

the

per

iod

19

.59

4

17

.69

8

1

4.3

22

9

.00

1

1

9.5

94

1

7.6

98

1

4.3

22

9

.00

1

Cas

h fl

ow

hed

ge

gai

ns/

loss

es, n

et(1

9.9

89

)

4

.41

2

(1

4.8

53

)

(1

4.4

79

)

(1

9.9

89

)

4

.41

2

(1

4.8

53

)

(1

4.4

79

)

Com

preh

ensi

ve in

com

e lo

ss(3

95

)

2

2.1

10

(53

1)

(5.4

78

)

(39

5)

22

.11

0

(53

1)

(5.4

78

)

See

the

acco

mp

anyi

ng

no

tes

to th

e q

uar

terl

y in

form

atio

n.

Con

solid

ated

Par

ent c

ompa

ny

Com

panh

ia M

inei

ra d

e A

çúca

r e

Álc

ool P

artic

ipaç

ões

Sta

tem

ents

of c

hang

es in

sha

reho

lder

s' e

quity

Six

-mon

th p

erio

d en

ded

Sep

tem

ber

30, 2

014

and

2013

(In

thou

sand

s of

rea

is)

Not

e

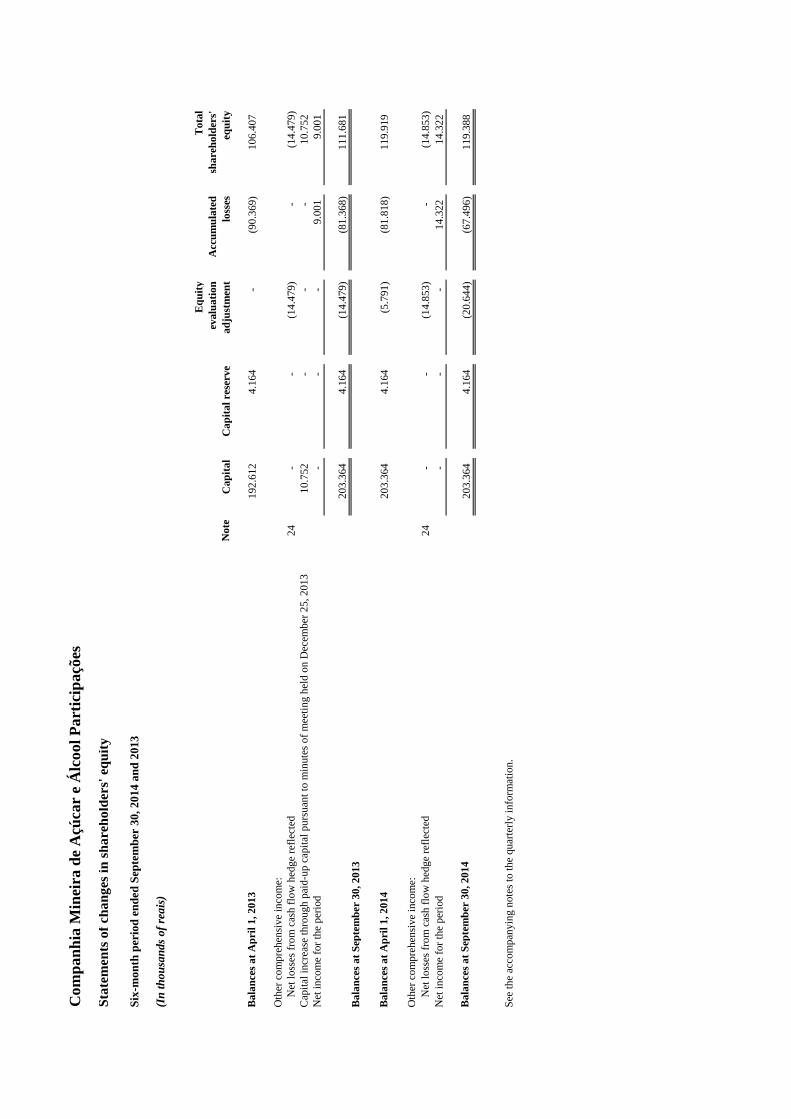

Bal

ance

s at

Apr

il 1,

201

319

2.61

2

4.

164

-

(9

0.36

9)

10

6.40

7

Oth

er c

ompr

ehen

sive

inco

me:

Net

loss

es fr

om c

ash

flow

hed

ge r

efle

cted

24 -

-

(14.

479)

-

(1

4.47

9)

C

apita

l inc

reas

e th

roug

h pa

id-u

p ca

pita

l pur

suan

t to

min

utes

of m

eetin

g he

ld o

n D

ecem

ber

25, 2

013

10.7

52

-

-

-

10.7

52

Net

inco

me

for

the

perio

d -

-

-

9.

001

9.

001

203.

364

4.16

4

(1

4.47

9)

(8

1.36

8)

11

1.68

1

B

alan

ces

at S

epte

mbe

r 30

, 201

3

Bal

ance

s at

Apr

il 1,

201

420

3.36

4

4.

164

(5

.791

)

(81.

818)

119.

919

Oth

er c

ompr

ehen

sive

inco

me:

Net

loss

es fr

om c

ash

flow

hed

ge r

efle

cted

24 -

-

(14.

853)

-

(1

4.85

3)

N

et in

com

e fo

r th

e pe

riod

-

-

-

14.3

22

14.3

22

Bal

ance

s at

Sep

tem

ber

30, 2

014

203.

364

4.16

4

(2

0.64

4)

(6

7.49

6)

11

9.38

8

See

the

acco

mpa

nyin

g no

tes

to th

e qu

arte

rly in

form

atio

n.

Cap

ital

Cap

ital r

eser

ve

Equ

ity

eval

uatio

n ad

just

men

tA

ccum

ulat

ed

loss

es

Tot

al

shar

ehol

ders

' eq

uity

Companhia Mineira de Açúcar e Álcool Participações

Statement of cash flows – Indirect method

Six-month period ended September 30, 2014 and 2013

(In thousands of reais)

Note

09/30/2014 09/30/2013 09/30/2014 09/30/2013(6 months) (6 months) (6 months) (6 months)

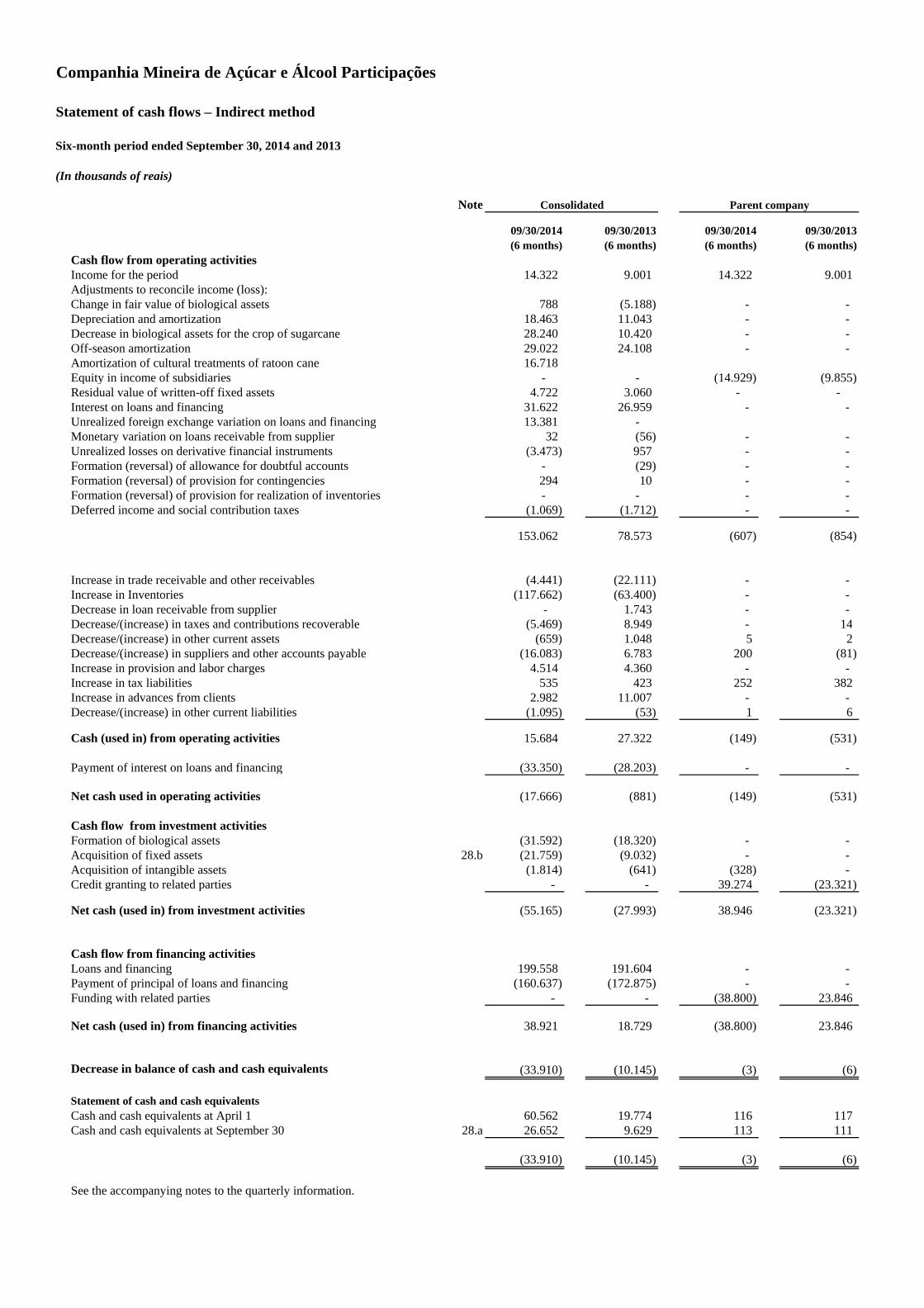

Cash flow from operating activitiesIncome for the period 14.322 9.001 14.322 9.001 Adjustments to reconcile income (loss):Change in fair value of biological assets 788 (5.188) - - Depreciation and amortization 18.463 11.043 - - Decrease in biological assets for the crop of sugarcane 28.240 10.420 - - Off-season amortization 29.022 24.108 - - Amortization of cultural treatments of ratoon cane 16.718 Equity in income of subsidiaries - - (14.929) (9.855) Residual value of written-off fixed assets 4.722 3.060 - - Interest on loans and financing 31.622 26.959 - - Unrealized foreign exchange variation on loans and financing 13.381 - Monetary variation on loans receivable from supplier 32 (56) - - Unrealized losses on derivative financial instruments (3.473) 957 - - Formation (reversal) of allowance for doubtful accounts - (29) - - Formation (reversal) of provision for contingencies 294 10 - - Formation (reversal) of provision for realization of inventories - - - - Deferred income and social contribution taxes (1.069) (1.712) - -

153.062 78.573 (607) (854)

Increase in trade receivable and other receivables (4.441) (22.111) - - Increase in Inventories (117.662) (63.400) - - Decrease in loan receivable from supplier - 1.743 - - Decrease/(increase) in taxes and contributions recoverable (5.469) 8.949 - 14 Decrease/(increase) in other current assets (659) 1.048 5 2 Decrease/(increase) in suppliers and other accounts payable (16.083) 6.783 200 (81) Increase in provision and labor charges 4.514 4.360 - - Increase in tax liabilities 535 423 252 382 Increase in advances from clients 2.982 11.007 - - Decrease/(increase) in other current liabilities (1.095) (53) 1 6

Cash (used in) from operating activities 15.684 27.322 (149) (531)

Payment of interest on loans and financing (33.350) (28.203) - -

Net cash used in operating activities (17.666) (881) (149) (531)

Cash flow from investment activitiesFormation of biological assets (31.592) (18.320) - - Acquisition of fixed assets 28.b (21.759) (9.032) - - Acquisition of intangible assets (1.814) (641) (328) - Credit granting to related parties - - 39.274 (23.321)

Net cash (used in) from investment activities (55.165) (27.993) 38.946 (23.321)

Cash flow from financing activitiesLoans and financing 199.558 191.604 - - Payment of principal of loans and financing (160.637) (172.875) - - Funding with related parties - - (38.800) 23.846

Net cash (used in) from financing activities 38.921 18.729 (38.800) 23.846

Decrease in balance of cash and cash equivalents (33.910) (10.145) (3) (6)

Statement of cash and cash equivalentsCash and cash equivalents at April 1 60.562 19.774 116 117 Cash and cash equivalents at September 30 28.a 26.652 9.629 113 111

(33.910) (10.145) (3) (6)

See the accompanying notes to the quarterly information.

- - - -

Consolidated Parent company

Companhia Mineira de Açúcar e Álcool Participações

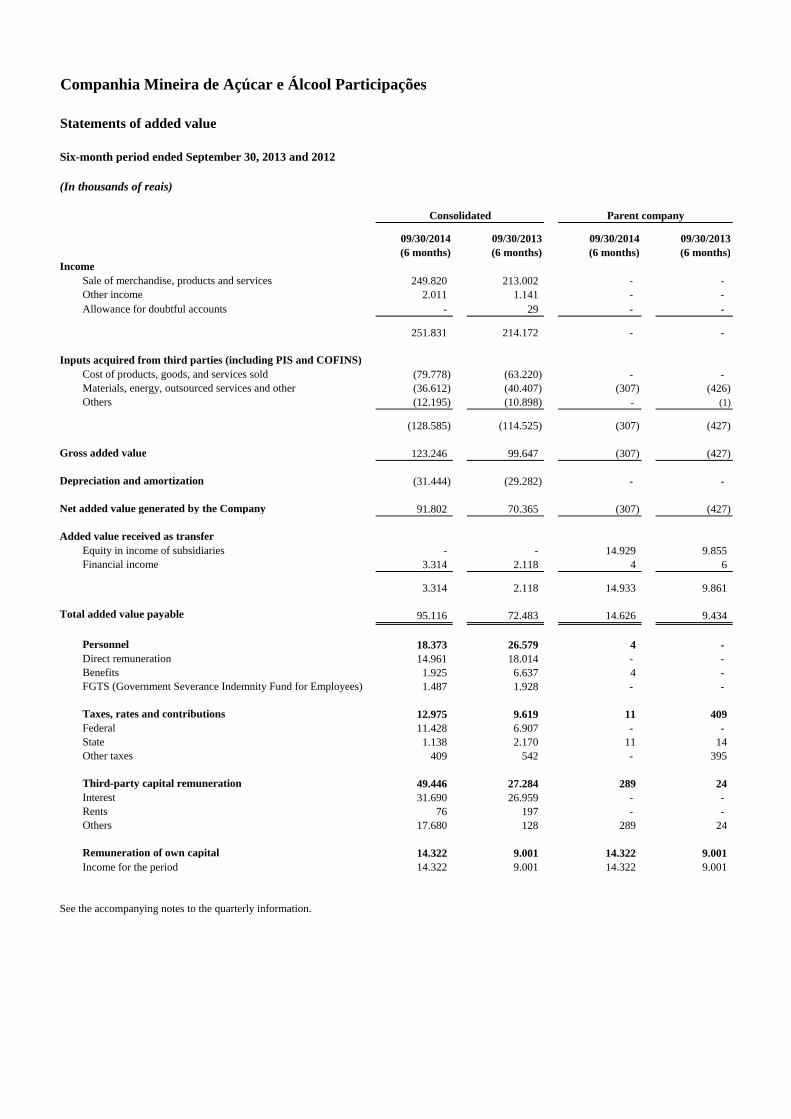

Statements of added value

Six-month period ended September 30, 2013 and 2012

(In thousands of reais)

09/30/2014 09/30/2013 09/30/2014 09/30/2013(6 months) (6 months) (6 months) (6 months)

IncomeSale of merchandise, products and services 249.820 213.002 - - Other income 2.011 1.141 - - Allowance for doubtful accounts - 29 - -

251.831 214.172 - -

Inputs acquired from third parties (including PIS and COFINS)Cost of products, goods, and services sold (79.778) (63.220) - - Materials, energy, outsourced services and other (36.612) (40.407) (307) (426) Others (12.195) (10.898) - (1)

(128.585) (114.525) (307) (427)

Gross added value 123.246 99.647 (307) (427)

Depreciation and amortization (31.444) (29.282) - -

Net added value generated by the Company 91.802 70.365 (307) (427)

Added value received as transferEquity in income of subsidiaries - - 14.929 9.855 Financial income 3.314 2.118 4 6

3.314 2.118 14.933 9.861

Total added value payable 95.116 72.483 14.626 9.434

Personnel 18.373 26.579 4 - Direct remuneration 14.961 18.014 - - Benefits 1.925 6.637 4 - FGTS (Government Severance Indemnity Fund for Employees) 1.487 1.928 - -

Taxes, rates and contributions 12.975 9.619 11 409 Federal 11.428 6.907 - - State 1.138 2.170 11 14 Other taxes 409 542 - 395

Third-party capital remuneration 49.446 27.284 289 24 Interest 31.690 26.959 - - Rents 76 197 - - Others 17.680 128 289 24

Remuneration of own capital 14.322 9.001 14.322 9.001 Income for the period 14.322 9.001 14.322 9.001

See the accompanying notes to the quarterly information.

Consolidated Parent company

Companhia Mineira de Açúcar e Álcool Participações

Report on the review of quarterly information - ITR quarter ended

September 30, 2014

11

Notes to the quarterly financial information (In thousands of reais)

1 Operations The Company, located at Rodovia BR 050 (KM 121) - Distrito Industrial I of Uberaba/MG, is a limited-liability company engaged in holding interest in other companies that produce, sell and export sugar, ethanol, power and other products derived from the processing of sugarcane. It obtained its registry of publicly-traded company on March 4, 2009, by means of CVM/SEP/RIC Circular Nº 001/2009, for trading of common shares on the non-organized over-the-counter market. The Company is the parent company of the following companies:

• Triângulo Mineiro Açúcar e Álcool S/A. (Triângulo Mineiro);

• Vale do Tijuco Açúcar e Álcool S/A. (Vale do Tijuco); and

• Rio Tijuco Agropecuária S/A. (Rio Tijuco).

The subsidiary Triângulo Mineiro Açúcar e Álcool S/A. with head offices in Uberlândia, and the subsidiaries Vale do Tijuco Açúcar e Álcool S/A. and Rio Tijuco Agropecuária S/A., both with head offices in Uberaba, are engaged in the production, sale and export of sugar, ethanol and other products derived from the processing of sugarcane; the provision of services to third parties and industrialization by their order; co-generation and sale of electric power, and it may exploit the planting of sugarcane in their own or third-party land; the sale of their own or third-party sugarcane; the intermediation of sale of sugarcane, and in holding interests as a shareholder or partner in other companies. The subsidiary Triângulo Mineiro Açúcar e Álcool S/A. is at pre-operating phase with estimated grinding of 2.2 million tons per year for the first phase and 5.5 million for the final phase of expansion, according to the business plan. The operations of the subsidiary Vale do Tijuco Açúcar e Álcool S/A. began on April 12, 2010. The industrial plant of Vale do Tijuco Açúcar e Álcool S/A. has grinding capacity of around 4 million tons of sugarcane per year, producing sugar, anhydrous ethanol, hydrated ethanol and power, as well as the by-products fusel oil and sugarcane bagasse. The subsidiary Rio Tijuco Agropecuária S/A. is in the operating phase and its main activity is the cultivation and trading of sugarcane both in own lands and third party lands. The planting of sugarcane requires a period of up to 18 months for maturation and beginning of harvest, which usually occurs between April and November. The sale of the production occurs throughout the year and it does not suffer variations due to seasonality, but only variation of the usual market offer and demand (commodity price and foreign exchange). In order to extend the Company’s debt profile, which on September 30, 2014 presented current liabilities above current assets in the amount of R$ 251,472, Management adopted the following strategies:

Companhia Mineira de Açúcar e Álcool Participações

Report on the review of quarterly information - ITR Quarter ended

September 30, 2014

12

• On September 24, 2014, Certificates of Agribusiness Credit Rights ("CDCA") in the amount of

R$ 99,000 were issued, maturing in 54 installments as of their issuance date, under a fiduciary regime, recorded at BM&F Bovespa and CETIP. The release of that amount occurred subsequently as described in note 30 and will be used for the repayment of short term loans according to their maturities. CDCA installments will bear interest levied on an annual basis, as of the date of payment of the CRA until the respective payment date of each installment of CDCA interest, calculated on the nominal value and equivalent to 100% of accumulated average daily rates of DI over extra group - Interbank Deposits, calculated by CETIP. The issuance will be in favor of Gaia Agro Securitizadora S.A., whose amount mentioned will be released until December 2014. Financial institutions and agents were hired as follow: Leading coordinating bank: BB-Banco de Investimentos S/A; issuing creditor agent: Gaia Agro Securitizadora S.A.; fiduciary agent: Planner Trustee Distribuidora de Títulos e Valores Mobiliários Ltda; registrar agent: BNY mellon Serviços Financeiros Distribuidora de Títulos e Valores Mobiliários S.A.; custodian agent: SLW Corretora de Valores de Câmbio Ltda.; and

• The Company's management is already renegotiating balances of loans and funding adequate to finance its activity, besides extending the debt profile with the main creditor banks whose debt is classified as current liabilities, in order to adjust its operating cash flow. The strategic planning that the Company has been implementing aims to generate positive results in the coming years. Among the main actions taken, it is worth highlighting the obtainment of long-term credit facilities for adjusting working capital and reducing financial expenses.

These strategies were approved by the Company’s shareholders.

2 Group entities The consolidated financial statements include the financial statements of the parent company Companhia Mineira de Açúcar e Álcool Participações and the following subsidiaries: Ownership interest Subsidiaries Country 2014 2013 Triângulo Mineiro Açúcar e Álcool S/A. (Triângulo Mineiro) Brazil 99.99% 99.99% Vale do Tijuco Açúcar e Álcool S/A. (Vale do Tijuco) Brazil 99.99% 99.99% Rio Tijuco Agropecuária S/A. (Rio Tijuco) Brazil 100% - The individual and consolidated financial statements for the twelve-month period ended September 30, 2014 comprise the Company and its subsidiaries (collectively referred to as the “Group”).

Companhia Mineira de Açúcar e Álcool Participações

Report on the review of quarterly information - ITR Quarter ended

September 30, 2014

13

3 Preparation basis

a. Statement of compliance (in relation to IFRS standards and CPC standards) These quarterly information of the Parent Company and the Consolidated, included in the Quarterly Information Form - ITR, were prepared in accordance with CPC 21 (R1) - Interim Financial Reporting and with IAS 34 - Interim Financial Reporting, issued by International Accounting Standards Board (IASB), and presented in accordance with the rules issued by the Brazilian Securities and Exchange Commission (CVM), applicable to the preparation of Quarterly Information - ITR and are identified as “Company” and “Consolidated” respectively.

These practices differ from IFRS applicable to individual interim financial information only with regard to the valuation of investments in subsidiaries under the equity method, where under IFRS the investment would be valued at cost or fair value.

However, there is no difference between the shareholders' equity and consolidated result presented by the Group and the shareholders' equity and result of the Parent company in its individual quarterly information. Accordingly, the Group’s consolidated quarterly information and the Parent Company's individual quarterly information are being presented side by side in a single set of quarterly information.

The issue of individual and consolidated financial statements was authorized by the Board of Directors in a meeting held on November 05, 2014.

b. Measuring basis The individual and consolidated financial statements were prepared based on the historical cost, except for the following items recognized in the balance sheets:

• Financial instruments measured at fair value through profit or loss; and

• Biological assets measured at fair value less sales expenses.

c. Functional currency and presentation currency These individual and consolidated financial statements are being presented in reais, functional currency of the Company and its subsidiaries. All financial information presented in Brazilian Reais has been rounded to the nearest value in thousands, except otherwise indicated.

d. Use of estimates and judgments The preparation of individual and consolidated financial statements according to IFRS and CPC standards requires Management to make judgments, estimates and assumptions that affect the application of accounting principles and the reported amounts of assets, liabilities, income and expenses. Actual results may differ from these estimates. Estimates and assumptions are revised on an ongoing basis. Revisions to accounting estimates are recognized in the year in which the estimates are revised and in any future periods affected. The information on critical judgments that refer to accounting policies adopted that have effects on amounts recognized in the financial statements is presented in the following notes:

• Note 18 – Deferred tax assets and liabilities; and

Companhia Mineira de Açúcar e Álcool Participações

Report on the review of quarterly information - ITR Quarter ended

September 30, 2014

14

• Note 24 – Financial instruments.

Information on uncertainties as to assumptions and estimates that pose a significant risk of resulting in a material adjustment within the next financial year are included in the following notes:

• Note 7 - Trade accounts receivable and other receivables;

• Note 11 – Biological assets;

• Note 12 – Property, plant and equipment; and

• Note 16 – Provision for contingencies.

4 Significant accounting policies The accounting policies described in detail below have been consistently applied to all the periods presented in these individual and consolidated financial statements. The accounting policies have also been consistently applied by the Group companies.

a. Basis of consolidation

(i) Business combination among entities under joint control The measurement of transactions relating to acquisitions of subsidiaries under common control is carried out book value.

(ii) Subsidiaries The financial statements of subsidiaries are included in the consolidated financial statements as from the date they start to be controlled by the Group until the date such control ceases. The accounting policies of the subsidiaries are aligned with the policies adopted by the Group. The Company’s financial information of subsidiaries is recognized under the equity method in the individual financial statements. The financial statements of the subsidiaries on the same base date of submittal of the financial statements are used to calculate equity in the earnings and consolidation. Subsidiaries are consolidated in the consolidated financial statements.

Companhia Mineira de Açúcar e Álcool Participações

Report on the review of quarterly information - ITR Quarter ended

September 30, 2014

15

(iii) Transactions eliminated in the consolidation Balances and transactions with subsidiaries, and any income or expenses derived from transactions with subsidiaries, are eliminated in the preparation of the consolidated financial statements. Unrealized gains originating from transactions with investee company recorded using the equity method, are eliminated against the investment in the proportion of the Company's interest in the investee company. Unrealized losses are eliminated in the same way as unrealized gains, but only up to the point where there is no evidence of loss due to impairment.

b. Foreign currency Foreign currency transactions Transactions in foreign currency are translated into the functional currency of the Group at the exchange rates on the dates of the transactions. Monetary assets and liabilities denominated in foreign currencies at the reporting date are retranslated into the functional currency at the exchange rate at that date. Exchange gain or loss in monetary items is the difference between the amortized cost of the functional currency at the beginning of the period, adjusted by interest and effective payments during the period, and the amortized cost in foreign currency at the exchange rate at the end of the presentation period. Non-monetary items measured at historical costs in foreign currencies are converted by the exchange rate prevailing on the transaction date. Exchange differences arising from the reconversion are charged to income.

c. Financial instruments

(i) Non-derivative financial assets The Group recognizes loans and receivables and deposits initially at the date of the transaction that originated them. The other financial assets (including assets designated at fair value through profit or loss) are initially recognized on the date of the negotiation under which the Company becomes a party to the contractual provisions of the instrument. The Group writes-off a financial asset when the contractual rights to the cash flow of the asset expire, or when the Group transfers the rights to the reception of contractual cash flows over a financial asset in a transaction in which essentially all the risks and benefits of ownership of the financial asset are transferred. Any interest in transferred financial assets that is created or retained by the Group is recognized as a separate asset or liability. Financial assets and liabilities are offset and the net amount reported in the balance sheet only when there is a legally enforceable right of the Group to set off and there is intention to settle on a net basis, or to realize the asset and settle the liability simultaneously. The Group has the following non-derivative financial assets: trade accounts receivable and other receivables, other current assets and receivables with related parties.

Companhia Mineira de Açúcar e Álcool Participações

Report on the review of quarterly information - ITR Quarter ended

September 30, 2014

16

Financial assets measured at fair value through profit or loss A financial asset is classified as measured at fair value through profit or loss if it is held for trading or is designated as such upon initial recognition. The transaction costs are recognized in income (loss) as incurred. Financial assets measured at fair value through profit or loss are measured at fair value and changes in the fair value of such assets, which consider any gain with dividends, are recognized in profit or loss for the year. Financial assets classified as held for trading are actively managed to meet the liquidity needs of the Group. Accounts receivable and other receivables Trade accounts receivable and other receivables are financial assets with fixed or determinable payments, but not quoted on any active market. Such assets are initially recognized at fair value plus any transaction costs directly assignable. After their initial recognition are measured at amortized cost using the effective interest rate method, reduced by any impairment losses. Trade and other receivables include cash and cash equivalents, trade receivables, other receivables and advances to suppliers. Cash and cash equivalents Cash and cash equivalents comprise balances of cash and financial investments with original maturities of three months or less as of the contracting date, which are subject to an insignificant risk of change in value and are used to manage short-term obligations.

(ii) Non-derivative financial liabilities The Group recognizes non-derivative financial liabilities on the date that they are originated. All other financial liabilities are recognized initially on the negotiation date on which the Company and its subsidiaries becomes a party to the contractual provisions of the instrument. The Company and its subsidiaries write off a financial liability when its contractual obligations are discharged or canceled or expired. Such financial liabilities are initially recognized at fair value, net of any transaction costs directly assignable. After their initial recognition, these financial liabilities are measured at amortized cost using the effective interest rate method. The Company and its subsidiaries have the following non-derivative liabilities: loans and financing, suppliers and other accounts payable and debts with related parties.

(iii) Capital – Parent company Common shares Common shares are classified as shareholders' equity. Additional costs directly attributable to the issue of shares are recognized as a deduction from shareholders' equity, net of any tax effects. The Company’s bylaws determines a percentage higher than 25% to payment of compulsory minimum dividends.

Companhia Mineira de Açúcar e Álcool Participações

Report on the review of quarterly information - ITR Quarter ended

September 30, 2014

17

(iv) Derivative financial instruments, including hedge accounting The Group holds derivative financial instruments to hedge its exposure to foreign currency and interest rate changes. Upon initial designation of the derivative as a hedging instrument, the Group formally documents the relationship between the hedge instruments and the hedgeable items, including the risk management goals and the strategy in the execution of the hedge transaction and the hedgeable risk, together with the methods that will be used to assess the effectiveness of the hedge relationship. The Group evaluates the hedge relationship, initially and then continuously, to conclude if hedge instruments are expected to be "highly effective" in the offset of variations in fair value or cash flows of items subject to hedge during the period for which hedge is assigned whether the actual results of each hedge are within the range of 80%-125%. For a cash flows hedge of a planned transaction, the transaction should have its occurrence as highly probable and should present exposure to variations in the cash flows that at the end could affect the reported income (loss). Derivatives are initially recognized at their fair value; any attributable transaction costs are recognized in profit or loss when incurred. After the initial recognition, derivatives are measured at fair value and changes in fair value are recorded as described below. Cash flow hedge When a derivative is designated as a hedge instrument to hedge cash flow variability attributed to a specific risk associated with a recognized asset or liability or a highly probable foreseen transaction that could affect the net income, the effective portion of variation in the derivative's fair value is recognized in other comprehensive income and disclosed in “equity evaluation adjustments” caption in shareholders' equity. Any non-effective portion of the variations in the fair value of the derivative is recognized immediately in net income. When the hedged item is a non-financial asset, the accumulated amount held in other comprehensive income is reclassified to income (loss) in the same year or years during which the non-financial asset does not affect income (loss). In other cases, the amount accumulated in other comprehensive income is transferred to income (loss) in the same year in which the hedgeable item affects income (loss). If the hedge instrument no longer satisfies the hedge accounting criteria, expires or is sold, wound up, exercised or has its designation revoked, then the hedge accounting is discontinued prospectively. If there are no more expectations regarding the occurrence of the planned transaction, then the balance in other comprehensive income is reclassified to income (loss).

d. Property, plant and equipment

(i) Recognition and measurement PP&E items are stated at historical acquisition or construction cost, net of accumulated depreciation and impairment losses, when applicable. The cost includes expenditures that are directly attributable to the acquisition of assets. The cost of assets constructed by the Company itself and its subsidiaries include:

• The cost of materials and direct labor;

• Any other costs directly attributable to bringing the assets to the location and condition required for them to operate in the manner intended by the Management;

Companhia Mineira de Açúcar e Álcool Participações

Report on the review of quarterly information - ITR Quarter ended

September 30, 2014

18

• The costs for dismantling and restoration of the site where these assets are located; and

• Borrowing costs on qualifiable assets.

Purchased software that is integral to the functionality of a piece of equipment is capitalized as part of that equipment. When parts of a property, plant and equipment item have different useful lives, they are accounted for as separate items (major components) of PP&E. Gains and losses on disposal of a property, plant and equipment item are determined by comparing the proceeds from disposal with the carrying amount of Property, plant and equipment and are recognized net within "Other income" in the income (loss).

(ii) Subsequent costs Subsequent expenses are capitalized only when it is probable that associated future benefits may be earned by the Company and its subsidiaries. Maintenance expenses and recurring repairs are recognized in the income when incurred.

(iii) Maintenance costs The maintenance cost of a component of property, plant and equipment is recognized in the book value of the item when it is probable that the future economic benefits embodied in the component will flow and its cost can be reliably measured. The book value of the component that has been replaced by another is written off. Costs of normal maintenance on property, plant and equipment are charged to the income statement as incurred. The subsidiary Vale do Tijuco Açúcar e Álcool S/A. performs annual maintenance at its manufacturing unit, approximately in the period from December to March. The main maintenance costs include costs of labor, materials, outsourced services and overhead allocated during the off-season period. Said costs are accounted for as a component of the cost of the equipment and depreciated during the following harvest. Any other type of expenditure, which does not increase the useful life or maintain the grinding capacity, is recognized as an expense.

(iv) Depreciation Items of property, plant and equipment are depreciated from the date they are installed and are available for use, or, in the case of assets constructed by the Company, as of the date the construction is concluded and the asset is available for use.

Companhia Mineira de Açúcar e Álcool Participações

Report on the review of quarterly information - ITR Quarter ended

September 30, 2014

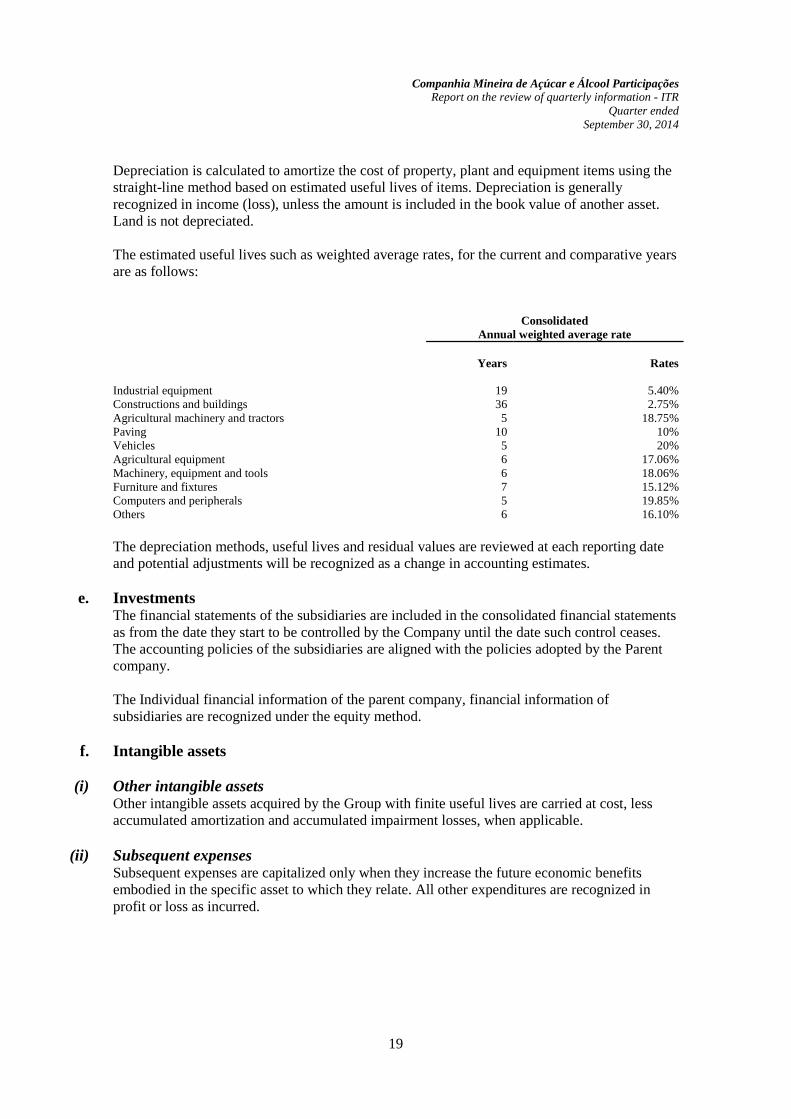

19

Depreciation is calculated to amortize the cost of property, plant and equipment items using the straight-line method based on estimated useful lives of items. Depreciation is generally recognized in income (loss), unless the amount is included in the book value of another asset. Land is not depreciated. The estimated useful lives such as weighted average rates, for the current and comparative years are as follows: Consolidated Annual weighted average rate

Years Rates Industrial equipment 19 5.40% Constructions and buildings 36 2.75% Agricultural machinery and tractors 5 18.75% Paving 10 10% Vehicles 5 20% Agricultural equipment 6 17.06% Machinery, equipment and tools 6 18.06% Furniture and fixtures 7 15.12% Computers and peripherals 5 19.85% Others 6 16.10% The depreciation methods, useful lives and residual values are reviewed at each reporting date and potential adjustments will be recognized as a change in accounting estimates.

e. Investments The financial statements of the subsidiaries are included in the consolidated financial statements as from the date they start to be controlled by the Company until the date such control ceases. The accounting policies of the subsidiaries are aligned with the policies adopted by the Parent company. The Individual financial information of the parent company, financial information of subsidiaries are recognized under the equity method.

f. Intangible assets

(i) Other intangible assets Other intangible assets acquired by the Group with finite useful lives are carried at cost, less accumulated amortization and accumulated impairment losses, when applicable.

(ii) Subsequent expenses Subsequent expenses are capitalized only when they increase the future economic benefits embodied in the specific asset to which they relate. All other expenditures are recognized in profit or loss as incurred.

Companhia Mineira de Açúcar e Álcool Participações

Report on the review of quarterly information - ITR Quarter ended

September 30, 2014

20

(iii) Amortization Amortization is recognized in income on a straight-line basis over the estimated useful lives of the intangible assets as of the date they are available for use. The estimated useful life for the current years and comparative are presented below: Software 5 years The depreciation methods, useful lives and residual values are reviewed at each reporting date and potential adjustments will be recognized as a change in accounting estimates.

g. Biological assets Biological assets are measured at fair value less sales expenses. Changes in fair value less sales expenses are recognized in results. Sale costs include all costs that are necessary to sell the assets. Sugarcane is transferred to the cost of production at their fair value, minus estimated selling expenses determined on the cutoff date.

h. Leased assets Leases in terms of which the Group assumes substantially all the risks and rewards of ownership are classified as finance leases. Upon initial recognition, the leased asset is measured at an amount equal to the lower of its fair value and the present value of the minimum lease payments. Subsequent to initial recognition, the asset is accounted for in accordance with the accounting policy applicable to that asset. The other leases are operating leases and are not recognized in the balance sheets of the Group.

i. Inventories Inventories are measured at the lower of cost and net realizable value. Inventory costs are valued at the average cost of purchase or production and include expenses incurred in the acquisition of inventories, production and conversion costs and other costs incurred in bringing them to their current locations and conditions. The net realizable value is the estimated price at which inventories can be realized in the normal course of business, less the estimated completion costs and selling expenses. The sugarcane consumed in the production process is measured at its fair value, net of sales expenses determined on the cutoff date.

j. Impairment

(i) Financial assets (including receivables) A financial asset not measured at fair value through profit or loss is assessed at each reporting date for objective evidence of impairment loss. An asset is impaired when there is objective evidence that a loss event has occurred after the initial recognition of the asset, and that such loss event had a negative effect on the projected future cash flows of that asset that can be reliably estimated. Objective evidence that financial assets (including equity securities) are impaired can include default or delinquency by a debtor, restructuring of the amount due to the Group on terms that the Group would not consider otherwise, indication that the debtor or issuer will file for bankruptcy, or disappearance of an active market for a security. In addition, for an equity

Companhia Mineira de Açúcar e Álcool Participações

Report on the review of quarterly information - ITR Quarter ended

September 30, 2014

21